Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

SPAIN DATA

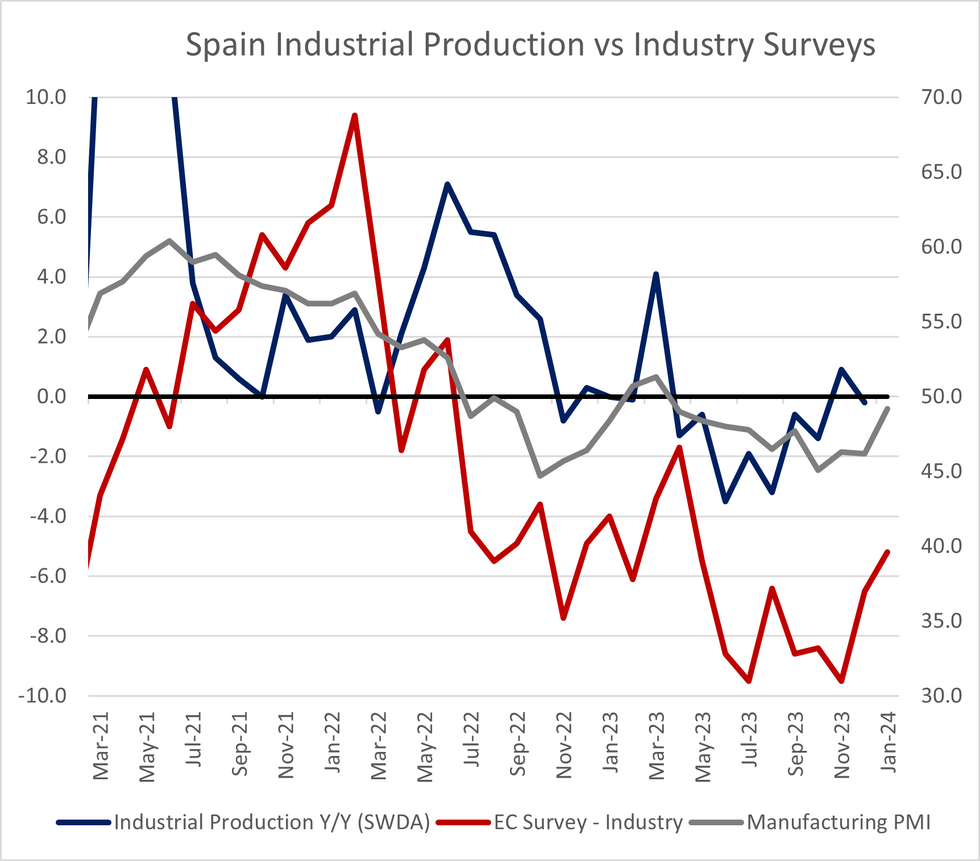

Spanish industrial production ended the year on a weak note, printing at -0.3% M/M SWDA in December (vs a 6-analyst consensus of -0.1% and a 0.1pp upwardly revised +1.1% prior) and -0.2% Y/Y SWDA (vs a 0.1pp upwardly revised +0.9% prior).

- The unadjusted annual series saw a larger -4.0% Y/Y decline (vs a 0.1pp downwardly revised 1.0% prior).

- Of the major subcategories of production, consumer goods saw the largest sequential monthly fall at -1.7% M/M (vs +1.3% prior), led by durable goods. Capital goods fell -1.5% M/M (vs 2.2% prior). Energy was the largest upside contributor, rising +3.1% M/M (vs +0.4% prior).

- The December fall in IP comes despite various survey measures pointing to a recovery in the Spanish industrial outlook. Both the manufacturing PMI and January EC Industrial Confidence metric rose in January, though both still remain in contractionary territory.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok