Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

GERMAN DATA

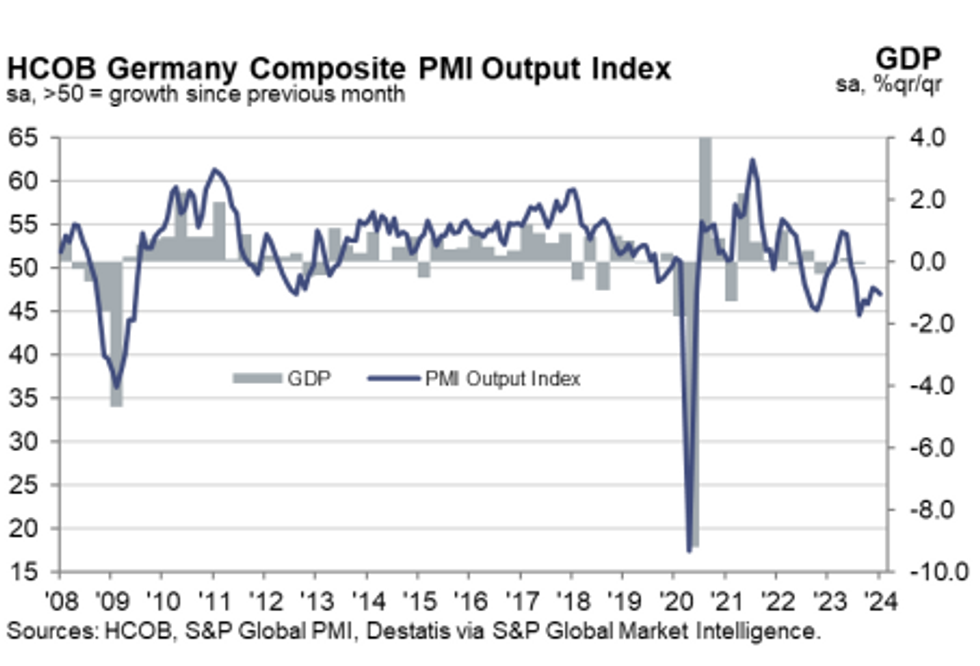

Similarly to France, the Germany flash Jan PMI saw services come in lower-than-consensus and manufacturing higher, prompting further support for EGBs. Though again, both remain below 50. Services printed at 47.6 (vs 49.3 cons and prior) - a 5-month low and the second consecutive deceleration - while manufacturing was 45.4 (vs 43.7 cons, 43.4 prior). As previewed by our earlier post, there was evidence of continued wage pressures in services (as in France) and some impact of Red Sea disruptions on manufacturers.

Key notes from the release are:

- "On the price front, inflationary pressures remained elevated in the service sector, where firms remarked on the influence of wage demands".

- "Prices in the manufacturing sector continued to fall, although the rate of decline in factory input costs was the weakest for nine months amid reports of "some supply disruption due to the events in the Red Sea".

- Services prices charged rose steeply once again, though manufacturing factor gate prices fell at a faster rate.

- "Signs of easing capacity pressures were reflected in further job losses across Germany’s private sector in January". Job cuts were again confined to manufacturing, with services employment rising slightly.

- "Where a reduction [in new work] was recorded, firms commented on customer hesitancy amid a backdrop of high financing costs and geopolitical uncertainty". The services sector saw a faster decrease in new business compared to manufacturing counterparts.

- "Lower international demand remained a factor behind Germany’s slowdown".

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok