Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

EUROZONE DATA

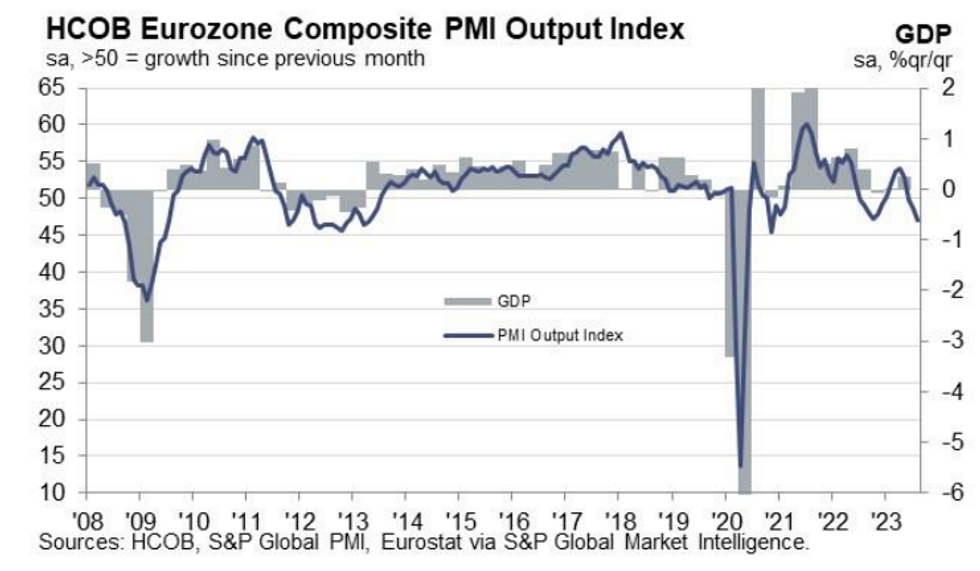

Eurozone August flash PMIs unsurprisingly reflected the French and German reports released earlier, with weaker than expected services, and a surprising uptick in manufacturing. Amid weak demand, employment slowed to near-stall speed with services inflation ticking higher.

- Eurozone Manufacturing PMI rose to a 3-month high of 43.7 (had been expected coming into today to remain steady at July's 42.7), but Services fell much more quickly than had been expected to a 30-month low 48.3 (vs 50.5 survey, 50.9 prior). Overall Composite fell to a 33-month low of 47.0 from 48.6 in July and the 48.5 expected.

- With the French and German dynamics already known and incorporated into the eurozone-wide reading, including HCOB S&P Global noting Germany potentially being the "sick man of Europe" with the strongest overall decline recorded among Euro area countries in the survey, the report is interesting in its description of activity elsewhere in the eurozone.

- Overall Services activity fell into contraction for the first time since December 2022, no doubt largely influenced by a 47.3 reading in Germany and 46.7 in France.

- Eurozone ex-Germany and France "suffered a moderate decline in output compared to France and Germany, yet the reduction was notable in being the first recorded since December amid an ongoing loss of manufacturing output alongside a near stagnation of activity in the service sector".

- Italy and Spain had posted relatively solid activity in prior months, including Services readings solidly above 50 in Jun and Jul, suggesting they may have deteriorated in August.

- The HCOB S&P Global Nowcast based on PMI figures points to an overall 0.2% contraction in Eurozone GDP in Q3.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok