Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

STIR

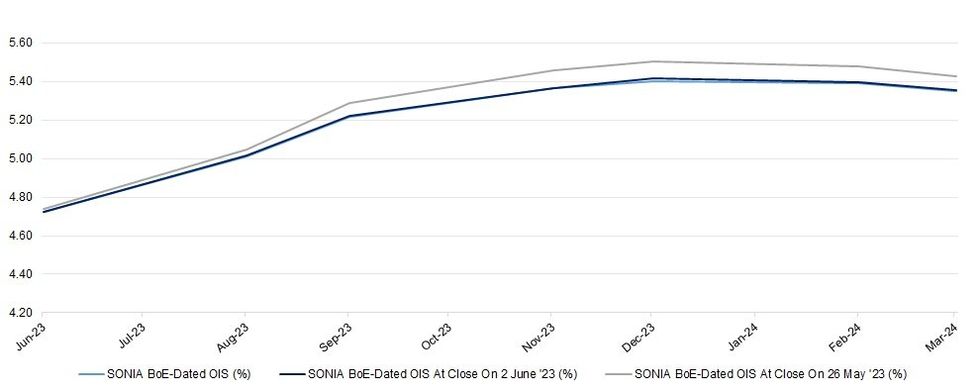

Akin to ECB pricing, BoE-dated OIS hasn’t seen much in the way of domestic drivers of note on Monday.

- There was an initial uptick on the wider cheapening in core global FI markets and higher oil prices, albeit with the latter moderating from extremes. That allowed terminal policy rate pricing to show a little above 5.50% this morning, before moderating with Gilts happy to generally consolidate within the range established early on, even as core global FI counterparts extended their early weakness.

- Terminal pricing currently sits just below 5.50% in policy rate terms (seen at the end of December meeting), around 5.475%, with residual chances of a > 50bp hike priced over the next few MPC decisions.

- We didn’t get near a challenge of recent hawkish extremes before the move back from intraday highs.

- Local headline flow has been fairly limited, with nothing in the way of meaningful movement in the final services PMI reading for May.

- The remainder of the week is light on market moving domestic economic data releases, before tier 1 data and BoE speak returns next week.

| BoE Meeting | SONIA BoE-Dated OIS (%) | Difference Vs. Current Effective SONIA Rate (bp) |

| Jun-23 | 4.725 | +29.7 |

| Aug-23 | 5.009 | +58.1 |

| Sep-23 | 5.218 | +79.0 |

| Nov-23 | 5.365 | +93.7 |

| Dec-23 | 5.402 | +97.4 |

| Feb-24 | 5.392 | +96.4 |

| Mar-24 | 5.352 | +92.4 |

MNI London Bureau | +44 0203-865-3809 | anthony.barton@marketnews.com

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok