Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

Thursday’s data schedule will focus on the ECB’s MPC meeting today, ahead of the Easter long weekend. US retail sales, jobless claims and the U Michigan index will be of interest in the afternoon.

ECB Monetary Policy Decision (1245 BST)

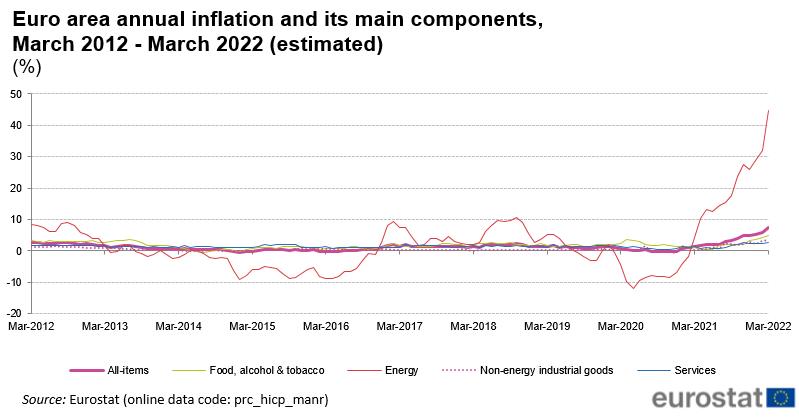

Eurozone March inflation jumped 2pp to 7.5% Y/Y, significantly outpacing the 6.7% consensus estimate and producer prices accelerated to 31.4% Y/Y in February, up from 1.5% Y/Y 12m before. The upside potential for oil prices in the event of further restrictions on Russian energy implies little respite in soaring prices.

Consensus expects no material change in policy at the April ECB meeting due to wages not yet seen adjusting to spot inflation, however, MNI believes this meeting is a close call and that markets should be prepared for a hawkish surprise. The key focus will be whether rhetoric shifts to highlight inflation concerns over growth, hinting at a pre-September hike. The more dovish scenario would see emphasis placed more upon downside growth risks and uncertainty regarding the Ukraine war.

For MNI’s in-depth preview of the upcoming meeting click here.

US Retail Sales (1330 BST)

The March retail sales print sees small improvements, implying that the onset of the Ukraine war and inflation failed to dampen consumer spending in the US. Sales are projected to tick up to +0.6% m/m in March (Feb +0.3%) and recover to +1.0% m/m (Feb +0.2%) excluding auto which fell 22% y/y in March.

US Jobless Claims (1330 BST)

US initial jobless claims are seen ticking up 4k to 170k in the week ending April 9, remaining around the same level seen over the last four weeks. These are levels last seen in the late 60’s, implying extremely tight labour market conditions which underpin confidence in the US economy. Continuing claims are expected to decrease by 23k to 1500k.

University of Michigan Sentiment (1500 BST)

Consensus is expecting the U. Michigan consumer sentiment to step down to 59.0 from 59.4 in the prelim April print, reaching a fresh 2011 low. The one-year inflation expectation is seen inching up 0.1pp to 5.5% at a new 1981 high.

The slide in sentiment is largely inflation based as consumers highlighted concerns of reduced living standards (the Ukraine war not being cited).

With the ECB meeting today, policymaker appearances include President Christine Lagarde at the post decision press conference and in the U.S., just Cleveland Fed's Loretta Mester and Philadelphia Fed's Patrick Harker due to speak. Links to events are in the calendar below.

| Date | GMT/Local | Impact | Flag | Country | Event |

| 14/04/2022 | 0600/0800 | *** |  | SE | Inflation report |

| 14/04/2022 | 1100/0700 | * |  | TR | Turkey Benchmark Rate |

| 14/04/2022 | 1145/1345 | *** |  | EU | ECB Deposit Rate |

| 14/04/2022 | 1145/1345 | *** | | EU | ECB Main Refi Rate |

| 14/04/2022 | 1145/1345 | *** | | EU | ECB Marginal Lending Rate |

| 14/04/2022 | 1230/0830 | ** |  | CA | Wholesale Trade |

| 14/04/2022 | 1230/0830 | ** | | CA | Monthly Survey of Manufacturing |

| 14/04/2022 | 1230/0830 | ** |  | US | Jobless Claims |

| 14/04/2022 | 1230/0830 | *** | | US | Retail Sales |

| 14/04/2022 | 1230/0830 | *** | | US | PPI |

| 14/04/2022 | 1230/0830 | ** | | US | Import/Export Price Index |

| 14/04/2022 | 1230/0830 | ** | | US | WASDE Weekly Import/Export |

| 14/04/2022 | 1230/1430 | | EU | ECB President Lagarde Post-meet presser | |

| 14/04/2022 | 1400/1000 | *** | | US | University of Michigan Sentiment Index (p) |

| 14/04/2022 | 1400/1000 | * | | US | Business Inventories |

| 14/04/2022 | 1430/1030 | ** | | US | Natural Gas Stocks |

| 14/04/2022 | 1530/1130 | ** | | US | NY Fed Weekly Economic Index |

| 14/04/2022 | 1530/1130 | * | | US | US Bill 08 Week Treasury Auction Result |

| 14/04/2022 | 1530/1130 | ** | | US | US Bill 04 Week Treasury Auction Result |

| 14/04/2022 | 1920/1520 | | US | Cleveland Fed's Loretta Mester | |

| 14/04/2022 | 2200/1800 | | US | Philadelphia Fed's Patrick Harker |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.