Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

STIR FUTURES

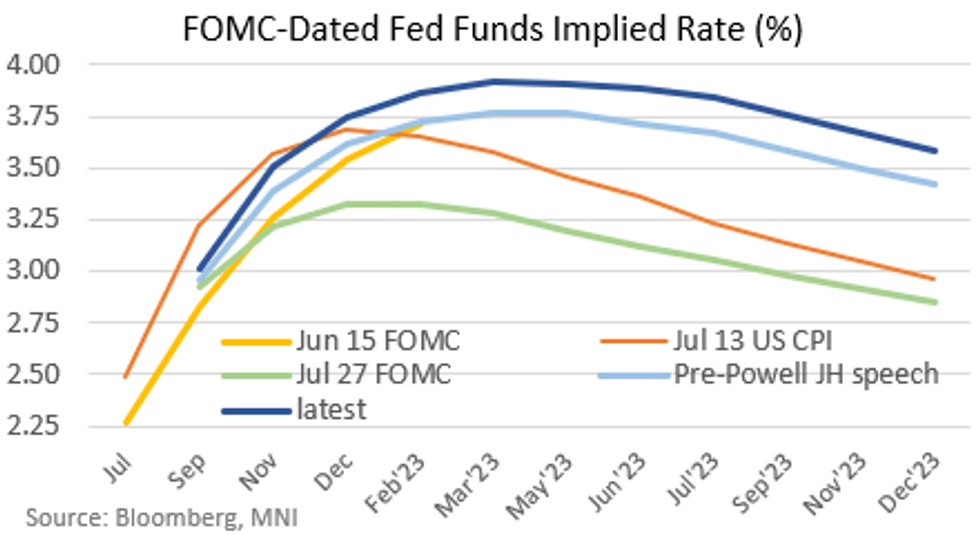

Futures-implied U.S. rate pricing is steady/a little firmer early Wednesday, sustaining the "higher for longer" Fed rate path seen following Jackson Hole.

- September FOMC hike pricing is flat vs Tuesday and has been fairly steady this week, roughly between 64 and 69bp implied, and currently sits at 68bp. In other words, a better than even chance of a 75bp (vs 50bp) hike, but not a done deal as August draws to a close.

- A strong JOLTS figure yesterday helped bolster 75bp Sept pricing; today's ADP data will be fresher in both data coverage (Aug vs JOLTS's Jul) and approach (see our earlier notes regarding the new methodology), and will set the stage for Friday's key nonfarm payrolls reading. And of course, MNI Chicago PMI (BBG survey expects it to remain at 52.1, same as July) merits watching.

- December FOMC pricing remains near the week's highs at 3.74%, +141bp from current levels, up 2bp overnight. The Fed rate cycle is seen peaking at/near 4% in Q2 2023 before receding.

- In that regard, Cleveland Fed Pres Mester's prepared comments will be eyed for any further insight following her Jackson Hole media appearance in which she said rates may have to go above 4% in 2023 and hold there.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok