Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

US OUTLOOK/OPINION

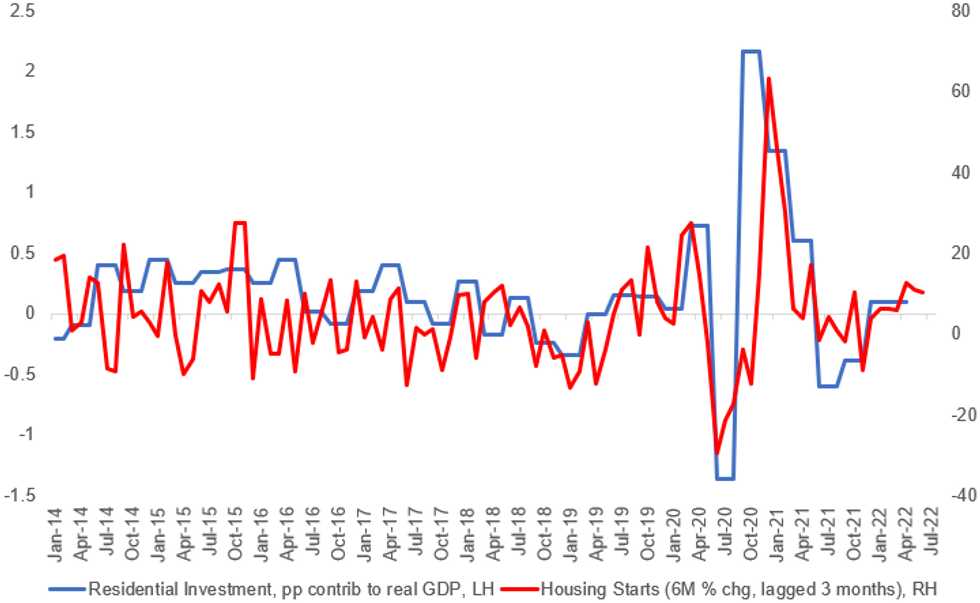

Wednesday's Housing Starts data for April came in better than expected in growth terms (-0.2% vs -2.1% exp) BUT that includes a big downward revision to prior (from +0.3% to -2.8%).

- Looking at the annualized number as opposed to the % change, 1.756mn starts were expected in April, vs 1.793mn in March: but we got 1.724mn (versus a downwardly revised 1.728mn in March).

- Apart from one month, housing starts have plateaued at post-2006 highs above 1.7mn since November 2021.

- The "soft" data has already started turning, notably with the larger-than-expected drop in NAHB homebuilder sentiment out yesterday (to its lowest level since April 2020).

- But deteriorating homebuilder optimism is to be expected with the big spike in mortgage prices and weakening overall economic sentiment, and the NAHB reading was above 50 (68), so more homebuilders saw conditions as "good" than "poor".

- For now, the housing sector is contributing and isn't dragging on the economy, and the strong starts at the outset of 2022 should mean completions are robust through mid-year.

- But likewise, conditions are deteriorating to the point where it's probably not going to be a major contributor to growth by late 2022 either. For context, in Q421 and Q122, residential investment added just 0.1pp to GDP.

Source: BEA, MNI

Source: BEA, MNI

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok