Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

GERMAN DATA

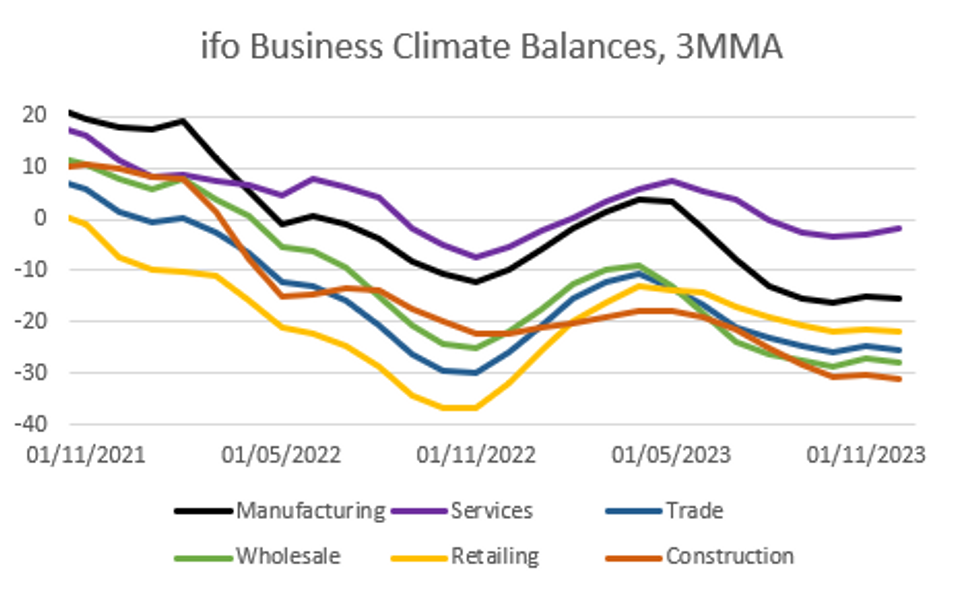

The December ifo business climate index came in weaker than expected at 86.4 vs 87.7 (consensus) and 87.2 (prior, revised from 87.3). The index thus failed to repeat its small gain in November, having previously fallen for 5 consecutive months.

- The downside vs consensus was driven by both a miss in the current assessment (88.5 vs 89.5 cons, 89.4 prior) as well as expectations (84.3 vs 85.6 cons, 85.1 prior, revised from 85.2).

- The overall weakness matches Friday’s flash German December PMIs, though developments in the individual sectors were flipped, with manufacturing ticking up in the PMI (43.1 vs 42.6 prior) but declining in the Ifo (-17.2, the weakest value since June 2020, vs -13.8 prior) and services weakening re PMI (48.4 vs 49.6 prior) but strengthening re ifo (-1.7 vs -2.5 prior).

- For the manufacturing sector, the decline was clear on both the current assessment and the expectations balances (current assessment -6.9, the weakest value since October 2020, vs -3.5 prior, expectations -26.9 vs -23.6 prior). Energy-intensive companies especially were seen to be struggling.

- The services sector stayed comparatively resilient, with both the current assessment and expectations gaining.

- The trade sector was hit by weak Christmas sales, and assessed both its current conditions and expectations worse than before (total business climate at -26.6 vs -22.2 prior).

- On a longer term picture, the 3MMA measure saw all sectors except services ticking down vs November. The decrease was limited but the report suggests a strengthening of German economic conditions is not imminent.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok