Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

SPAIN DATA

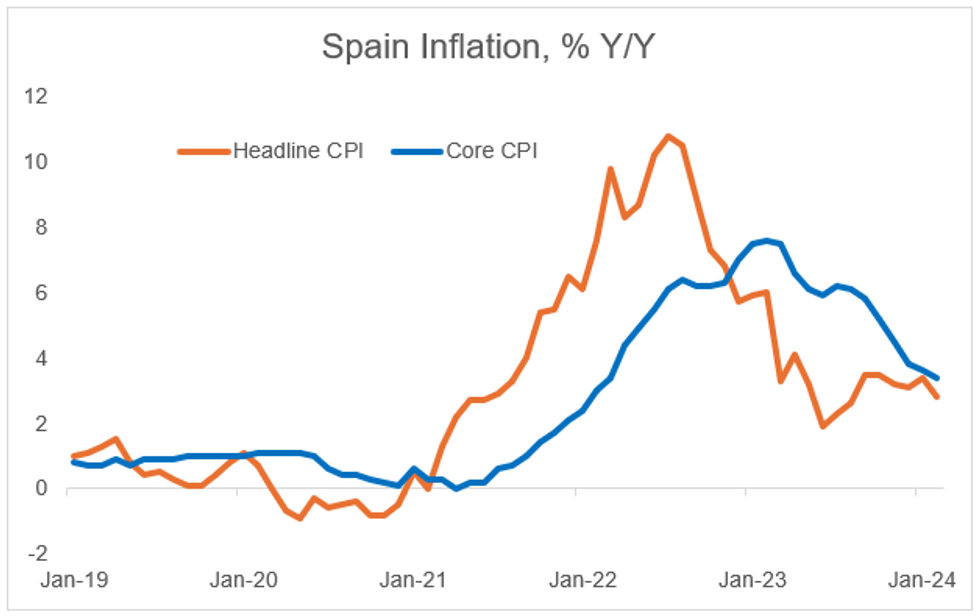

Spanish preliminary February HICP came in slightly firmer-than-expected at +2.9% Y/Y (vs +2.8% cons and 3.5% prior), with the sequential reading a more sizeable upside miss at 0.4% M/M (vs +0.2% cons and -0.2% prior). The national CPI measure data came in line at 2.8% Y/Y (vs +2.8% cons; +3.4% prior) and 0.3% M/M (vs +0.4% cons; +0.1% prior).

- Core inflation also slightly exceeded expectations, printing at +3.4% Y/Y (vs 3.3% cons and 3.6% prior). For the core rate, this represents the 8th consecutive decline and the lowest value since March 2022.

- The headline rate was strongly driven downward by electricity prices according to INE, in line with analyst expectations. Fuel prices increased, however.

- INE did not comment on food inflation, which analysts also expected to decrease.

- The slight upside surprise on core CPI in particular may marginally bias upward expectations for Friday's Eurozone-wide inflation prints, but the lack of detail in the report (particularly on services) makes it difficult to draw any firm conclusions other than that there was no disinflationary surprise this month.

- For context, Spain represents 11% of the Eurozone HICP basket in 2024.

MNI, INE

MNI, INE

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok