Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

NORWAY

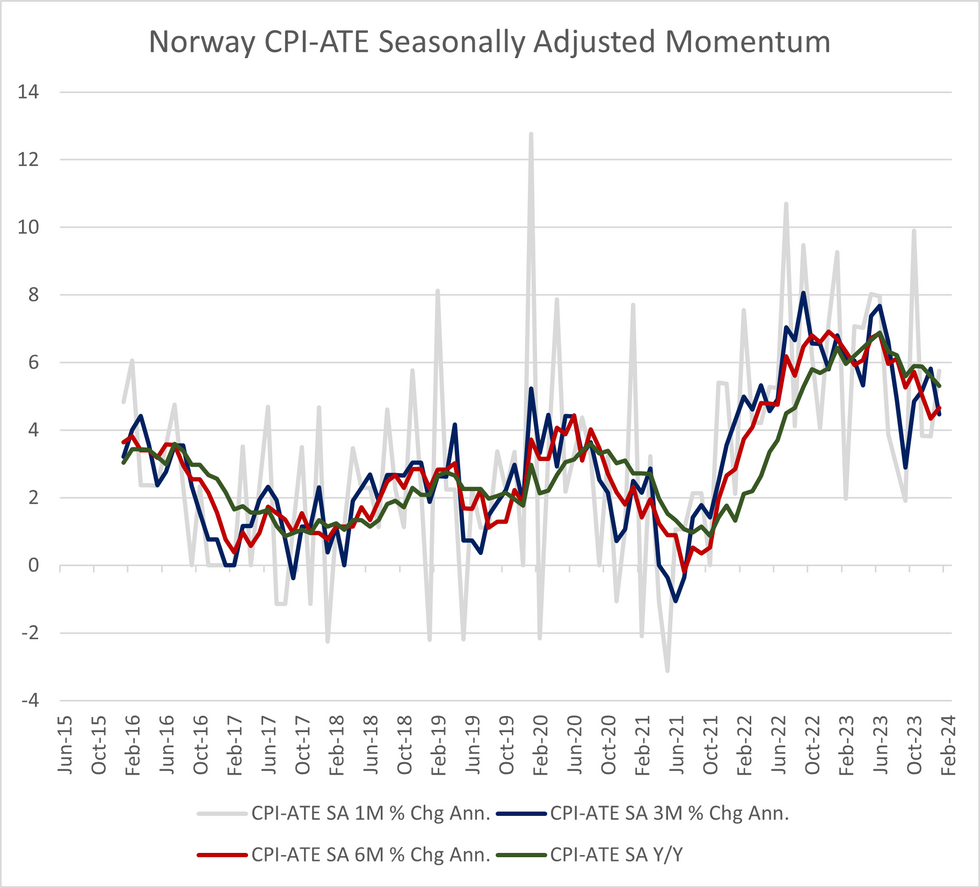

January's inflation data shows a decelerating but bumpy path for CPI-ATE momentum. Overall, the data gives little reason for the Norges Bank to deviate from their current guidance, which states that the policy rate will need to remain at current levels for "some time ahead".

- CPI-ATE momentum measured on a 3M/3M SAAR basis moderated to 5.15% (vs 5.28% prior), from a peak of 7.22% in July 2023.

- When looking at annualised SA inflation at different time horizons (see chart), the trend is clearly downwards but shorter-horizons (e.g. 1M ann and 3M ann) are volatile. In January, even the 6M ann measure accelerated a touch to 4.66% (vs 4.35% prior).

- January also introduced the new 2024 weights. Of the main sub-components, energy saw its weight fall to 43.2 (vs 55.8 prior), with core goods and services seeing increased weights as a result. All else-equal, this assigns even more importance to the CPI-ATE components which are still running far above the 2% target.

- The smaller weight of energy likely contributed to the higher-than-expected headline CPI print this month, since base effects are still pulling down annual inflation. Going forward, the lower weight will place less upward pressure on headline CPI as base effects reverse (which we expect to see over the next 2/3 months).

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok