Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

ASIA FX

Energy prices have started this week much the same way they ended the last one, continuing to trend higher. However, correlations between some USD/Asia pairs and energy prices are quite different now compared to the norm for 2022.

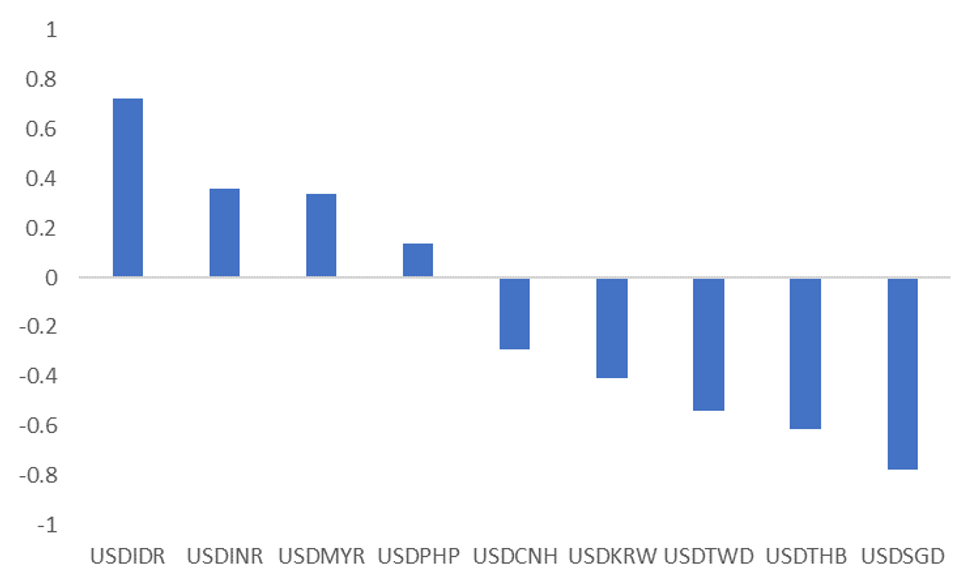

- The first chart shows the correlation between energy prices and USD/Asia pairs for the past month. For pairs like USD/SGD, USD/THB, USD/TWD and USD/KRW, they have all weakened as energy prices have trended higher.

- At the opposite end, USD/IDR, USD/INR and USD/MYR have had a positive correlation with energy prices over the past month.

Fig 1: USD/Asia FX & Energy Price Correlations - Past Month

Source: MNI - Market News/Bloomberg

Source: MNI - Market News/Bloomberg

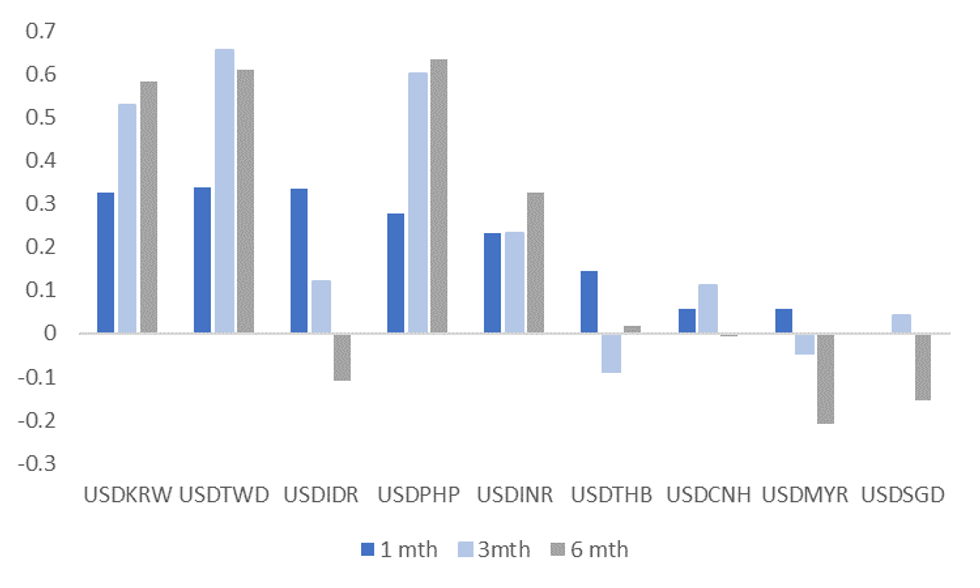

- The second chart plots the average correlations between USD/Asia pairs and energy prices for 2022. We do this for 1 month periods, but also 3 and 6 month.

- USD/KRW and USD/TWD have usually had negative correlations with energy prices in 2022. This is likely to reflect the negative terms of trade for these countries from rising energy prices and the feedback loop such rises have to Fed expectations. This hasn't occurred during the most recent run up in energy prices, with Fed expectations staying fairly flat.

- It may be the case that we need to see Fed expectations being biased higher by rising energy prices before the correlation with such USD/Asia pairs turns more positive.

- MYR and SGD look reasonably well placed to maintain their historical correlations. Malaysia has a positive terms of trade relationship with energy, while the SGD may benefit from expectations that the MAS has more tightening work to do the higher energy prices rise.

- INR and PHP may not fare as well, at least on a relative value basis, particularly given weaker starting positions for trade balances compared to the rest of the region.

Fig 2: USD/Asia & Energy Price Correlations - Averages For 2022

Source: MNI - Market News/Bloomberg

Source: MNI - Market News/Bloomberg

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok