Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

STIR

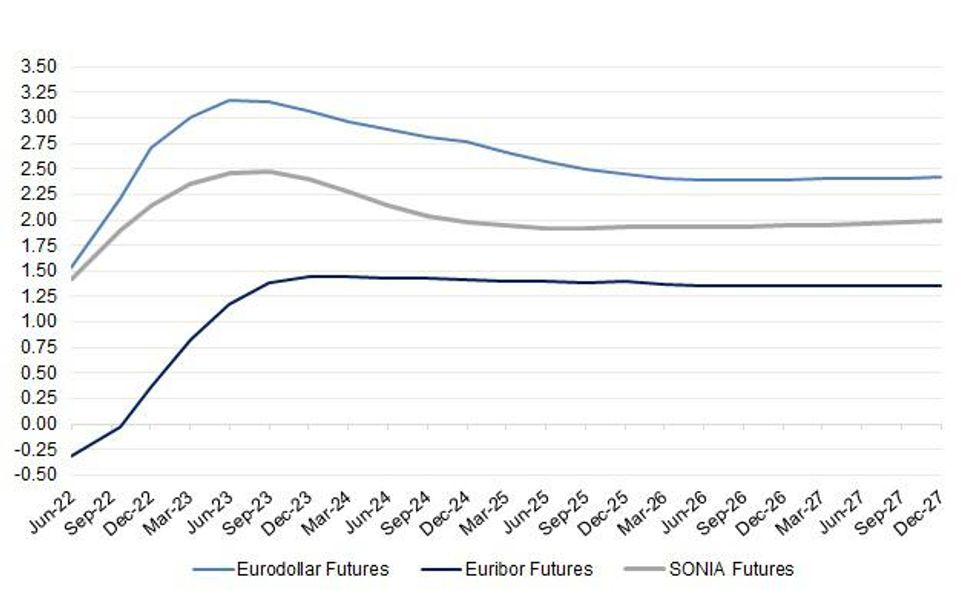

While the major central bank hiking cycles embedded into the various STIR curves have been widely discussed, we want to quickly highlight the other side of the coin when it comes to Fed, BoE & ECB market pricing i.e. the degree of “policy error” priced into the major 3-month futures curves at present (this is of course an approximation given that we are using Eurodollar, EURIBOR & SONIA futures for liquidity and time horizon purposes, not OIS).

- Note that we use contract price levels observed on 30 March ’22 for consistency.

- The highest implied rate on the Eurodollar curve currently sits at 3.18%, in June ‘23. That is then pared down to 2.385% come Sep ’26 (the curve is virtually flat beyond this point), implying 79.5bp of rate cuts over that horizon, with 42bp of that cutting cycle priced by Dec ’24. This suggests that the Fed hiking cycle will be shorter, in time horizon terms, than the central bank currently believes (albeit occurring at a faster velocity than was projected in the latest dot plot), with a need to hike clearly above the assumed neutral level before cuts begin i.e. the market is saying that the Fed will not be able to engineer a soft landing, despite the central bank making assurances to the contrary. A reminder that the Fed discussion re: the velocity of hikes has already moved on since the most recent FOMC decision, with hawkish tones becoming more apparent.

- The story for the BoE is relatively similar when it comes to market projected rate hikes, albeit with shallower moves foreseen. SONIA futures are indicating a peak rate of 2.47% in Sep ’23, with 56bp of cuts then priced through Sep ’25, and the curve virtually flat thereafter. A reminder that the BoE already started to sound a little more cautious/guarded at its most recent MPC meeting, although that hasn’t stopped the contracts from Dec ’22 further out from registering fresh cycle lows i.e. new highs in implied rate terms. Meanwhile, the aforementioned BoE caution leaves the Jun ’22 contract ~30bp above its cycle low, with worry about UK standards of living owing to spiralling inflation evident.

- Meanwhile, the EURIBOR strip continues to price relatively aggressive hikes when compared to the ECB’s gradualist guidance, with this week’s regional inflation data (namely the CPI readings out of Germany & Spain) allowing markets to further test the ECB’s view. Note that the EURIBOR strip currently projects a peak rate of 1.45%, although that comes a touch later than what is seen for the Fed & BoE, in Mar’24. The “policy error” priced into the strip isn’t anywhere near that seen in the Eurodollar and SONIA futures curves, with 9bp of cuts seen between the Mar ’24 implied rate peak and Jun ’26.

Fig. 1: Implied Interest Rates On The Eurodollar, SONIA & EURIBOR Futures Strips (%)

Source: MNI - Market News/Bloomberg

Source: MNI - Market News/Bloomberg

MNI London Bureau | +44 0203-865-3809 | anthony.barton@marketnews.com

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok