Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

STIR

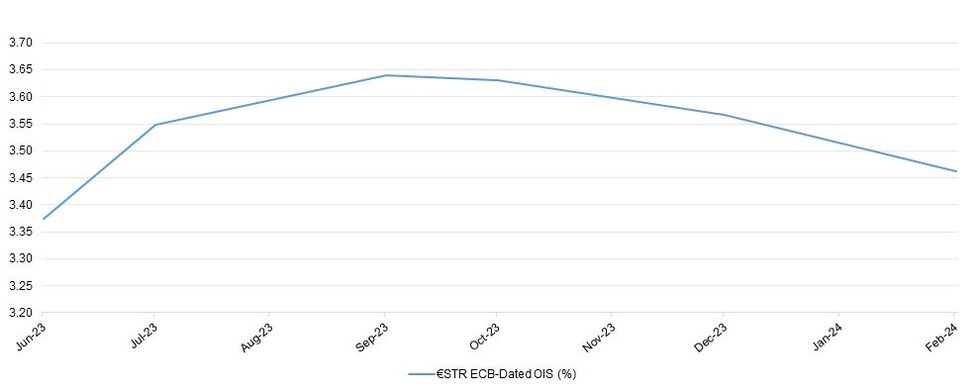

The ECB-dated OIS strip essentially hangs on to all of Friday’s modest upward repricing of terminal rate expectations, which was driven by FOMC-pricing related moves. That leaves a terminal ECB deposit rate of 3.75% more or less fully priced come the end of the Bank’s September gathering, followed by ~18bp of cuts being priced by February.

- Weekend ECB speak saw Vice President de Guindos point to the current monetary policy cycle moving into the home stretch, highlighting a meeting by meeting, data-dependent stance, while he also suggested that QT has led to a 60-70bp lift in government bond yields.

- Elsewhere, Bank of Italy chief Visco generally echoed de Guindos, while highlighting that there was too much uncertainty present to predict the Bank’s exact rate path.

- The two stuck to the dovish side of the spectrum, as is their norm.

- We also heard from Slovakian central bank chief Kazimir, who reaffirmed his recent hawkish line of rhetoric, warning of the potential for a longer than previously envisaged round of rate hikes.

- Bundesbank chief Nagel will speak later today, although he provided plenty of hawkish rhetoric recently, so don’t expect too much fresh policy steer from him.

| ECB Meeting | €STR ECB-Dated OIS (%) | Difference Vs. Current Effective €STR Rate (bp) |

| Jun-23 | 3.375 | +22.7 |

| Jul-23 | 3.549 | +40.1 |

| Sep-23 | 3.640 | +49.2 |

| Oct-23 | 3.631 | +48.3 |

| Dec-23 | 3.567 | +41.9 |

| Feb-24 | 3.462 | +31.4 |

Source: MNI - Market News/Bloomberg

Source: MNI - Market News/Bloomberg

MNI London Bureau | +44 0203-865-3809 | anthony.barton@marketnews.com

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok