Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

DATA REACT

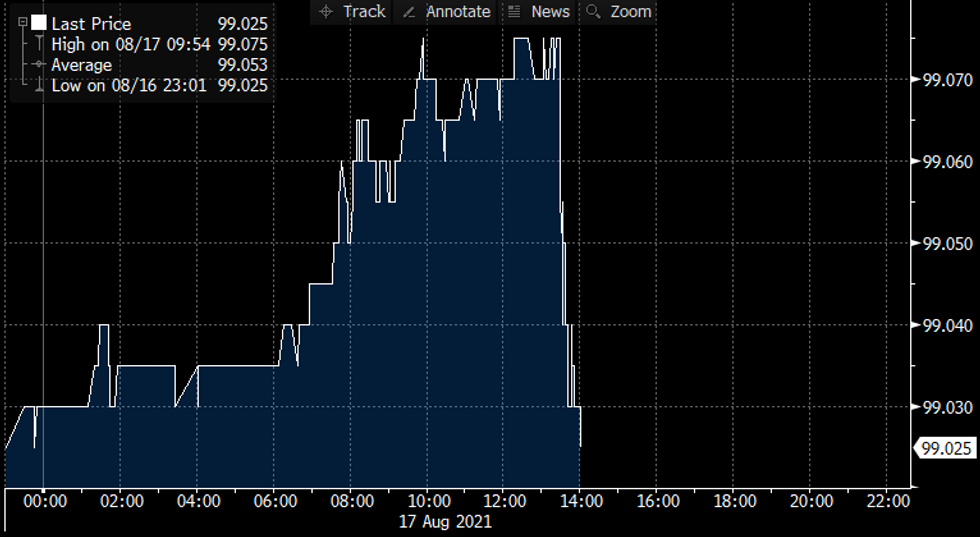

A somewhat baffling move in Treasuries following those retail sales figures, with weakness across the curve. 5Yrs underperforming as well, which is more consistent with the Fed bringing rate liftoff closer rather than pushing it farther away as you would expect with such a weak reading.

- Indeed, ED implied Dec23 rate hike pricing actually rose 4bp.

- Weak sales at motor vehicle and parts dealers (-3.9% M/M) was seen as the major culprit for the headline figure, but the ex-autos -0.4% figure shows it was a broadly weak report either way.

- July's was considered a "pre-Delta impact" reading with waning consumer confidence as seen in the latest UMichigan survey likely to impact sales to a greater degree in Aug and Sep. But it may reflect expiring fiscal transfers (including unemployment benefits ending in dozens of states).

- Consider also that CPI rose 0.5% M/M in July, so the "real" outturn was even worse.

- In other words, a very weak start to the 3rd quarter even before Delta's impact, and that's surely dovish for Fed liftoff timing.

- Earlier in the pandemic era, it used to be that a reaction like this on bad news was attributable to it actually being "good news" as it would spur more fiscal stimulus...not sure that is the case this time.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok