Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

US TSY SUMMARY: Reflation? Tell That To Bonds

Tsys traded weaker on Tue's open, gradual rebounding until Consumer Confidence, futures gapped lower after better than expected read 109.7 for March vs. 90.4 last month.- Tsys gradually rebounded, 30Y Bonds and Ultra-Bond futures making new session highs by noon. Couple long end block buys (+4,250 USM 154-31, buy through 154-28 post-time offer; +3,010 WNM1 182-28, buy-through 182--22 post-time offer) contributed to curves flattening while 2s-10s held lower levels after the bell.

- No unifying driver cited for continued carry-over weakness in rates, except for a reflation narrative that helped push yields to 1+ year highs late Feb into first half of March.

- Not market moving, Fed speak contributing to the reflation theme: Atlanta Fed Bostic: HOPEFUL THAT U.S. WILL SEE "LARGE" JOB NUMBERS IN COMING MONTHS, Bbg; and NY Fed Williams: SEES A STRONG U.S. ECONOMIC RECOVERY, Bbg. Aside, Pres Biden to deliver his "economic vision" from Pittsburg Wednesday (no set time).

- Month/quarter-end positioning and squaring ahead Friday's March employment data generated decent volumes on two-way flow. Tsy options downside insurance highlights: over +26,000 FVM 121/122/123 put flys, 9.5-10, FVM currently trading 123-14.5; wk1 TY midcurve put flys tactical buys for strong data Friday.

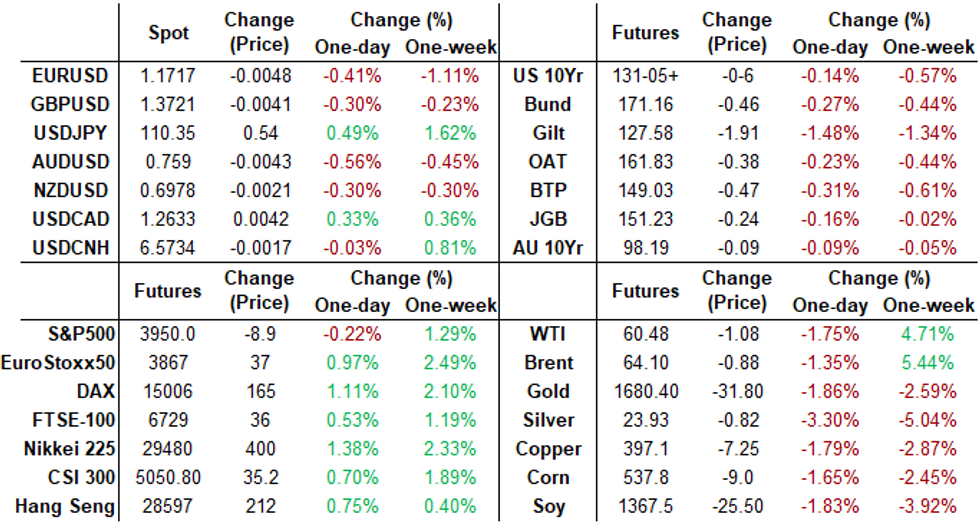

- The 2-Yr yield is up 0.6bps at 0.1465%, 5-Yr is up 1.9bps at 0.907%, 10-Yr is up 1.4bps at 1.7225%, and 30-Yr is down 1.5bps at 2.39%.

MONTH-END EXTENSIONS: Updated Barclays/Bbg Extension Estimates

Forecast summary compared to the avg increase for prior year and the same time in 2020. TIPS 0.01Y; Govt inflation-linked, 0.02. Note: Update MBS extension figure doubled from 0.12 prelim estimate while intermediate Gov climbed from steady.

| Estimate | 1Y Avg Incr | Last Year | |

| US Tsys | 0.08 | 0.09 | -0.03 |

| Agencies | 0.03 | 0.05 | -0.03 |

| Credit | 0.11 | 0.09 | 0.16 |

| Govt/Credit | 0.08 | 0.09 | 0.06 |

| MBS | 0.24 | 0.06 | 0.03 |

| Aggregate | 0.13 | 0.08 | 0.04 |

| Long Gov/Cr | 0.11 | 0.09 | 0 |

| Iterm Credit | 0.11 | 0.08 | 0.09 |

| Interm Gov | 0.08 | 0.08 | 0.01 |

| Interm Gov/Cr | 0.09 | 0.08 | 0.05 |

| High Yield | 0.15 | 0.1 | 0.12 |

SHORT TERM RATES

US DOLLAR LIBOR: Latest settles:

- O/N +0.00412 at 0.07700% (+0.00362/wk)

- 1 Month +0.00663 to 0.11513% (+0.00788/wk)

- 3 Month -0.00087 to 0.20163% (+0.00263/wk) (Record Low of 0.17525% on 2/19/21)

- 6 Month +0.00387 to 0.20675% (+0.00350/wk)

- 1 Year +0.00513 to 0.28663% (+0.00588/wk)

- Daily Effective Fed Funds Rate: 0.07% volume: $74B

- Daily Overnight Bank Funding Rate: 0.07%, volume: $252B

- Secured Overnight Financing Rate (SOFR): 0.01%, $858B

- Broad General Collateral Rate (BGCR): 0.01%, $348B

- Tri-Party General Collateral Rate (TGCR): 0.01%, $329B

- (rate, volume levels reflect prior session)

- TIPS 7.5Y-30Y, $1.199B accepted vs. $3.146 submitted

- Next scheduled purchases:

- Wed 3/31 1010-1030ET: Tsy 20Y-30Y, appr $1.750B

- Pause for Easter Holiday, Resume April 5:

- Mon 4/05 1100-1120ET: Tsy 0Y-2.25Y, appr $12.825B

US TSYS/OVERNIGHT REPO: 10s Heat Up Slightly

Overnight repo remains at special across the curve, heating up slightly in 10s. Current levels:

T-Bills: 1M 0.0025%, 3M 0.0025%, 6M 0.0355%; Tsy General O/N Coll. 0.02%.

| Duration | Current | Old Issue |

| 2Y | 0.00% | 0.02% |

| 3Y | -0.01% | -0.16% |

| 5Y | -0.18% | 0.02% |

| 7Y | -0.23% | 0.02% |

| 10Y | -0.23% | -0.15% |

| 30Y | -0.09% | -0.01% |

EURODOLLAR/TREASURY OPTIONS SUMMARY

Eurodollar Options:- +24,000 Green Apr 91 puts, 2.5

- Update, over +40,000 short Apr 96/97 put spds on day, 2.5

- +6,000 short Dec 97/98/100 call flys, 1.0

- +5,000 short Sep 93/95/96 put flys, 1.25/legs

- +10,000 Sep 97 puts, 1.25

- 3,000 Blue Jul 97.37 puts, 2.0

- 5,200 Blue Jun 85 puts, 19.0

- Overnight trade

- +9,000 Green Sep 83/86/88 put flys, 3.5 (+15k at 3.0 Mon)

- 6,275 Blue Apr 82 puts, 3.5

- +2,500 Blue Apr 86/87/88 call trees, 2.5

- 10,000 FVM 122/122.75 put spds, 9 on screen, still offered

- -3,000 TYM 128 puts, 14

- >+5,000 wk1 TY 130.25/130.75/131.25 put flys, 9

- +15,000 TYM 127 puts, 10-11

- -5,400 TYK 130.5 puts at 32

- -1,000 TYK 129/130/131/132 put condors, 24 still bid

- Update, over 26,000 FVM 121/122/123 put flys, 9.5-10, FVM currently trading 123-14.5

- >10,000 TYK 129/130 put spds, 5 in small pieces

- 5,000 TYM 127/128.5put spds, 9

- Overnight options

- +15,000 FVM 121/122/123 put flys, 9.5-10

- >20,000 TYK 131 puts, 51

- 4,000 TYM 128.5/130/131.5 put flys

- +2,000 TYK 133 calls, 8

- +4,000 wk1 TY 130.5/130.75/131.25 2x3x1 put flys, 10

- 2,000 USK 157 calls, 37

EGBs-GILTS CASH CLOSE: Reflation Narrative Maintains Steepening Pressure

The UK and German curves bear steepened yet again Tuesday as the reflation narrative has driven global core FI yields higher this week. Periphery spreads were little changed.

- EGBs mainly took their cue from US Treasuries, with 10-Yr yields hitting 14-month highs on expectations of strong US economic activity and further fiscal stimulus.

- Germany and Spain posted above-expected CPI prints in the morning. Upside surprises in French and Eurozone sentiment indicators added a bit of reflationary sentiment.

- That said, Bund and Gilt yields ended the session off the highs, with some citing month-end extension dynamics as a possible support.

- Wed sees EZ/French/Italian CPI and revised Q4 UK GDP in data, as well as German 15-Yr supply. A few speakers as well with ECB's Lagarde, Rehn, Visco and Villeroy appearing.

Closing yields/10-Yr Spreads to Bunds:

- Germany: The 2-Yr yield is up 1.7bps at -0.692%, 5-Yr is up 3.2bps at -0.625%, 10-Yr is up 3.2bps at -0.286%, and 30-Yr is up 2bps at 0.268%.

- UK: The 2-Yr yield is up 0.7bps at 0.074%, 5-Yr is up 2.3bps at 0.364%, 10-Yr is up 3.6bps at 0.824%, and 30-Yr is up 4.1bps at 1.36%.

- Italian BTP spread up 0.9bps at 96.6bps / Spanish down 0.2bps at 62.9bps

OPTIONS/EUROPE SUMMARY: Largely May/June Bund Structures

Tuesday's options flow included:

- DUM1 112.10/112.20/112.30c fly, bought for 2in 5k

- RXK1 170.5/169.5/168.5/167.5p condor, bought for 21.5 in 30k

- RXK1 168.50/173.50 strangle, sold at 23 in 1.5k

- RXK1 172.5/173.5 call spread bought for 12.5 in 5.5k

- RXM1 171.00/169.50/168.00p fly, bought for 26 in 1k

- RXM1 169.00/172.50 combo bought for 0 in 1.5k (+put, - call)

- RXM1 172.00/172.50/173.50 call fly bought for -1.5 in 1.7k

- 3RK1 100.25/100.12ps vs 0RK1 100.50/100.37ps x2, sold the blue at half in 4kx8k

- 3RM1 100.125/99.87/99.62p fly, bought for 1.5 in 2k

FOREX SUMMARY

Main story of the day for FX has been the continued better buying of the Dollar across the board.

- The Greenback is bid against all majors, but the SEK is now the worst performer down 0.65%, closely followed by the JPY on higher US yields, now down 0.53%, after Treasuries futures move off their lows.

- Next target in USDJPY is seen further out towards 110.63 0.764 proj of Mar - Apr 2020 rally from Jan 6 low

- Also note, that 110.67 is the May 2019 high

- EURUSD broke out lower and tested MNI tech support at 1.1711 (05/11 low), printed 1.1712 low at the time of typing.

- Cable is looking to test the figure at 1.3700, now at 1.3709.

- Further downside traction in Cable would open towards next support at 1.3670/63 Low Mar 25 / Low Feb 5.

- CHF is down 0.40% versus the Dollar, as safe haven FX loses ground with risk tilted to the upside.

- USDCHF trades at 0.9434, just off the session high at 0.9438 (at the time of typing).

- Looking ahead, Riksbank Ingves and Fed Williams are the speakers left on the calendar for today

FX OPTIONS: Expiries for Mar31 NY cut 1000ET (Source DTCC)

- EUR/USD: Apr01 $1.1850(E1.1bln-EUR puts); Apr06 $1.1800(E1.0bln); Apr08 $1.1700(E1.3bln), $1.1725(E3bln), $1.1800(E1.2bln), $1.1840-50(E1.2bln), $1.1900(E1.1bln)

- USD/JPY: Apr01 Y106.80-85($1.6bln-USD puts); Apr07 Y109.95-110.00($1.9bln); Apr08 Y108.45-55($1.3bln), Y108.60-70($1.5bln)

- NZD/USD: Apr09 $0.6948-50(N$1.1bln)

- USD/CAD: Apr01 C$1.2450($1.5bln), C$1.2600-10($1.3bln-USD puts), C$1.2660-75($1.2bln)

- USD/CNY: Apr02 Cny6.58($1.4bln); Apr07 Cny6.60($1.6bln)

PIPELINE: Deutsche Bank Launched, FRN Dropped

- Date $MM Issuer (Priced *, Launch #)

- 03/30 $2.5B #Pakistan $1B 5Y 6.0%, $1B 10Y 7.375%, $500M 30Y 8.875%

- 03/30 $1.5B *Dexia Credit 5Y +12

- 03/30 $1.2B *Jardine Matheson $800M 10Y +87.5, $400M 15Y 127.5

- 03/30 $750M #Deutsche Bank 4NC3 +112.5, 4NC3 FRN SOFR dropped

- 03/30 $Benchmark Chile 32Y Formosa/30Y +140a

COMMODITIES: Precious Metals Extend Lower Amid Buoyant Dollar

- Gold prices slipped beneath the $1,700 an ounce threshold for the first time since early March. The firmer dollar, rising on expectations that President Biden will launch efforts to secure a $4 trillion infrastructure package, has continued to weigh on precious metals.

- The latest decline in gold prices stands to bring the metal's loss to more than 11% so far this year. Spot fell to lows of $1,678.30 an ounce on Tuesday before paring some of that loss and residing down 1.6% as we approach the close. Technically, clearance of short-term supports has exposed $1676.9, Mar 8 low and the bear trigger.

- Silver continued to make fresh recent trend lows and has slumped 2.5% on Tuesday. Similarly, spot prices are approaching a key support at $24.057 – the Jan 18 low.

- Oil fell alongside the appreciating dollar as near-term risks to the demand recovery emerged ahead of an OPEC+ meeting this week to decide on output policy. WTI crude futures unwound yesterday's gains and briefly slipped under $60 a barrel before consolidating back above but posting losses of 1.8% on Tuesday.

- A panel of OPEC+ technical experts agreed to revise down oil-demand estimates for 2021 after Saudi Arabia suggested that the figure looked too high, delegates said. The move, which was also supported by Algeria, comes just days before the group meets to discuss production levels for May.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.