Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

US TSY SUMMARY: Follow the Bouncing Ball That Is Tsys

Choppy late session trade tied to month/quarter-end flows Wednesday, Tsys weaker but well off session lows from the closing bell, while equities pared gains after making new all-time highs in SPUs (ESM1 3983.75). Late chop exacerbated by thinning markets ahead Fri's March NFP (+650k est vs. +379k last for Feb) and participation heading into Easter holiday (early 1100ET close Fri).- Post-ADP Bounce: Tsy futures blipped higher after ADP private employ data came out a little less optimistic than estimated (+517k vs. +550k) with futures inside the

- overnight range on the open, curves mixed with short end steeper.

- Tsys inched off early lows into midday, loosely following equities, amid two-way trade, positioning ahead the extended holiday weekend, but reversed course/extended lows during the second half as equities plowed higher. Brief bounce in rates after French Pres Emmanuel Macron anncd will extend nationwide lockdown measures for the next four weeks.

- Tsys see-sawed lower yet again, making session lows on the bell (10YY 1.7494%H; 30YY 2.4289%H) -- only to gap higher on hevy volumes in the hour that followed with couple ultra-band Block buys adding impetus +2,000 WNM1 181-19, buy through 181-16 post-time offer; +3,500 WNM1 182-05 buy through 182-01 post-time).

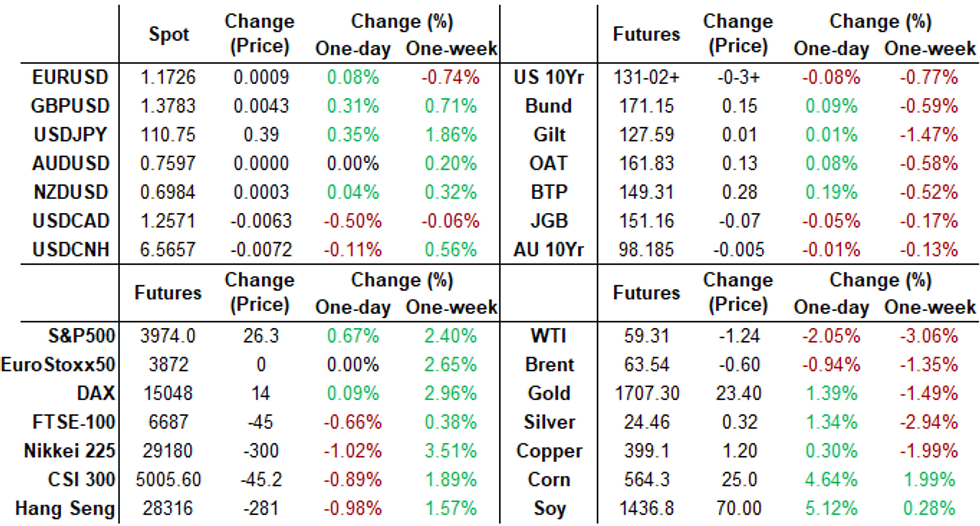

- The 2-Yr yield is up 1bps at 0.1564%, 5-Yr is up 3.1bps at 0.9264%, 10-Yr is up 2.9bps at 1.7315%, and 30-Yr is up 4bps at 2.4082%.

MONTH-END EXTENSIONS: Updated Barclays/Bbg Extension Estimates

Forecast summary compared to the avg increase for prior year and the same time in 2020. TIPS 0.01Y; Govt inflation-linked, 0.02. Note: Update MBS extension figure doubled from 0.12 prelim estimate while intermediate Gov climbed from steady.

| Estimate | 1Y Avg Incr | Last Year | |

| US Tsys | 0.08 | 0.09 | -0.03 |

| Agencies | 0.03 | 0.05 | -0.03 |

| Credit | 0.11 | 0.09 | 0.16 |

| Govt/Credit | 0.08 | 0.09 | 0.06 |

| MBS | 0.24 | 0.06 | 0.03 |

| Aggregate | 0.13 | 0.08 | 0.04 |

| Long Gov/Cr | 0.11 | 0.09 | 0 |

| Iterm Credit | 0.11 | 0.08 | 0.09 |

| Interm Gov | 0.08 | 0.08 | 0.01 |

| Interm Gov/Cr | 0.09 | 0.08 | 0.05 |

| High Yield | 0.15 | 0.1 | 0.12 |

SHORT TERM RATES

US DOLLAR LIBOR: Latest settles:

- O/N +0.00363 at 0.08063% (+0.00725/wk)

- 1 Month -0.00400 to 0.11113% (+0.00388/wk)

- 3 Month -0.00738 to 0.19425% (-0.00475/wk) (Record Low of 0.17525% on 2/19/21)

- 6 Month -0.00150 to 0.20525% (+0.00200/wk)

- 1 Year -0.00350 to 0.28313% (+0.00238/wk)

- Daily Effective Fed Funds Rate: 0.07% volume: $76B

- Daily Overnight Bank Funding Rate: 0.07%, volume: $246B

- Secured Overnight Financing Rate (SOFR): 0.01%, $808B

- Broad General Collateral Rate (BGCR): 0.01%, $338B

- Tri-Party General Collateral Rate (TGCR): 0.01%, $324B

- (rate, volume levels reflect prior session)

- Tsy 20Y-30Y, $1.734B accepted vs. $4.646 submitted

- Next scheduled purchase:

- Pause for Easter Holiday, Resume April 5:

- Mon 4/05 1100-1120ET: Tsy 0Y-2.25Y, appr $12.825B

US TSYS/OVERNIGHT REPO: 10s, 30s Heat Up, GC Decline

Overnight repo remains at special across the curve, heating up slightly in 10s. Current levels:

T-Bills: 1M -0.0025%, 3M 0.0152%, 6M 0.0304%; Tsy General O/N Coll. 0.01%.

| Duration | Current | Old Issue |

| 2Y | -0.01% | -0.01% |

| 3Y | -0.17% | -0.32% |

| 5Y | -0.02% | -0.25% |

| 7Y | 0.00% | -0.22% |

| 10Y | -0.50% | -0.23% |

| 30Y | -0.15% | -0.05% |

EURODOLLAR/TREASURY OPTIONS SUMMARY

Eurodollar Options:- Block, +14,000 short Mar 90/92 put spds 3 over 97 calls

- Block, 12,750 short Dec 95/96 put spds 3.0 over 97 calls, w/another 7,250 in pit

- +10,000 Jul 96/97 put spds 0.5 vs 99.815/0.10%

- Block, 13,159 short May 99.62/99.75 put spds, 3.5 vs. 99.725/0.50% at 1058:46ET

- +4,000 Green Jun 87/90 3x2 put spds, 11

- +2,500 Blue Sep 72/75 3x2 put spds, 4.0

- -15,000 Jun 99.875 calls cab

- +5,000 Mar 99.81/99.87 1x2 call spds, cab

- +4,500 Red Dec'22 85/87 put spds, 4.5

- -12,000 Jun 99.75/99.81 2x1 put spds, 2.0

- +5,000 short Mar 91/93 put spds 2.0 over 96/98 call spd vs. 99.415/0.45%

- Overnight trade

- Block, +10,000 Red Dec'22 95/96 put spds, 4.5 vs. 99.515/0.11% at 0740:16ET

- -6,000 TYM 127 puts, 11

- -2,500 TYM 129 puts, 27

- 8,00 TYM 127 puts, 10

- -3,750 TYM 131 puts, 101

- Block +12,000 wk2 FV 123.25 puts, 10.5 vs. 123-16/0.35%

- 4,000 USM 160 calls, 34-37

- +4,000 TYK 132 puts puts 13 over TYM 131 puts

- +5,000 TYK 130.5 puts 3-4 over TYM 129 puts

- +1,500 FVM 123.5 straddles, 106

- 10,000 TYK 132.5 calls, 14, volume on day >13.2k

- Update, over -18,000 TYM 129 puts 25-26

- +1,500 USK 152/154 put spds, 35-36

- Update, +8,200 FVK 123.75 puts, 7.5-8

- 2,000 TYK 133 straddles, 204

- -5,000 TYM 127/132.5 strangles, 39

- Overnight trade

- +15,000 TYM 127 puts, 10

- -5,000 TYM 129 puts 25-26

- +10,000 wk1 TY 131 puts, 17 ongoing (+10K late Tue 13-14)

EGBs-GILTS CASH CLOSE: Wary Of Tighter Lockdowns At Month-End

Curves traded mixed Wednesday with a combination of factors at play at various points in the session, including more stringent lockdown measures in Europe, lower-than-expected inflation data, and some degree of month-end buying. Gilts underperformed, fading quickly after hitting session highs mid-afternoon. Conversely, Bunds rallied from a weak open. Periphery spreads were mixed.

- Early data showed UK Q4 GDP revised higher, while FR, IT and EZ CPI was softer than expected.

- ECB Pres Lagarde said markets can test the ECB "as much as they want", as the bank has "exceptional tools".

- French Pres Macron is reportedly to announce tighter lockdown measures this evening, while Italy's set to extend restrictions to April 30 (from Apr 6th currently).

- Thu's pre-holiday session sees final Mar PMIs.

Closing yields/10-Yr Spreads to Bunds:

- Germany: The 2-Yr yield is up 0.1bps at -0.691%, 5-Yr is down 0.3bps at -0.628%, 10-Yr is down 0.6bps at -0.292%, and 30-Yr is down 1bps at 0.258%.

- UK: The 2-Yr yield is up 3bps at 0.104%, 5-Yr is up 3bps at 0.394%, 10-Yr is up 2.1bps at 0.845%, and 30-Yr is up 3.7bps at 1.397%.

- Italian BTP spread down 0.6bps at 96bps / Spanish spread unchanged at 62.9bps

OPTIONS/EUROPE SUMMARY: Long-Dated Euribor Features

Wednesday's options flow included:

- DUK1 112.20c, bought for 1.25 in 5k

- DUK1 112.20/112.10/112.00p fly, sold at 4 in 1.25k

- DUK1 112.10/112.20/112.30c fly, bought for 2 in 5k

- ERH3 100.87c, bought for 2.25 in 4k

- 3RN1 100/99.87ps, bought for 1 in 4k (ref 100.285, 7 delta)

- 0LU1 99.62/99.75/99.87c fly 1x3x2, bought for flat in 3.2k

- 3LM1 99.62/99.50/99.37p fly, sold at 1.25 in 3k

FOREX: JPY Seals Worst Monthly Performance since 2016

- JPY was comfortably the poorest performer Wednesday, helping buoy USD/JPY toward the Y111.00 handle. A break above this level would be the first since March, and could open another leg higher toward 2020's best levels at 112.23.

- The greenback started the session well, pressuring EUR/USD to new 2021 lows before month-end flow conspired against the greenback and boosted most major pairs into the month-end fix.

- At the upper end of the table, GBP outperforms as the contrast between the UK's approach to COVID lockdowns and the Eurozone widens further. Both France and Italy extended their domestic lockdowns Wednesday, leaving vaccine politics as a key issue headed into Q2.

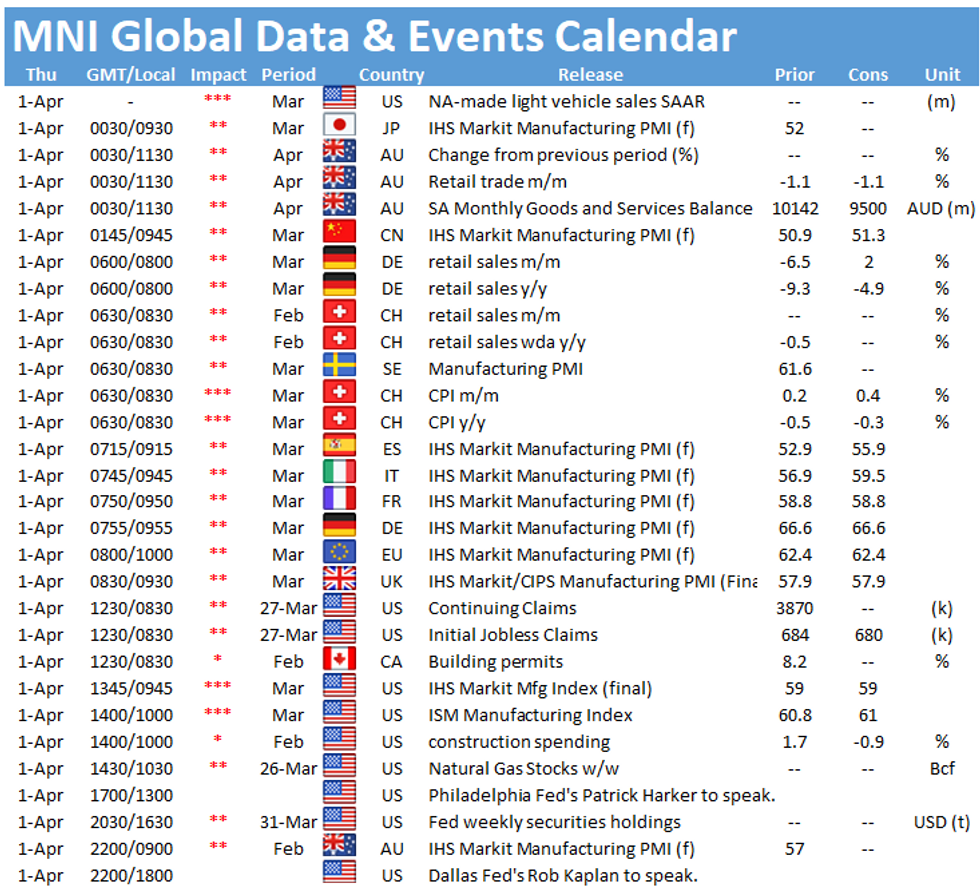

- Focus Thursday turns to Japan's Tankan survey, US weekly jobless claims and March ISM manufacturing. Thursday also marks the final full trading day of the week, with markets only seeing a limited open Friday.

Expiries for Apr01 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1850(E1.1bln-EUR puts)

- USD/JPY: Y106.80-85($1.6bln-USD puts), Y107.00($988mln), Y108.00($969mln), 108.90-00($660mln), Y109.35($585mln), Y110.00($532mln), Y111.00($645mln)

- USD/CAD: C$1.2450($1.5bln), C$1.2600-10($1.3bln-USD puts), C$1.2630-45($1.1bln), C$1.2660-75($1.2bln)

- USD/CNY: Cny65475($750mln)

PIPELINE: Rounding Out March With $232.62B High-Grade Debt Issuance

Modest issuance ahead Easter Holiday, March still leads 2021 with stellar $232.62B high-grade corporate issuance vs. $157.865B in February and $227.55B in January. March 2020 saw $275.48B corporate debt issued -- second to all-time record of $401.325B in April 2020.

- Date $MM Issuer (Priced *, Launch #)

- 03/31 $1B *Ooredoo Qatar 10Y +100

- 03/31 $1B Goodyear 10Y 5.25%a, 12Y 5.625%a

- 03/31 $500M #Element Fleet 3Y +130

- 03/31 $500M #Inversiones CMPC 10Y +135

EQUITIES: S&P 500 Strikes New Record Ahead of Biden's Economic Plan

- Markets shrugged off the prospect of higher corporation taxes Wednesday, with the S&P 500 hitting a new record high - fuelled by solid gains in the tech and consumer discretionary sectors. Communication services and healthcare also traded well, while energy and financials lagged.

- Stronger tech names resulted in outperformance for the NASDAQ, while the Dow Jones Industrial Average sat just above unchanged. Persistent equity strength weighed on the VIX, which holds close to the late March lows (thereby closing the pandemic-inspired gap higher in late Feb'20).

- In Europe, stocks were softer, with UK's FTSE-100 leading losses after a 0.9% drop. German stocks fared slightly better, closing unchanged on the day.

COMMODITIES: Softer Dollar Prompts Bounce In Precious Metals

- Gold prices recovered back above the $1,700 mark as broad dollar indices came under pressure leading up to the WMR month end fix.

- The softer greenback provided a welcome relief rally for spot gold and silver, both of which took a substantial hit to begin the week. Technical support at $1676.9, Mar 8 low and the bear trigger held overnight and aided dip buyers ahead of the long holiday weekend.

- Gold and Silver recovered just shy of 2% but the latter still resides down 2.5% on the week and down roughly 10% for the month of March.

- Opec+ meetings continued where Secretary General Barkindo said that the economic environment "remains challenging, complex and uncertain, with the market volatility we have witnessed in the last two weeks of March a reminder of the fragility facing economies and oil demand."

- Crude futures gave up modest gains late in the session to trade down just over 1% on the comments.

- Correspondent Amena Bakr stated it was not an upbeat JMMC and that concerns were expressed over compliance and the compensation cuts plans.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.