Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

US TSY SUMMARY: More Pain Trade for Rate Bears

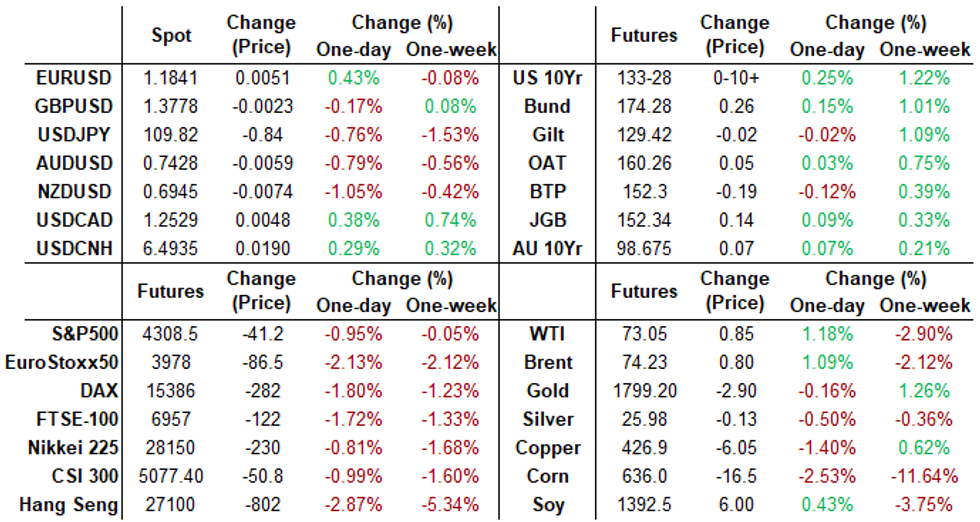

Another day of pain for staunch shorts willing or able to hold onto positions. Yields receded to levels not seen since early Feb, 30YY fell to 1.8551% low, 1.8852% last; 10YY 1.2479% low and testing 200DMA before paring back midday.

- Coincidentally, Tsys peaked/started to recede around time ECB strategy review released (in-line: adopting symmetric 2% inflation target expected).

- No immediate reaction to weekly claims climbing 2k to 373k -- higher than est of +350k, while continuing claims recedes slightly (-.145M to 3.339M vs. 3.35M exp).

- Both rates and equities are traded back near the middle of their respective ranges after the rates closing bell: Tsys but well off highs (5s30s yield curve actually a little steeper on day at 117.129 (+1.395) while equities were weaker ESU1 -43.0 at 4306.75 vs. 4279.25 low.

- Heavy volumes traded on day with lions share of TYU1 1.75M occurring before midday. Heavy option volumes with call skew outpacing puts for first time in over a year. Nevertheless, willing put buyers and existing long put positions continued to fade the underlying rally.

- The 2-Yr yield is down 2.4bps at 0.1904%, 5-Yr is down 4.3bps at 0.7356%, 10-Yr is down 3bps at 1.2862%, and 30-Yr is down 2.9bps at 1.9091%.

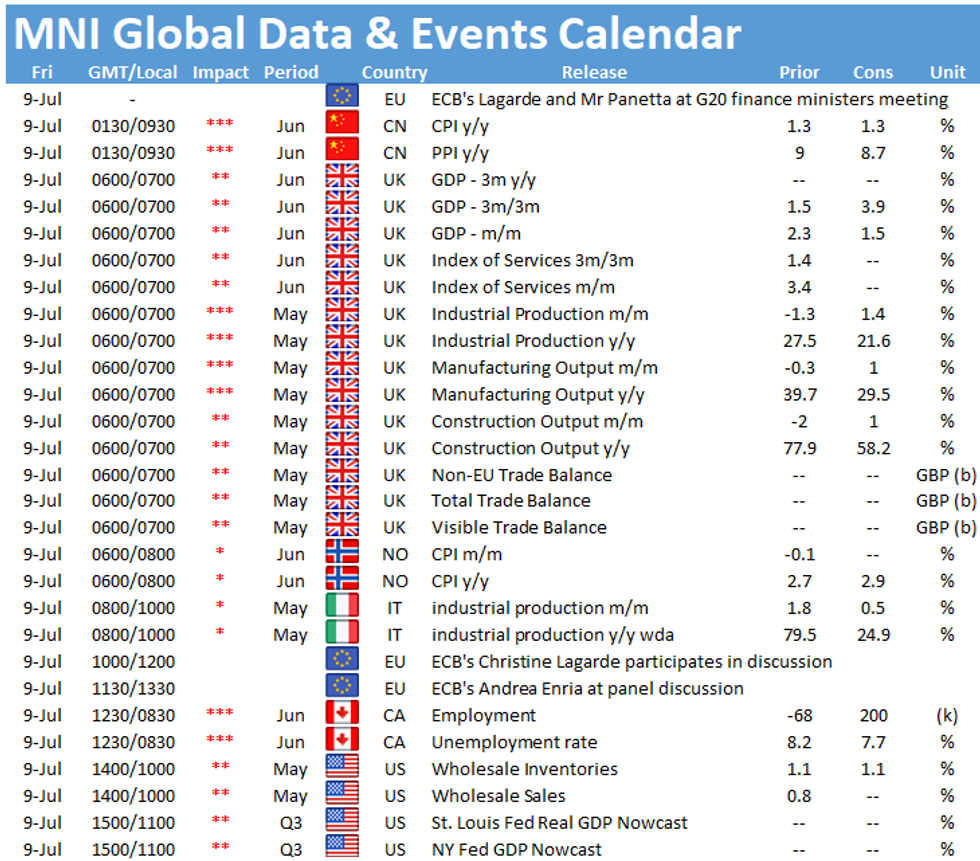

- Friday focus on Wholesale Inventories/sales. No data Monday with June CPI data not until next week Tuesday: MoM (0.6%, 0.5% est); Ex Food and Energy MoM (0.7%, 0.4% est).

SHORT TERM RATES

US DOLLAR LIBOR: Latest Settles

- O/N +0.00100 at 0.08613% (+0.00563/wk)

- 1 Month -0.00250 to 0.10038% (-0.00250/wk)

- 3 Month -0.00488 to 0.11900% (-0.01888/wk) ** (Record Low: 0.11800% on 6/14)

- 6 Month -0.00525 to 0.15700% (-0.00600/wk)

- 1 Year -0.00150 to 0.23888% (-0.00563/wk)

- Daily Effective Fed Funds Rate: 0.10% volume: $77B

- Daily Overnight Bank Funding Rate: 0.08% volume: $247B

- Secured Overnight Financing Rate (SOFR): 0.05%, $905B

- Broad General Collateral Rate (BGCR): 0.05%, $360B

- Tri-Party General Collateral Rate (TGCR): 0.05%, $325B

- (rate, volume levels reflect prior session)

- Tsy 2.25Y-4.5Y, $8.401B accepted vs. $26.791B submission

- Next scheduled purchases:

- Fri 7/9 1010-1030ET: Tsy 22.5Y-30Y, appr $2.025B

FED: Repo and Reverse Repo Operations

NY Fed reverse repo usage climbs to $793.399B from 72 counterparties vs. $785.720B on Wednesday. Remains well shy of record high of $991.939B on June 30.

EURODOLLAR/TREASURY OPTIONS SUMMARY

Eurodollar Options:- Update, over +50,000 short Dec 93/95/96 put flys, 2.0

- +10,000 Blue Mar 80 puts, 9.5

- -5,000 Blue Sep 80/85 put spds, 5.0

- +4,500 Sep 99.81/99.87 put spds, 1.25

- +15,000 Blue Jul 85/86 put spds, 1.5

- +5,000 short Dec 99.18/99.43 2x1 put spds, 1.0

- -3,000 Blue Jul 98.75/98.87 call spds, 3.0

- -2,500 Green Sep 90 puts, 6.5 vs. 99.125/0.34%

- +10,000 Blue Sep 80/82/85 put flys, 2.75

- -2,000 Green Oct 90 straddles, 29.5

- -10,000 short Sep 95/96/97 put flys, 3.25

- Overnight trade

- +22,000 short Dec 93/95/96 put flys, 2.0

- 5,750 short Mar 99.12/99.37 put spds

- 6,300 Gold Dec 97.87/98.12 put spds

- 4,000 Gold Oct 97.87/98.12 put spds

- Block, 10,000 long Green Dec'23 88/90/92 call trees, 14.0/2-legs over

- Block, 10,000 long Green Mar 99.25 calls, 22.0

- Block, 3,787 Blue Aug 98.87/99.00 4x5 call spds, 10.5

- Block, 3,787 Blue Aug 98.87/99.00 4x5 call spds, 10.0

- +5,000 USU 173/176 1x2 call spds, 2 cr

- -1,600 TYU 133.5/134 strangles, 136-135

- -3,500 FVU 124.25 straddles, 58.5

- 3,500 FVU 123/123.25/123.5/123.75 put condors

- +5,000 TYQ 132.5/133.5 put spds, 15

- -2,500 TYU 136 calls, 13

- -2,500 TYU 136.5 calls, 9

- +20,000 TYU 133 puts, 12 pushes volume over 35k

- +13,000 TYU 135.5 calls 18-19

- -2,000 TYQ 134 calls, 24

- -5,000 TYU 133.5/134 put spds, 15

- 5,500 TYU 130.5/132/133.5/134 put condors, 1

- -3,500 TYU 136 calls 15

- -2,500 TYU 134 calls, 50

- Overnight trade

- 10,000 TYU 136 calls, 16

- 5,000 TYQ 132/132.25/132.75 put trees, 2

- 2,000 TYU 131.5/132/132.5/133 put condors

- 7,500 FVQ 124.75 calls, 2.5-3.5

- 3,000 FVU 122.75 puts, 6.5

- 2,500 FVU 121.25/122.25/123.25 put flys

- -3,000 USQ 161.5 puts, 16-15

EGBs-GILTS CASH CLOSE: Morning Rally Reverses

Bunds and Gilts staged a huge reversal over the course of the afternoon session, with yields coming off multi-month lows and bull flattening reversing.

- Periphery spreads widened over the entire session though, which was very much risk-off with several European equity indices dropping 2+% on global growth concerns.

- The ECB unveiled the conclusions of its strategy review, which says in part that the central bank will adopt a symmetric 2% inflation target (implying overshoots will be allowed). However this was not seen as market-moving, as the conclusions were largely anticipated well in advance.

- Ireland sold E1.5bln of IGBs, concluding European bond supply this week.

- We'll get multiple ECB speakers Friday, plus the delayed publication of the June meeting accounts. UK GDP is Friday's data focus.

Closing Yields / 10-Yr Periphery EGB Spreads To Germany

- Germany: The 2-Yr yield is down 0.7bps at -0.683%, 5-Yr is down 0.9bps at -0.603%, 10-Yr is down 0.9bps at -0.307%, and 30-Yr is down 0.4bps at 0.183%.

- UK: The 2-Yr yield is up 2.3bps at 0.085%, 5-Yr is up 0.9bps at 0.264%, 10-Yr is up 1.2bps at 0.612%, and 30-Yr is up 0.7bps at 1.128%.

- Italian BTP spread up 3.1bps at 107bps / Spanish spread up 2.7bps at 65.5bps

OPTIONS/EUROPE SUMMARY: Mix Of Rates Structures

Thursday's options flow included:

- RXU1 172/170.5/169p fly, bought for 10.5 in 4k

- DUQ1 112.30c bought for 1 in 3k

- DUU1 112.20/112.10^^, sold at 6.5 in 2

- 2RH2 100.25/100.37cs 1x1.25, vs 100.125p, bought cs for 2.75 up to 3.5 in 15k

- 3RU1 100.37c, bought for 1.75 in circa 7.2k (ref 100.29)

- 3RU1 100.12/00/87/75p condor, bought for 2 in 3.5k

- 3RZ1 99.62p bought for 1 in 3.6k

- 0LZ1 99.50/99.62/99.75c fly, bought for 3.5 in 5k

FOREX: Souring Sentiment Prompts Further Haven Demand

- A volatile Thursday for G10 currencies where safe haven demand continued to dominate the price action.

- In particular, JPY and CHF were favoured, with some significant intraday moves in the crosses.

- USDJPY had a large 117 pip range after breaking the most recent lows through 110.40 during European hours. A quick acceleration down to 109.80 was briefly consolidated before extending throughout the US session to print fresh lows at 109.53. A small recovery after the WMR fix, sees the pair around 109.85 heading into the close. USDCHF remains 1.04% lower.

- With the move very much tied to risk sentiment waning, AUD, NZD and CAD all suffered.

- NZDJPY has had the most significant move, down 1.69%, closely followed by AUDJPY, down 1.37% amid the pressure in equities.

- EURUSD performed well, rising back above the 1.18 mark and gradually climbing around half a percent on the day to near 1.1850. Once again strong demand for EUR crosses, particularly against NZD and AUD, explain the outperformance.

- Despite oil snapping its losing streak, EURNOK gained a further 1.25% to trade above 10.40 for the first time since early March.

- On Friday, markets will await the rescheduled ECB Monetary Policy Meeting Accounts, however, Canadian Employment will headline the data docket.

FOREX/Expiries for Jul09 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1780-00(E1.5bln), $1.1830-50(E1.5bln), $1.1875(E658mln), $1.1885-00(E1.6bln)

- USD/JPY: Y111.10-25($938mln)

- AUD/USD: $0.7500(A$575mln), $0.7550(A$754mln)

- USD/CAD: C$1.2350($600mln)

PIPELINE: Dexia, Mitsubishi Issued

- Date $MM Issuer (Priced *, Launch #)

- 07/08 $1B *Dexia no-grow 3Y +8

- 07/08 $500M #Mitsubishi Corp 5Y +75a

- $13.45B Priced Wednesday

- 07/07 $5B *KFW 3Y -3

- 07/07 $4B *Enel Fin $1.25B 5Y+70, $1B 7Y+85, $1B 10Y+100, $750M 20Y+110

- 07/07 $1.2B *Xiaomi $800M 10Y +165, $400M 30Y +220

- 07/07 $1B *PacifiCorp 31Y Green +98

- 07/07 $1B *Gazprom 10Y 3.5%

- 07/07 $750M *Royal Bank of Canada 5Y Green +38

- 07/07 $500M *EIB 7Y FRN/SOFR+25

EQUITIES: Stocks Sour as Buy-The-Dip Fails to Materialize

- As was the case on both Tuesday and Wednesday, equities saw a sharp spell of weakness following the open, although the dip seemed to stick into the close, with the S&P 500 off around 0.8%.

- The sharp bull flattening of the US Treasury curve worked against the banking sector, with financials the worst performer in the US. Materials and industrials also traded poorly, with energy the only sector to hold above water.

- The sell-off in stocks managed to underpin the VIX, which saw support and briefly showed above 20 points.

- European markets underperformed their US counterparts, with Italian, Spanish stocks sinking over 2.25% apiece. The FTSE-100 was partially shielded from losses but still closed off 1.7%.

COMMODITIES: Oil Snaps Losing Streak on Sharp DoE Draw

- After several sessions of losses, WTI and Brent crude futures managed to hold onto positive territory Thursday as the market bias switched to short-covering, helped by a much larger-than-expected draw in crude oil inventories.

- The headline crude oil inventories number saw a near 7mln bbls draw on reserves vs. expectations of just 4.5mln bbls. Similarly, NatGas also saw solid gains on a much smaller than expected build in reserves, of just 16 BCF.

- Gold maintains a firmer tone. Attention is on the 50-day EMA that intersects at $1814.6. A clear break of the EMA is required to suggest scope for a stronger rally. This would open $1833.7, 50.0% of the Jun 1 - 29 decline.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok