Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

US TSY SUMMARY: Bond Bear Reprieve

Bond bears see some relief from the week's rally back to mid-February levels, 10Y futures rejecting a bull channel top, 10YY off 200DMA. No data to speak of: US MAY WHOLESALE INV 1.3%; SALES 0.8%.- Rates trade near late session lows after the bell with equities near highs as the week's risk-off tone ebbed: not that any single factor behind the week's rally had really changed -- Covid-19 Delta variant remains as much a concern as ever, Asia market slow-down, fading stimulus tail winds, etc.

- Parallel with technicals, traders posited markets had come too far/too fast after return from extended holiday weekend. Return of Tsy coupon supply early next week contributing to sell pressure (3s and 10Y re-open on Monday, 30Y on Tuesday).

- Focus also on "big-6" bank earnings next week: JPM and GS Tuesday, BoAML, Citi and Wells Fargo Wednesday, MS Thursday.

- Option traders reported continued interest in buying downside puts, hedging for modest rate hike positioning in mid 2023-2024.

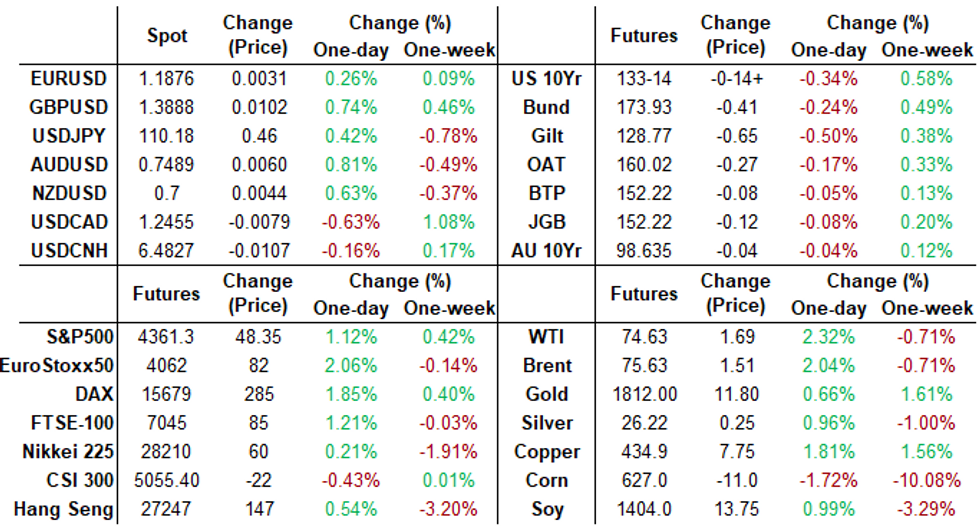

- The 2-Yr yield is up 2bps at 0.2146%, 5-Yr is up 4.5bps at 0.7866%, 10-Yr is up 6.3bps at 1.3561%, and 30-Yr is up 5.7bps at 1.9836%.

SHORT TERM RATES

US DOLLAR LIBOR: Latest Settles

- O/N +0.00050 at 0.08663% (+0.00613/wk)

- 1 Month -0.00025 to 0.10013% (-0.00275/wk)

- 3 Month +0.00963 to 0.12863% (-0.00925/wk) ** (Record Low: 0.11800% on 6/14)

- 6 Month -0.00600 to 0.15100% (-0.01200/wk)

- 1 Year +0.00000 to 0.23888% (-0.00563/wk)

- Daily Effective Fed Funds Rate: 0.10% volume: $76B

- Daily Overnight Bank Funding Rate: 0.08% volume: $256B

- Secured Overnight Financing Rate (SOFR): 0.05%, $874B

- Broad General Collateral Rate (BGCR): 0.05%, $364B

- Tri-Party General Collateral Rate (TGCR): 0.05%, $331B

- (rate, volume levels reflect prior session)

- Tsy 22.5Y-30Y, $2.001B accepted vs. $4.781B submission

- Next scheduled purchases:

- Mon 7/12 1010-1030ET: TIPS 1Y-7.5Y, appr $2.025B

- Tue 7/13 1010-1030ET: Tsy 4.5Y-7Y, appr $6.025B

- Wed 7/14 1010-1030ET: Tsy 10Y-22.5Y, appr $1.425B

- Wed 7/14 1500ET Update NY Fed Operational Purchase Schedule

FED: Reverse Repo Operations

NY Fed reverse repo usage recedes to $780.596B from 68 counterparties vs. $793.399B on Thursday. Compares to record high of $991.939B on June 30

EURODOLLAR/TREASURY OPTIONS SUMMARY

Eurodollar Options:- -7,000 Red Dec 98.87 puts, 5.0

- +4,000 short Mar 99.87 calls, 1.0

- +2,000 Gold Sep 97.75/98.00 3x2 put spds 1.0 over 4,000 Gold Sep 99.0 calls

- +10,000 Blue Dec 97.25 puts, 1.0

- Block, 12,414 short Sep 95/96/97 put flys, 3.5 vs. 99.62/0.25%

- +7,500 Green Jul 99.25/99.31/99.43/99.56 call condors

- +5,000 short Sep 95/96 2x1 put spds, 0.5

- Overnight trade

- +10,000 Blue Sep 97.75/98.00 put spds, 1.0 vs. 99.10-.095/0.05%

- 7,500 Green Aug 98.93 puts vs. Green Sep 98.81/98.93, 0.0 net

- -4,000 TYU 130/131.5 put spds, 11.0 vs. 133-16/0.05%

- -10,000 TYU 131.5/135 strangles, 34-33

- Update, > 11,000 FVQ 123.5 puts, 4-5, mostly 5

- -1,500 TYU 135.5/TYQ 134.5 call spds, 6

- -2,000 TYU 134.5/135.5 call spds, 15

- -2,500 TYU 132/134 call spds, 114

- -1,500 TYQ 132/134 1x2 call spds, 105

- -3,000 TYQ 134.5 calls, 6

- -2,000 USQ 167 calls, 10 vs. 162-26/0.10%

- +1,000 USQ 162/USU 160 put calendar spds, 18-19

- +5,000 USQ 163 calls, 62 vs. 162-22/0.46%

- +8,000 FVU 122.5/123.5 put spds, 12

- +4,000 wk3 TY 133 puts, 10-9

- Overnight trade

- 5,300 TYU 130 puts, 6

- 1,600 USU 174 calls

EGBs-GILTS CASH CLOSE: Another Bullish Week Ends On Bearish Note

Thursday's sharp fall in Gilt and Bund yields reversed completely on Friday - but nonetheless FI ended stronger for the 2nd consecutive week.

- The UK and German long-ends underperformed in a bear-steepening move as the multi-day rally took a breather, no particular macro / headline catalyst seen.

- In a generally risk-on session, with equities gaining, periphery spreads tightened, though Italian 10Yr spreads didn't quite make up all of Thursday's lost ground vs Bunds.

- UK May GDP data and Italy May IP data came in weaker than expected.

- Next week's calendar highlights largely surround the UK: BoE speeches (Bailey and Ramsden) and employment / CPI data.

Closing Yields / 10-Yr Periphery EGB Spreads To Germany

- Germany: The 2-Yr yield is up 0.7bps at -0.676%, 5-Yr is up 0.7bps at -0.596%, 10-Yr is up 1.4bps at -0.293%, and 30-Yr is up 2.3bps at 0.206%.

- UK: The 2-Yr yield is up 0.2bps at 0.087%, 5-Yr is up 3.1bps at 0.295%, 10-Yr is up 4.3bps at 0.655%, and 30-Yr is up 4.5bps at 1.173%.

- Italian BTP spread down 1.4bps at 105.6bps / Spanish down 0.8bps at 64.7bps

OPTIONS/EUROPE SUMMARY: Large Bund Structures

Friday's options flow included:

- RXU1 172.50p vs RXQ1 175.50c, bought the Sep for 34 in 1.5k

- Bund package: RXU1 168.5p, bought for 4 in 2.5k / RXU1 169.5/167.5ps, bought for 4.5 in 2.5k / RXU1 172.5/171.5ps 1x2, bought for -4 in 2.5k

- RXQ1 172p sold in 25k vs RXU1 173p bought in 22.5k vs 175.5c sold in 30k,traded from -2 to flat for the structure (put vs Risk Reversal)

- RXQ1 172p, bought for 4 in 5k

- OEQ1 134.75c, sold at 6.75 in 2k

- 2RZ1 99.87/99.75/99.62p fly 1x1.5x0.5, bought for 0.25 in 4k

- 0LU1 99.75/99.87cs, bought for 0.75 in 7k

FOREX: Equity Bounce Works Against Greenback & Haven FX

- Currency markets were the follower rather than the leader Friday, with the sharp bounce off the week's lows in equity markets helping fuel cross-asset risk sentiment. This resulted in the e-mini S&P topping out at new alltime highs as traders watch incoming earnings reports due next week.

- Global equity strength worked against the greenback, with the USD index off around 0.5% from the week's highs. Haven currencies also partially reversed the week's strength, with USD/JPY back above Y110 and EUR/CHF back above 1.0850. The conviction behind these recoveries could be key going forward, as market focus shifts to the US CPI report on Wednesday.

- The recovery rally in GBP/USD looked relatively one-way until the WMR fix, which saw the pair come under sharp selling pressure, with close to £700mln notional in futures contracts changing hands inside 5 minutes. The heavy volume knocked the rate off 1.3877 to trade either side of 1.3850.

- US, UK and German inflation data takes focus in the coming week, as well as the beginning of Q3 US earnings season and a raft of Chinese GDP, retail sales and industrial production data. Rates decisions from the Canadian, Turkish, Japanese and South Korean central banks also cross.

FOREX/Expiries for Jul12 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1930-35(E528mln)

- USD/JPY: Y109.00($500mln), Y109.30-50($669mln), Y110.00($705mln)

- AUD/USD: $0.7400(A$627mln), $0.7500(A$758mln)

- USD/CAD: C$1.2360-68($870mln), C$1.2500($610mln), C$1.2505-25($1.5bln), C$1.2575($500mln), C$1.2695-05($1.1bln)

- USD/CNY: Cny6.4530($560mln)

PIPELINE: $22.95B Total High-Grade Issuance

- Date $MM Issuer (Priced *, Launch #)

- 07/09 No new issuance Friday; $22.95B total for week

- $1.5B Priced Thursday

- 07/08 $1B *Dexia no-grow 3Y +8

- 07/08 $500M *Mitsubishi Corp 5Y +50

EQUITIES: Equities Heave Back to ATH

- All three major US indices traded solidly Friday, showing above the week's best levels to print a new alltime high.

- The S&P 500 was buoyed by a resurgence in financials, with a steepening Treasury curve helping support as markets look ahead to the beginning of Q3 earnings season.

- Banks are the first focus, with Goldman Sachs, JPMorgan, BofA, BlackRock, Citi and Wells Fargo among others all due to report. (Full timetable with timings, EPS and revenue expectations here: https://roar-assets-auto.rbl.ms/documents/10738/MN... )

- European indices were similarly strong, with France's CAC-40 surging over 2% into the close, closely followed by the EuroStoxx50 and Italy's FTSE-MIB.

COMMODITIES: Crude Extends Recovery, But Cycle Highs Out of Sight For Now

- Both WTI and Brent crude futures traded well Friday, with WTI showing back above the $74.50/bbl level, while Brent traded just above $75.50/bbl. Gains in energy markets were built on the back of yesterday sharp draw in crude oil and gasoline inventories, indicative of the solid demand for fuel products as the US economy reopens.

- The recovery saw further support from the faltering greenback Friday, which put the USD Index over 0.5% off the week's best levels. Despite the bounce in oil, focus remains on the downside, with Brent eyeing $71.24, the Jun 17 low. Similarly, WTI has cleared its 20-day EMA, opening losses toward $69.54, Jun 17 low.

- Gold maintains a firmer tone. Attention is on the50-day EMA that intersects at $1814.1. A clear break of the EMA is required to suggest scope for a stronger rally. This would open $1833.7, 50.0% of the Jun 1 - 29 decline.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok