Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

US TSY SUMMARY:

Rates see-sawed higher Friday, modest two-way action after early data, while chunky two-way flow going into the close saw better month-end selling as futures pared gains slightly.- Not exactly unexpected US/China headlines lent a small bid to Tsys pre-open: U.S. PAUSES IPO REGISTRATIONS FOR CHINESE COMPANIES: RTRS.

- Rates saw some fast two-way flow after PCE came out softer than anticipated (+0.5% vs. 0.6% est; core +0.4% vs. 0.6% est), levels moving off early session highs on moderate volume.

- StL Fed Bullard first to exit blackout said "MARKETS `VERY MUCH READY FOR A TAPER' TO START IN FALL".

- Tsys came under late sell pressure in the lead-up to the close, apparently month-end related amid chunky two-way flow as volume jumps appr 200k in TYU to 1.23M after the bell. Bonds off initial lows.

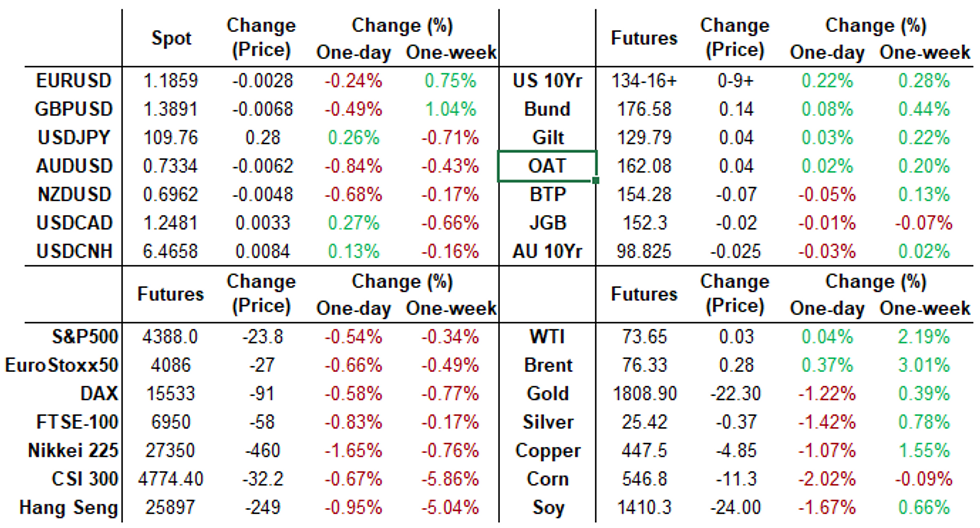

- Yield curves held mostly flatter all day. The 10YY still inside 1.29 to 1.22% range all week. The 2-Yr yield is down 1.8bps at 0.1859%, 5-Yr is down 3.8bps at 0.6967%, 10-Yr is down 4.2bps at 1.2273%, and 30-Yr is down 3.5bps at 1.8845%.

MONTH-END EXTENSIONS: Updated Barclays/Bbg Extension Estimates for US

Updated forecast summary compared to avg increase for prior year and same time in 2020. TIPS 0.14Y; US Gov inflation-linked 0.23Y. Note, MBS extension nearly doubled from 0.08Y preliminary to 0.15.

| SECURITY | Estimate | 1Y Avg Incr | Last Year |

| US Tsys | 0.08 | 0.09 | 0.09 |

| Agencies | 0.09 | 0.04 | 0.05 |

| Credit | 0.06 | 0.12 | 0.08 |

| Govt/Credit | 0.07 | 0.1 | 0.08 |

| MBS | 0.15 | 0.07 | 0.06 |

| Aggregate | 0.09 | 0.09 | 0.08 |

| Long Gov/Cr | 0.07 | 0.09 | 0.07 |

| Iterm Credit | 0.07 | 0.1 | 0.08 |

| Interm Gov | 0.08 | 0.08 | 0.08 |

| Interm Gov/Cr | 0.08 | 0.09 | 0.08 |

| High Yield | 0.09 | 0.11 | 0.1 |

SHORT TERM RATES

US DOLLAR LIBOR: Latest Settles

- O/N -0.00250 at 0.07688% (-0.00325/wk)

- 1 Month -0.00525 to 0.09050% (+0.00438/wk)

- 3 Month -0.00800 to 0.11775% (-0.01113/wk) ** (Record Low: 0.11800% on 6/14)

- 6 Month -0.00075 to 0.15313% (-0.00538/wk)

- 1 Year -0.00187 to 0.23513% (-0.00625/wk)

- Daily Effective Fed Funds Rate: 0.10% volume: $70B

- Daily Overnight Bank Funding Rate: 0.08% volume: $253B

- Secured Overnight Financing Rate (SOFR): 0.05%, $877B

- Broad General Collateral Rate (BGCR): 0.05%, $377B

- Tri-Party General Collateral Rate (TGCR): 0.05%, $341B

- (rate, volume levels reflect prior session)

- Tsy 2.25Y-4.5Y, $8.401B accepted vs. $21.043B submission

- Next scheduled purchases

- Mon 8/02 1100-1120ET: TIPS 7.5Y-30Y, appr $1.225B

- Tue 8/03 1010-1030ET: Tsy 10Y-22.5Y, appr $1.425B

- Wed 8/04 1100-1120ET: Tsy 7Y-10Y, appr $3.225B

- Thu 8/05 1010-1030ET: Tsy 22.5Y-30Y, appr $2.025B

- Fri 8/06 1010-1030ET: Tsy 0Y-2.25Y, appr $12.425B

FED: Reverse Repo Operations -- Record High, Over $1T

NY Fed reverse repo usage climbs to new record high, first time over $1T: $1,039.394B from 86 counterparties vs. $987.283B on Thursday. Compares to prior record high of $991.939B on June 30.

EURODOLLAR/TREASURY OPTIONS SUMMARY

Eurodollar Options:- +3,000 short Sep 99.62 puts, 1.5

- +15,000 Green Mar 100 calls, 1.0 vs. 99.045 -.5/0.05%

- Overnight trade

- 4,100 Sep 99.81/99.87 put spds

- 3,000 Green Aug 99.12 puts

- 2,500 wk1 TY 134.5/135 1x2 call spds, 3

- 2,000 wk1 TY 134.5/135 2x1 put spds, 2

- Update, over 60,000 TYU 133.5 puts, 19-18

- over 20,000 TYU 132.5 puts 8-9

- Overnight trade

- 12,000 TYU 132.5 puts, 8-9

- 6,200 TYU 133 puts, 12-13

- 5,600 TYU 133.5 puts, 19

- >10,000 wk2 TY 132.5 puts, 3

- 2,000 wk2 TY 132.75/133.5 put spds

EGB-GILTS CASH CLOSE: Lowest close for Bund yields since 2 February

Bunds and gilts have outperformed Treasuries today despite some decent data this morning.

- German GDP disappointed but there were some positive surprises elsewhere, both in the pan-Eurozone data and in Italian, Spanish and (to a lesser extent) French data.

- Eurozone inflation data also came in higher than expected with the headline rate rising to 2.2%Y/Y (2.0% expected) although core was in line with expectations at 0.7% Y/Y.

- Despite this better than expected data, peripheral spreads are generally a little wider on the day, with 10-year BTP-Bund spreads widening 0.7bp to 108.0bp.

- The moves higher for Bunds have seen yields close at their lowest level since February 2.

- Gilt yields in contrast have managed to close above the 200-dma which has now been breached many times over the past 2 weeks on an intraday basis.

- Bund futures are up 0.13 today at 176.57 with 10y Bund yields down -1.1bp at -0.462% and Schatz yields down -0.5bp at -0.767%.

- Gilt futures are up 0.04 today at 129.79 with 10y yields down -0.8bp at 0.564% and 2y yields down -1.4bp at 0.054%.

- BTP futures are down -0.07 today at 154.28 with 10y yields down -0.4bp at 0.620% and 2y yields unch at -0.453%.

FOREX: Greenback Stages Partial Recovery Ahead Of Month-End

- After retreating for four consecutive trading days the US dollar bucked the short-term trend and regained some poise on Friday.

- The dollar index firmed 0.3% ahead of the month-end WMR fix, with reported signals from sell-side institutions mixed ahead of the event. Despite the minor recovery, the index is set to post a 1% weekly drop.

- With stocks rolling off their highs, AUDUSD and NZDUSD came under pressure, the former losing roughly 0.65%.

- EURUSD breached the 1.19 handle but stopped just shy of touted short-term key resistance at the 50-day EMA at 1.1916. Broad dollar strength brought he single currency back to lows of 1.1852, traded just before 4pm London.

- The most notable turnaround in G10 was the Norwegian Krona where EURNOK reversed the majority of the last two days losses to post a positive week. USDNOK rose 1.15%.

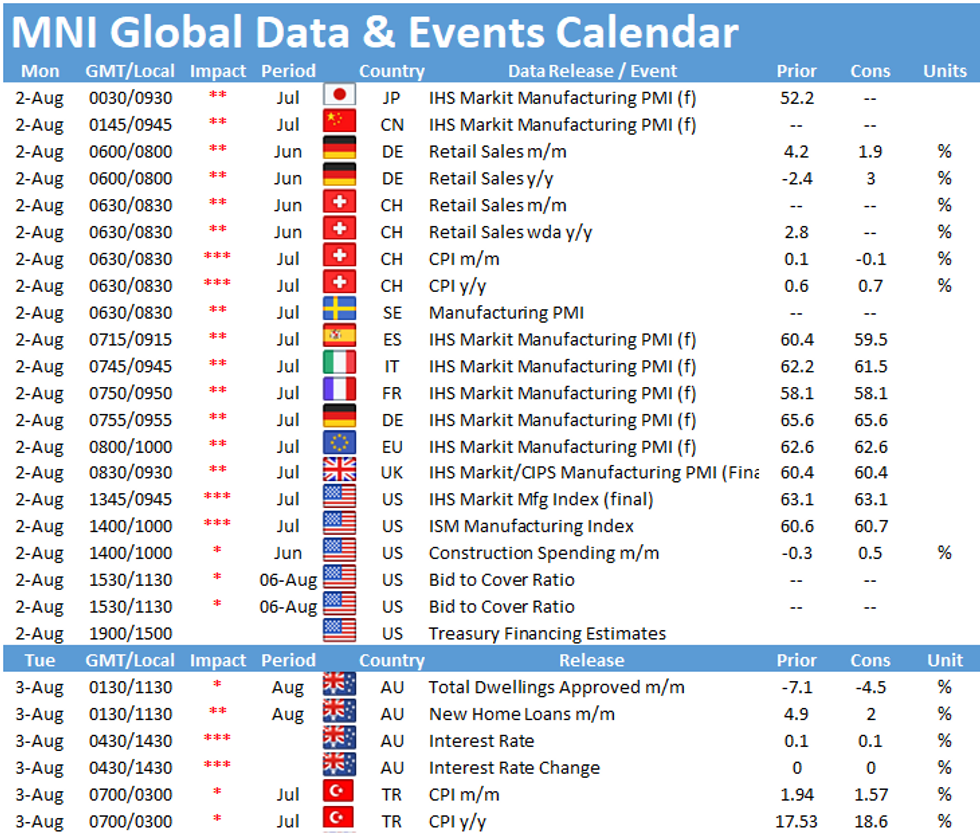

- Final European Manufacturing PMI readings on Monday before US ISM Manufacturing PMI headlines the docket. Canada will be out for Civic Holiday.

- The main focus for markets next week will be Friday's release of US Non-Farm Payrolls. Other notable events include the RBA and BOE meetings as well as NZ and CAD unemployment.

FX/Expiries for Aug02 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1800-15(E1.1bln), $1.1900(E1.3bln), $1.2000-20(E901mln)

- AUD/USD: $0.7360(A$524mln), $0.7400(A$1.1bln)

- USD/CAD: C$1.2550($514mln)

- USD/CNY: Cny6.50($650mln), Cny6.5300($1bln)

PIPELINE: Apple's $6.5B 4Pt Helped Push Issuance for Wk Over $28B

- Date $MM Issuer (Priced *, Launch #)

- 07/30 $750M United Rentals 10.5NC5

- $15.1B to price Thursday; $28.9B/wk

- 07/29 $6.5B *Apple 4pt jumbo: $2.3B 7Y +40, $1B 10Y +47, $1.8B 30Y +77, $1.4B 40Y +92 (adds to $8.5B issued back on May 4, 2020: $2B 3Y +60, $2.25B 5Y +80, $1.75B 10Y +110, $2.5B 30Y +145)

- 07/29 $3B *Humana $1.5B 2NC.5 +50, $750M 5Y +65, $750M 10Y +90

- 07/29 $2.5B *Synnex $700M 3NC1 +90, $700M 5Y +110, $600M 7Y +135, $500M 10Y +145

- 07/29 $2B *Blackstone $650M 7Y +65, $850M 10.5Y +85a, 30Y +95a

- 07/29 $500M *New York Life 10Y +58

- 07/29 $600M *DR Horton Inc 5Y +60

EQUITIES: Stocks Roll Off Highs as Amazon Knock Chunk Off Indices

- Wall Street traded softer Friday, with all three major indices headed into the close in the red as notable underperformance in Amazon weighed on sentiment. Following their disappointing earnings release, Amazon slipped over 7%, wiping well over $100bln off the company's market cap. Amazon reported a miss on quarterly sales for the first time in over three years.

- US-China sentiment worsened, with markets watching a decision from the US SEC to freeze all IPO registrations for companies based in China. The regulator has given no timeline for when registrations could resume, with guidance being drawn up to warn investors of the risks associated with companies sensitive to Chinese politics.

- Amazon's miss put the consumer discretionary sector at the bottom of the pile in the S&P, with energy names not far behind. Real estate and consumer staples were the best performing sectors.

COMMODITIES: WTI Prices Flat on Friday, But Curve Remains Steeper on the Week

- WTI and Brent crude futures finished flat on the session Friday, with few macro catalysts to nudge markets in either direction. Nonetheless, the curve remains steeper on the week, with markets looking through near-term volatility in China as US equities continue to march higher.

- The mid-week DoE inventories remain a supportive factor, suggesting solid implied demand that's carried prices into the Friday close. This keeps the near-term rebound intact, with prices breaching the 76.4% retracement of the Jul 6 - 20 downleg at $73.46. This signals scope for a climb towards key resistance at $76.07/bbl.

- Both gold and silver traded lower into the close, with MNI Chicago Business Barometer adding some weight, beating expectations to rise to 73.4 vs. Exp. 64.2.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok