Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

US TSY SUMMARY: Afghan Pullout Deadline Set for Aug 31

Tsys trading weaker after the bell, aside from a large 10k FVU block sale at 123-31.5, rates were under pressure all session with a cautious risk-on tone as equities made new all time highs (ESU1 4491.75).- Little direction from mixed data: Richmond Fed's August reading of 9 was well below expectations (24) and a sharp drop from July's reading (27). New home sales were better than expected: +1% TO 0.708M SAAR.

- Take away the heavy Sep/Dec roll volume and trade was rather muted -- typical for late summer trade. Tsy 10YY climbed to 1.2902% high in late trade, 30YY 1.9079% high. Underlying risk factors remain mixed: deadline for US/Allied pull-out from Afghanistan appears to be Aug 31 as hopes for an extension dashed by Taliban officials. Closer to home: HOUSE DEMOCRATS AGREE ON PATH TO ADVANCE BUDGET, INFRASTRUCTURE, Bbg

- Meanwhile, the 2Y note sale saw second consecutive stop -- Tsy futures bounced off lows following strong $60B 2Y (91282CCU3) note draws 0.242% vs. 0.252% WI. Bid-to-cover was 2.65x well over 5 month average of 2.53x. Indirect take-up climbs to 60.54% from 52.76% in July (50.94% 5M avg); direct bidder take-up of 21.18% continues to outpace 5M avg of 18.77%; primary dealer take-up falls to 18.28% vs. 5-month average of 30.29%.

- The 2-Yr yield is up 0bps at 0.2243%, 5-Yr is up 2.3bps at 0.7917%, 10-Yr is up 3.5bps at 1.2868%, and 30-Yr is up 3.4bps at 1.9046%.

SHORT TERM RATES

US DOLLAR LIBOR: Latest Settles

- O/N -0.00012 at 0.07763% (+0.00025/wk)

- 1 Month +0.00450 to 0.08888% (+0.00300/wk)

- 3 Month -0.00750 to 0.12175% (-0.00662/wk) ** (Record Low: 0.11800% on 6/14)

- 6 Month +0.00500 to 0.15800% (+0.00537/wk)

- 1 Year -0.00012 to 0.23688% (+0.00025/wk)

- Daily Effective Fed Funds Rate: 0.09% volume: $67B

- Daily Overnight Bank Funding Rate: 0.08% volume: $261B

- Secured Overnight Financing Rate (SOFR): 0.05%, $899B

- Broad General Collateral Rate (BGCR): 0.05%, $373B

- Tri-Party General Collateral Rate (TGCR): 0.05%, $356B

- (rate, volume levels reflect prior session)

- TIPS 1Y-7.5Y, $2.001B accepted vs. $3.791B submission

- Next scheduled purchases

- Wed 8/25 1010-1030ET: Tsy 10Y-22.5Y, appr $1.425B

- Thu 8/26 1010-1030ET: Tsy 0Y-2.25Y, appr $12.425B

- Fri 8/27 1010-1030ET: Tsy 22.5Y-30Y, appr $2.025B

FED: REVERSE REPO OPERATION

NY Fed reverse repo usage slips to 1,129.737B from 77 counter-parties vs. Monday's record $1,135.697B. Prior record high of $1,115.656B set Wednesday, Aug 18.

EURODOLLAR/TREASURY OPTIONS SUMMARY

Eurodollar Options:- +5,000 Dec 99.75/99.87 call spds, 6.25

- +10,000 Mar 100 calls, 1.0 vs. 99.84/0.05%

- +15,000 short Nov 99.37 puts, 2.5 vs. 99.545/0.20%

- +2,000 short Dec 99.50 puts, 6.5 vs. 99.545/0.41%

- -5,000 short Oct 99.37/99.50 2x1 put spds, 1.0

- Overnight trade

- 12,000 short Sep 99.56 puts, appr 4k vs. 99.68 puts on 2x1 spd

- 8,100 Blue Sep 98.00 puts

- 4,700 Blue Dec 98.25/98.50 put spds

- +7,000 TYZ 131.5/136.5 strangles, 45

- +25,000 wk1 TY 133.5/134.5 call spds, 22

- +2,000 TYU 133.25/133.75 2x1 put spds, 2 vs. 134-07/0.06%

- Overnight trade

- 7,600 TYZ 130 puts, 15

- 2,200 TYU 134 puts, 14

EGBs-GILTS CASH CLOSE: Decent Supply, But Little Direction

European FI failed to find decisive direction Tuesday. Yields rose sharply at the London open, then fell to session lows mid-morning before drifting higher again - finishing largely unchanged.

- Periphery spreads clawed back some ground vs Monday's widening.

- In supply, the GBP3bln 5Y auction was weak (earlier, DMO consultation minutes for 3Q issuance were largely in line with MNI's expectations) Finland sold E3bln 5Y RFGB via syndication, and Germany auctioned 4bln 7Y Bund.

- We also saw a lot of downside buying in Bunds via options.

- In data: German 2Q GDP was revised a little higher, but no market impact.

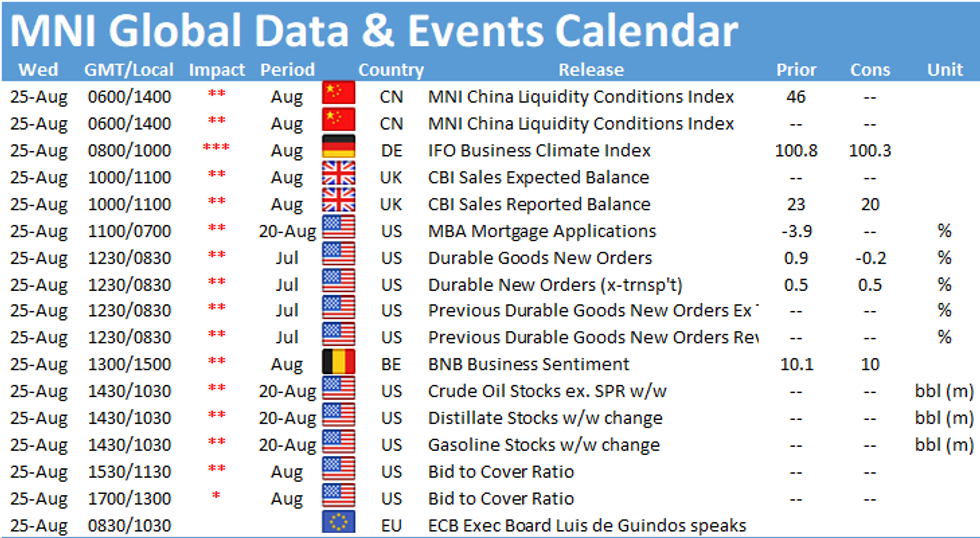

- Wednesday's calendar includes German IFO data and an appearance by ECB's de Guindos.

Closing Yields / 10-Yr Periphery EGB Spreads To Germany

- Germany: 2-Yr yield is up 0.3bps at -0.744%, 5-Yr is up 0.5bps at -0.737%, 10-Yr is up 0.3bps at -0.478%, and 30-Yr is up 0.3bps at -0.028%.

- UK: 2-Yr yield is up 1bps at 0.125%, 5-Yr is up 1bps at 0.27%, 10-Yr is up 0.3bps at 0.538%, and 30-Yr is up 0.2bps at 0.947%.

- Italian BTP spread down 1.4bps at 104.8bps / Spanish up 0.1bps at 71.3bps

EGB OPTIONS: Almost All Bund Downside Plays Tuesday

Tuesday's European rates/bonds options flow included:

- RXZ1 173.5/172.5ps vs 175/176cs, bought the ps for flat in 1k

- RXU1 176.00 put bought for 7 in 2k

- RXV1 173.00/172.00 1x2 put spread bought for 1 in 1.75k (3.5k all day)

- RXX1 170.00/168.50 put spread bought for 9 in 1.5k

- RXZ1 170.5p, bought for 39 in 1.5k

- 3RZ1 100.25/100ps 1x2, bought for 2 in 2.5k

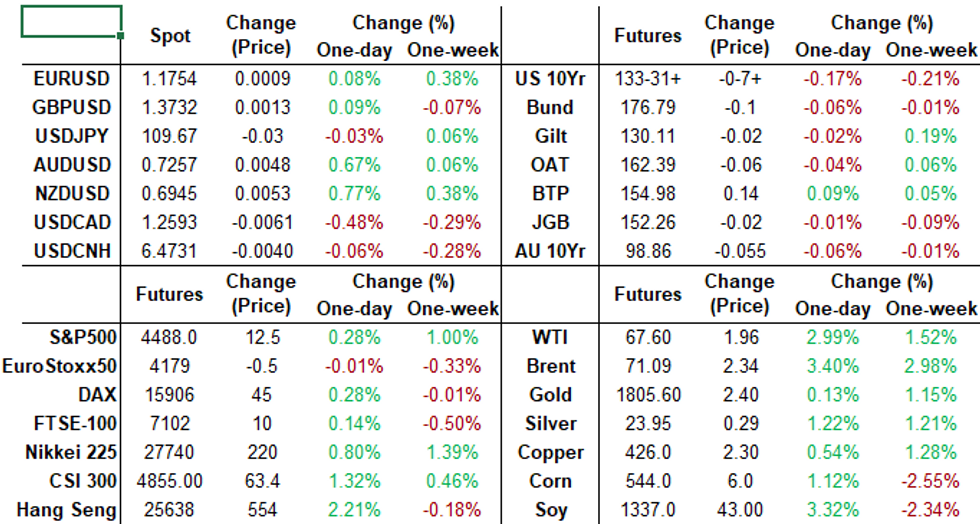

FOREX: Commodity-Tied FX Extends Gains, Greenback Consolidates

- The Norwegian Krone was top of the pile for a second day as oil extended its recovery into a second day and negated the entirety of last weeks drawdown. NOK firmed just under 1% on Tuesday.

- Antipodean FX was close behind, consolidating gains made during APAC trade and enjoying the relief rally in risk assets.

- EUR, JPY, GBP and CNH were broadly unchanged, trading in narrow ranges ahead of Jackson Hole later this week. As such EUR crosses suffered with EURNZD printing briefly below .169 after topping out at 1.7166 on Monday.

- The dollar index briefly extended its decline in the lead up to the WMR fix. However, with limited catalysts to prompt any momentum selling, a steady bounce to unchanged ceased the action for the day but indices held on to the week's declines.

- USDCAD (-0.45%) confirmed a short-term reversal pattern by extending past the 20-day EMA and now may target 1.2509, the 50-day EMA, with the additional 3% rally in crude a clear CAD tailwind.

- Emerging market currencies saw slightly more action with notable moves in high beta plays such as BRL and ZAR, with the latter slipping back below the 15.00 handle having traded at 15.40 on Friday.

- NZ Trade Balance overnight will be followed by German IFO data out of Europe. US Durable Goods Orders and Crude Oil Inventories will round of Wednesday's calendar.

PIPELINE: $3B EIB Priced, Nordea Launched

- Date $MM Issuer (Priced *, Launch #)

- 08/24 $3B *EIB WNG +5Y -1

- 08/24 $1B MUNIFIN WNG 5Y +4a

- 08/24 $1B #Nordea Bank perp 9/29 3.75%

- 08/24 $Benchmark Schwab 10Y +95a

- 08/24 $Benchmark ABC Int Holdings 3Y +70a, 5Y +85a

MARKET SNAPSHOT

Key late session market levels

- DJIA up 88.21 points (0.25%) at 35423.9

- S&P E-Mini Future up 12.75 points (0.28%) at 4488.25

- Nasdaq up 86.5 points (0.6%) at 15029.19

- US 10-Yr yield is up 3.5 bps at 1.2868%

- US Sep 10Y are down 7/32 at 134-0

- EURUSD up 0.001 (0.09%) at 1.1756

- USDJPY down 0.02 (-0.02%) at 109.68

- WTI Crude Oil (front-month) up $2.06 (3.14%) at $67.69

- Gold is up $0.53 (0.03%) at $1805.97

- EuroStoxx 50 up 1.66 points (0.04%) at 4178.08

- FTSE 100 up 16.76 points (0.24%) at 7125.78

- German DAX up 53.06 points (0.33%) at 15905.85

- French CAC 40 down 18.79 points (-0.28%) at 6664.31

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok