Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

US TSYS: Fed Chair Powell Has Last Word On Likely Nov Taper Annc Ahead Blackout

Back to the flattener. Tsys traded mildly weaker early Friday, gradually rebounding ahead mixed Markit PMIs: Mfg softer (59.2 vs. 60.5est and 60.7 in Sep) while Services picked up (58.2 vs. 55.2 est and 54.9 in Sep).- Tsy futures that had pared gains/traded weaker in 2s-10s after Fed chair started speaking at a SARB event, staying on script despite a surge in market rate hike pricing.

- Powell said Fed is "on track" to begin and complete the taper by mid-'22; inflation pressures as transitory, though likely to last longer than had previously been expected, with supply constraints lasting well into next year. Equities pared gains after chairman Powell said inflation "well above target."

- Focus on Powell quickly ebbed as Tsys surged on back of EU Brexit headlines -- unattributed and unconfirmed on wires and social media stating the EU will consider terminating the Brexit trade agreement (TCA) with the UK if the rift between Brussels and Westminster deepens. Tsy futures surged to session highs but have scaled back support slightly as well, Yield curve broadly flatter in near end, while 5s30s are off 18 month low tapped Monday:

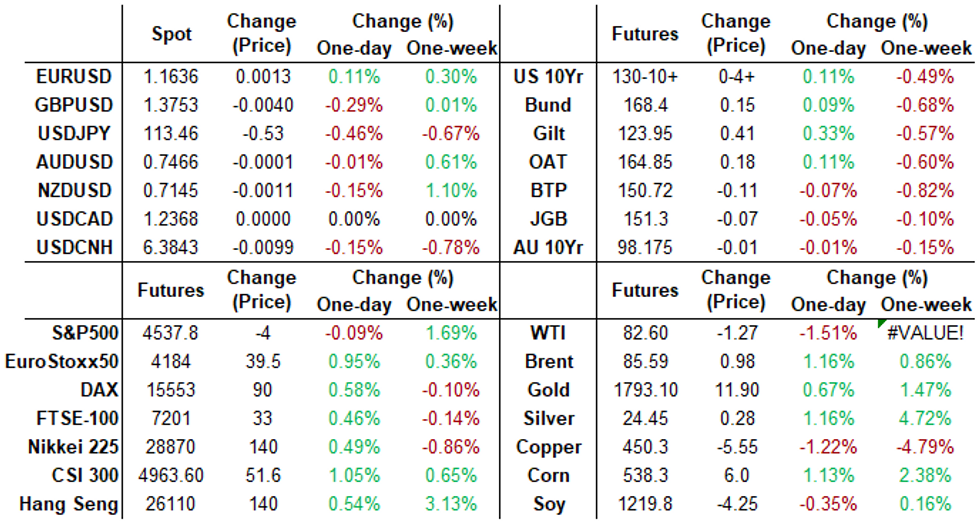

- The 2-Yr yield is up 0.7bps at 0.4615%, 5-Yr is down 3.3bps at 1.2072%, 10-Yr is down 4.9bps at 1.6518%, and 30-Yr is down 5.9bps at 2.0883%.

SHORT TERM RATES

US DOLLAR LIBOR: Latest settlements

- O/N +0.00075 at 0.07350% (+0.00038/wk)

- 1 Month -0.00137 to 0.08788% (+0.00750/wk)

- 3 Month +0.00100 to 0.12488% (+0.00125/wk) ** Record Low 0.11413% on 9/12/21

- 6 Month +0.00175 to 0.17200% (+0.01150/wk)

- 1 Year +0.02038 to 0.31688% (+0.03725/wk)

- Daily Effective Fed Funds Rate: 0.08% volume: $75B

- Daily Overnight Bank Funding Rate: 0.07% volume: $284B

- Secured Overnight Financing Rate (SOFR): 0.03%, $879B

- Broad General Collateral Rate (BGCR): 0.05%, $360B

- Tri-Party General Collateral Rate (TGCR): 0.05%, $332B

- (rate, volume levels reflect prior session)

- Tsys 4.5Y-7Y, $6.001B accepted vs. $20.799B submission

- Next scheduled purchases

- Mon 10/25 1010-1030ET: Tsy 22.5Y-30Y, appr $2.025B

- Tue 10/26 1010-1030ET: TIPS 7.5Y-30Y, appr $1.225B

- Wed 10/27 1010-1030ET: Tsy 10Y-22.5Y, appr $1.425B

- Thu 10/28 1010-1030ET: Tsy 0Y-2.25Y, appr $12.425B

- Fri 10/29 1010-1030ET: Tsy 10Y-22.5Y, appr $1.425B

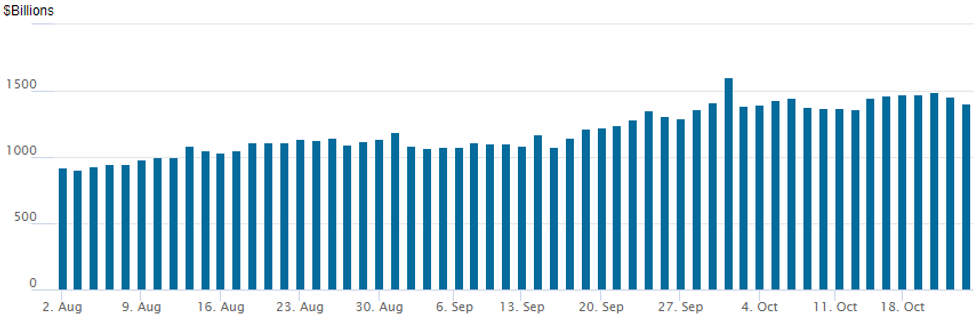

FED Reverse Repo Operation

NY Federal Reserve/MNI

NY Fed reverse repo usage recedes to $1,403.020B from 79 counterparties from $1,458.605B on Thursday. Record high remains at $1,604.881B from Thursday, September 30.

EURODOLLAR/TREASURY OPTIONS SUMMARY

Eurodollar Options:- 1,500 Apr/Jun 99.87/100 2x3 call spd strip

- Block, 16,000 short Dec 98.75/99.00/99.25 put flys, 5.5 at 1229:14ET

- 20,000 short Dec 98.93/99.00 put spds

- -10,000 short Dec 99.00 puts, 5.0

- BLOCK, +20,000 short Nov 99.50 calls, 0.5

- -50,000 Blue Jun 96.25/96.75/97.00/97.50 put condors, 4.5 -- Loss

- +50,000 Blue Jun 96.25/96.75/97.00/97.50 put condors, 5.0 -- error followed by sale

- -5,000 Jun 99.50/99.75 put spd w/ 99.37/99.62 put spd strip, 14.5

- Overnight trade

- 6,000 Green Dec 98.50/98.62/98.75 call trees

- +9,000 Jun 99.25/99.50 2x1 put spds, 0.0

- +4,000 Green Dec 98.00/98.25 put spds, 4.0

- 4,400 Green Mar 98.25 puts, 18.5

- +Block, 5,000 short Dec 98.62/98.87/99.12 put flys, 3.5 vs. 99.215/0.14%

- Block, 9,250 wk1 FV 120.75/121.25 put spds, 7 vs. 121-21.5/0.15%

- +50,000 FVZ 120.5 puts, 10.5, 121-18.5 ref, total volume 59,505

- 5,500 FVZ 121.75/122.25/122.75 put trees

- Overnight trade

- -10,000 TYZ 130/132 put spds 32

- 20,000 TYX 130 puts mostly around 5-6

- +11,000 TYZ 128/128.5 put spds, 5

- 3,500 TYZ 127.5 puts, 8

- 3,600 TYX 130/131.5 put spd vs. TYF 126/127.5 put spd

- 4,500 FVX 121.75/122 call spds

EGBs-GILTS CASH CLOSE: Last-Minute Brexit Surprise Cements Gilt Gains

Gilts closed the week on a strong note, with the long end rallying on a Bloomberg article out just minutes before the cash close: "EU Considers Terminating Brexit Trade Deal If UK Rift Deepens".

- The move cemented Gilt outperformance of Bunds and Treasuries on the day, but perhaps notably, the short-end didn't react much (perhaps the news is not seen impacting near-term BoE hike odds).

- Both the German and UK curves flattened Friday. Periphery spreads widened slightly.

- Data was mixed: UK retail sales disappointed in September, though UK PMI impressed while Eurozone numbers were generally on the weak side of expectations.

- After hours ratings reviews include Greece, Italy, and the UK.

Closing Yields / 10-Yr Periphery EGB Spreads To Germany

- Germany: The 2-Yr yield is up 0.9bps at -0.637%, 5-Yr is up 0.9bps at -0.423%, 10-Yr is down 0.3bps at -0.105%, and 30-Yr is down 3.3bps at 0.239%.

- UK: The 2-Yr yield is down 4.8bps at 0.661%, 5-Yr is down 3.4bps at 0.829%, 10-Yr is down 5.7bps at 1.145%, and 30-Yr is down 8.1bps at 1.361%.

- Italian BTP spread up 1.1bps at 110.4bps / Spanish up 0.7bps at 63.3bps

EGB Options: Mostly Fading Rate Downside

Friday's Europe rates / bonds options flow included:

- ERU3 100.00/99.875 put spread sold at 3 in 10k

- 0RH2 100.50 calls bought for 0.75 in 3k

- 2RZ1 100.25/100.50 call spread bought for 1.5 in 2k (vs 100.02 10d)

- 2RM2 100.25/100.375/100.625 broken call fly bought for 1 in 5.5k

- 3RZ1 99.875^ bought for 21.5 in 3.25k

- SFIH2 99.35/99.55/99.60 call ladder bought for 3.25 in 4k

FOREX: USDJPY Falls For Third Consecutive Session, GBP Reverts Lower

- Fed Chair Powell's stance doesn't seem to have changed significantly in recent weeks despite a surge in market rate hike pricing. While his comments initially lent support to the greenback, this price action quickly reversed and USDJPY made fresh weekly lows.

- USDJPY has now fallen for three days, edging back towards 113.50, consolidating on the sharp rally from 109 in late September. Dips are still considered technically corrective with initial firm support seen at 112.08, Sep 30 high and a recent breakout level.

- GBP was the worst G10 performer on Friday and the weakness was exacerbated as headlines dropped suggesting the EU could weigh terminating the post-Brexit trade deal if the U.K. government pulls out of its commitments over Northern Ireland.

- An already weak GBPUSD, shot to fresh lows of 1.3836 before stabilising into the close. Interestingly, for the sixth day in a row, EURGBP has made lows between 0.8422-24 before finding support. While the price action has remained broadly GBP supportive, today's rally marks the most meaningful bounce in the cross, rising back above the August lows to a high of 0.8468.

- In emerging markets, USDTRY continued its ascent, rising close to 1% and breaching 9.60 and printing fresh all-time highs of 9.6625. RUB bucked the trend following the surprise 75bp hike from the CBR prompting an extension of USDRUB weakness. After briefly breaching the 70.00 mark, the pair approaches the close down close to 1% at 70.35.

- A busy central bank schedule for next week, with monetary policy decisions from the Bank of Canada, the Band of Japan and the European central Bank.

- German IFO on Monday and AUD CPI Tuesday are early data points of note.

FX: Expiries for Oct25 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1600-15(E689mln), $1.1720-25(E638mln), $1.1883-00($1.2bln)

- USD/JPY: Y113.00($586mln), Y114.25-50($1.2bln)

- USD/CAD: C$1.2500($620mln)

- USD/CNY: Cny6.4000($631mln)

PIPELINE: $21B AerCap Pushed Total Oct Issuance To $120.7B

$24.5B Priced Thursday, puts total for week at $63.25B, $120.7B/month

- Date $MM Issuer (Priced *, Launch #)

- 10/21 $21B *AerCap 9-tranche jumbo: $1.75B 2Y +70, $500M 2Y FRN/SOFR+68, $3.25B 3Y +90, $1B 3NC1 +100, $3.75B 5Y +125, $3.75B 7Y +150, $4B 10Y +165, $1.5B 12Y +175, $1.5B 20Y +175

- 10/21 $3B *CADES (Caisse d'Amortissement de la Dette Sociale) 5Y LIBOR+5

- 10/21 $500M *Santander Chile 10Y +150

EQUITIES

- DJIA up 95.73 points (0.27%) at 35699.43

- S&P E-Mini Future down 4.5 points (-0.1%) at 4537.25

- Nasdaq down 119.7 points (-0.8%) at 15096.11

COMMODITIES: Powell Pinches Late Gold Rally

- Oil markets traded slightly firmer Friday, but were generally rangebound, with WTI crude futures failing to mount any material test on the cycle highs printed earlier in the week at $83.96/bbl.

- This keeps the trend condition bullish and this week's fresh trend high maintains the bullish price sequence of higher highs and higher lows, reinforcing the uptrend. The focus is on $85.01 next, a Fibonacci projection.

- Gold traded well into the Friday close, with prices gaining on the break of $1,800 as well as the mid-September highs of $1808.7. The break of the latter narrows the gap with the next bull trigger at the Jul 15 high of $1834.1.

- Precious metals gained well, but faltered slightly later in the session as Fed's Powell confirmed that the Fed is on track to begin a taper, and is set to complete by mid-2022. This comment underpinned a minor recovery in the dollar, preventing the USD Index from any material test on the week's lows of 93.496.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok