Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

US TSYS: Tsy Ylds Resume Climb Ahead Midweek FOMC Annc

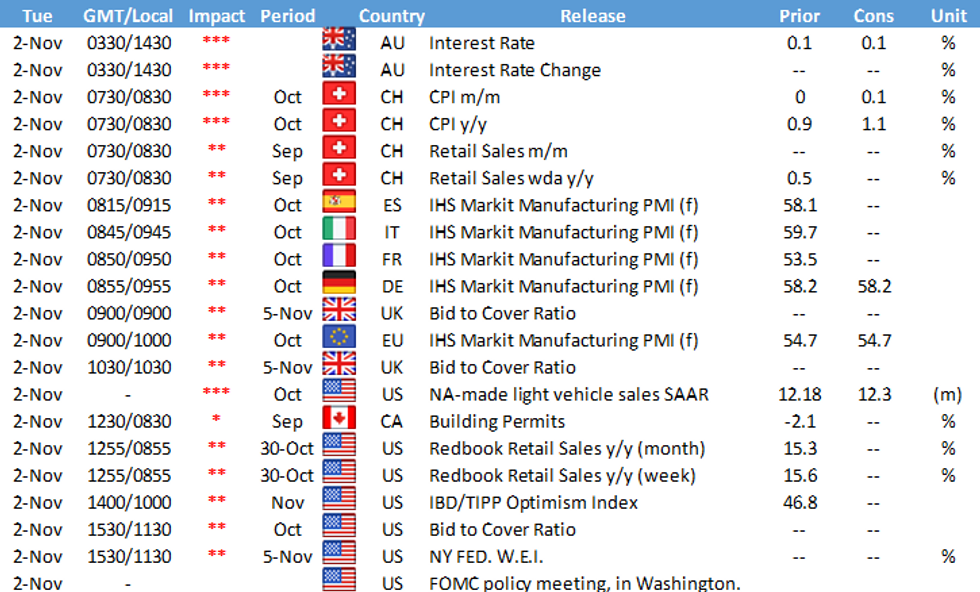

Tsys yields gained as November got underway, levels back near middle of Friday's range, yield curves steeper on moderate volumes.- Sights set on Wed's FOMC policy annc where $15B/month taper is expected with particular attention on inflation dynamics. Last but not least: Friday's October employment data: +450k median estimate up from +400k job gains last Friday.

- Session flow largely two-way position squaring ahead the Fed and jobs data risk events. Nevertheless, Tsy futures held weaker levels/off lows by the close, equities higher/off new all-time highs from the first half (ESZ1 4619.5). US$ pared some of Fri's strong gains (DXY -.235 at 93.888).

- Data remains muted Tuesday but picks up early Wednesday with ADP private employ figures at 0815ET (+400k est vs. +568k prior), and Tsy quarterly refunding at 0830ET.

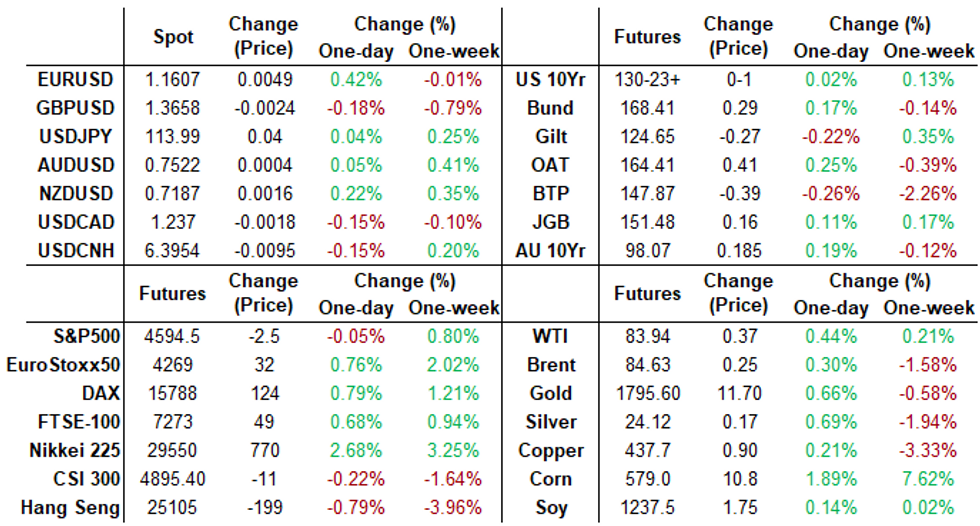

- The 2-Yr yield is up 1bps at 0.5071%, 5-Yr is up 0.7bps at 1.1896%, 10-Yr is up 1.6bps at 1.568%, and 30-Yr is up 3bps at 1.9631%.

SHORT TERM RATES

US DOLLAR LIBOR: Latest settlements

- O/N -0.00450 at 0.06763% (-0.00138 total last wk)

- 1 Month -0.00637 to 0.08113% (-0.00038 total last wk)

- 3 Month +0.00863 to 0.14088% (+0.00738 total last wk) ** Record Low 0.11413% on 9/12/21

- 6 Month +0.00988 to 0.21088% (+0.02900 total last wk)

- 1 Year +0.00612 to 0.36725% (+0.04425 total last wk)

- Daily Effective Fed Funds Rate: 0.07% volume: $70B

- Daily Overnight Bank Funding Rate: 0.06% volume: $222B

- Secured Overnight Financing Rate (SOFR): 0.05%, $847B

- Broad General Collateral Rate (BGCR): 0.05%, $336B

- Tri-Party General Collateral Rate (TGCR): 0.05%, $317B

- (rate, volume levels reflect prior session)

- Tsy 22.5Y-30Y, $1.999B accepted vs. $4.601B submission

- Next scheduled purchases

- Tue 11/02 1010-1030ET: TIPS 1Y-7.5Y, appr $2.025B

- Wed 11/03 No buy operation due to FOMC annc

- Thu 11/04 1010-1030ET: Tsy 4.5Y-7Y, appr $6.025B

- Thu 11/04 1100-1120ET: Tsy 10Y-22.5Y, appr $1.425B

- Fri 11/05 1010-1030ET: Tsy 2.25Y-4.5Y, appr $8.425B

FED Reverse Repo Operation

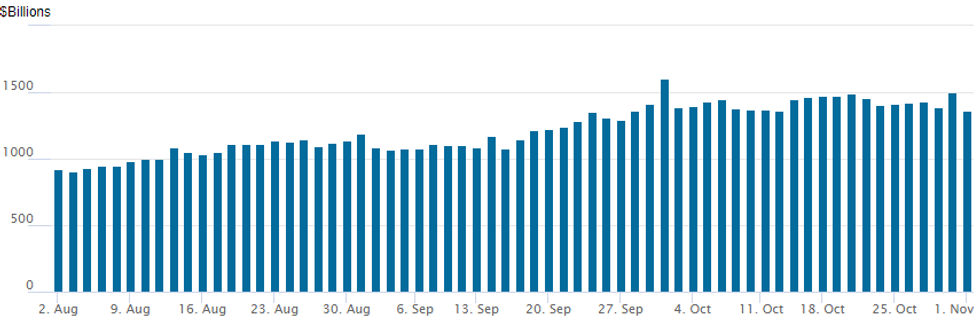

NY Fed reverse repo usage declines as November gets underway: at $1,358.606B from 74 counterparties vs. Friday's second highest usage on record of $1,502.296B. Record high remains at $1,604.881B from Thursday, September 30.

EURODOLLAR/TREASURY OPTIONS SUMMARY

Eurodollar Options:- -3,000 short Dec 99.25/99.37/99.50 put flys, 2

- 2,500 Jun 98.62/99.25 put spds

- 5,000 Sep 97.00/97.75 put spds

- Block, 15,000 Red Dec 99.00/99.25 put spds, 9.5

- 6,900 short Jan 98.00 puts, 2.5

- Overnight trade

- Block, 7,500 short Dec 98.75/98.87/99.00 put flys, 1.5 vs. 99.08/0.05%

- 37,800 short Mar 97.87 puts, 3.5

- 3,000 Red Dec 100.12 calls, 1.0

- 2,250 Blue Dec 97.50/97.87 3x2 put spds

- 2,500 Blue Dec 98.25/98.50 call spds

- 5,000 TYZ 129/130 put spds, 16

- Overnight trade

- 10,000 wk1 TY 129 puts

- 5,500 TYZ 129

FOREX: Swiss Franc and Swedish Krona Shine As Greenback Fades

- The greenback started the week on the backfoot after Friday's strong near 1% rally. The dollar index (-0.26%) slipped back below the 94.00 mark with EURUSD also regaining the 1.16 handle.

- Of note throughout the session were strong performances for both the Swiss Franc and the Swedish krona.

- EURCHF (-0.27%) and USDCHF (-0.70%) have continued recent trajectories lower, with both pairs approaching support areas worth noting. For EURCHF, 1.0505/10 represents an area of multiple lows between April-May 2020.

- On a slightly shorter-term note, USDCHF right around 0.9100 horizontal support across the mid-August lows. Additionally, an upward sloping trendline across the 2021 lows intersects near 0.9085. A break of this technical point could have the potential to accelerate CHF strength and would target the August and June lows at 0.9019 and 0.8926 respectively.

- USDSEK finds itself 0.81% lower on the session as EURSEK accelerates recent weakness below the 10.00 handle. Following the breach of the 2021 lows and a period of consolidation, EURSEK now trades below 9.90 and the lowest levels since February 2018.

- Elsewhere, EURGBP (+0.58%) enjoyed a relief rally, completing a full point bounce from the 0.84 lows made last week.

- In emerging markets, MXN and ZAR extended recent weakness and were particular underperformers both falling roughly 1.2% versus the dollar.

- Markets will focus on the RBA decision due overnight ahead of Swiss data to kickstart the European session.

PIPELINE: $11.45B To Price Monday

- Date $MM Issuer (Priced *, Launch #)

- 11/01 $3B #JP Morgan 11NC10 fix/FRN +97

- 11/01 $3B #American Express $800M 2Y +25, $600M 2Y FRN/SOFR+23, $1.1B 5Y +50, $500M 5Y FRN/SOFR+65

- 11/01 $2.1B #Raytheon Tech $1B +10Y +80, $1.1B +30Y +105

- 11/01 $1B #Invitation Homes $600M 7Y +87, $400M 12Y +115

- 11/01 $700M #Republic Services 11Y +83 (upsized from $600M)

- 11/01 $650M #Southwestern Electric Power 30Y +130

- 11/01 $500M #Duke Realty +10Y +82

- 11/01 $500M Jane Street Group 8NC3

EQUITIES

- DJIA up 73.4 points (0.2%) at 35889.29

- S&P E-Mini Future up 0.25 points (0.01%) at 4596.5

- Nasdaq up 32.9 points (0.2%) at 15529.23

COMMODITIES

- WTI Crude Oil (front-month) up $0.42 (0.5%) at $83.99

- Gold is up $9.75 (0.55%) at $1793.23

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok