Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

US TSYS: Solid October Jobs Gains/Up Revisions, Tsys Rally Anyway

Not exactly the result one would expect after solid job gains and up-revisions to prior reads: Treasury futures marched higher all day after initially trading modestly weaker on Oct NFP: +531k job gains vs. +450k est, Sep up-revision to +312k and unemployment rate drop to 4.6% vs. 4.7% est.- Tsys drew some sporadic buying/short covering after initial surge in selling across the curve. Futures marched higher with 30YY tapping 1.8708% low -- last seen Sep 23. Yield curves bull flattened for a period before bull flattening as the session progressed, 5s30s tapped 80.566L before bouncing to 82.671 after the bell.

- Fading the rally, sources report real$ acct selling in 10s, 20s and 30s late morning, rate receivers/payer unwinds in 2s-10s. Trading desks also partially tied rally to re-positioning in aftermath of Thu's FOMC (accelerated taper schedule) and Boe (hawkish hold) while gilts continued to outperform.

- Equities made new all-time highs (ESZ1 4711.75) while oil surged (WTI +2.75 to 81.56), Bbg story reports: "Saudi Aramco Raises Oil Prices Sharply After OPEC+ Defies Biden" call to increase output.

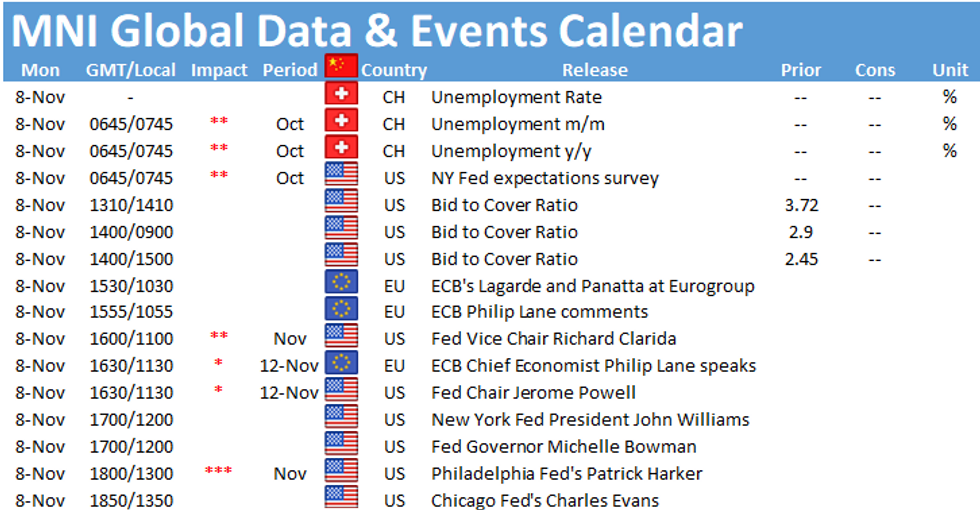

- Data look ahead: PPI and CPI on next week's shortened Veterans Day holiday (Nov 11), Treasury coupon supply (3s, 10s and 30s on reduced size) and Fed speakers coming off the sidelines.

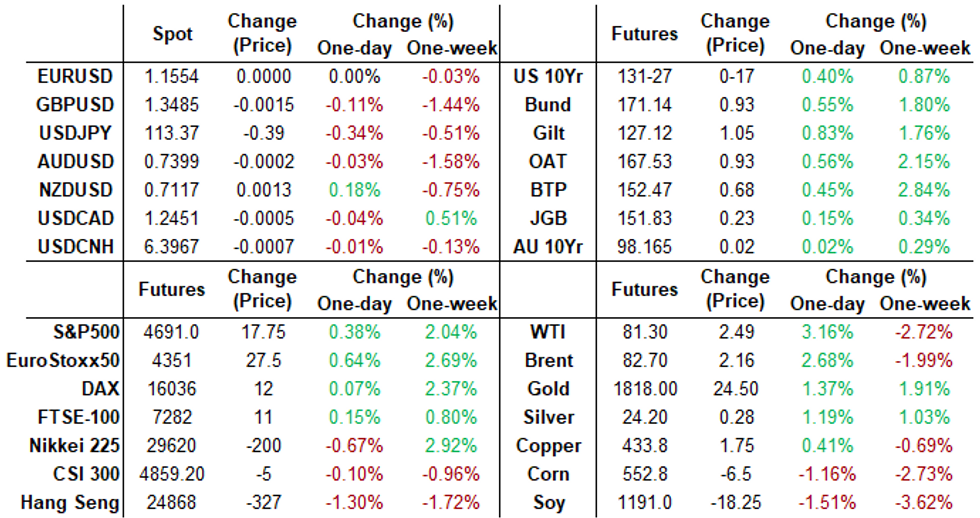

- After the bell, 2-Yr yield is down 2.6bps at 0.3988%, 5-Yr is down 6bps at 1.0507%, 10-Yr is down 7.7bps at 1.4496%, and 30-Yr is down 7.9bps at 1.8837%.

SHORT TERM RATES

US DOLLAR LIBOR: Latest settlements

- O/N +0.00363 at 0.07263% (+0.00050/wk)

- 1 Month -0.00100 to 0.08863% (+0.00213/wk)

- 3 Month -0.00163 to 0.14275% (+0.01050/wk) ** Record Low 0.11413% on 9/12/21

- 6 Month +0.00763 to 0.22088% (+0.01988/wk)

- 1 Year -0.00500 to 0.35750% (-0.00363/wk)

- Daily Effective Fed Funds Rate: 0.08% volume: $76B

- Daily Overnight Bank Funding Rate: 0.07% volume: $276B

- Secured Overnight Financing Rate (SOFR): 0.05%, $925B

- Broad General Collateral Rate (BGCR): 0.05%, $353B

- Tri-Party General Collateral Rate (TGCR): 0.05%, $338B

- (rate, volume levels reflect prior session)

- Tsy 2.25Y-4.5Y, $8.401B accepted vs. $22.622B submission

- Next scheduled purchases

- Mon 11/08 1010-1030ET: Tsy 22.5Y-30Y, appr $2.025B

- Tue 11/09 1010-1030ET: TIPS 7.5Y-30Y, appr $1.225B

- Wed 11/10 1010-1030ET: Tsy 7Y-10Y, appr $3.225B

- Fri 11/12 1500ET: Update NY Fed Operational Purchase Schedule

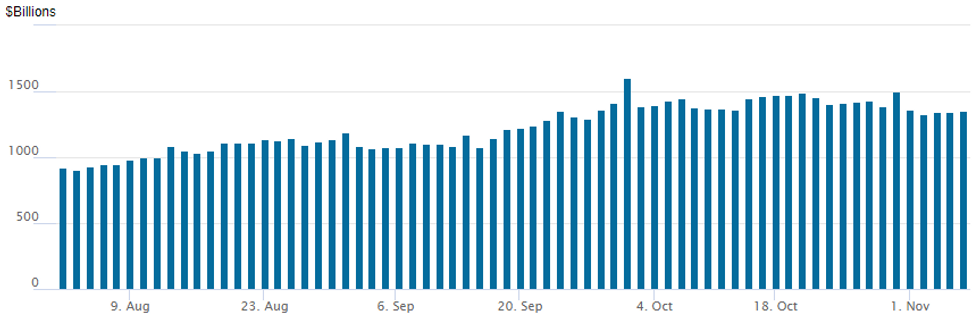

FED Overnight Repo

NY Federal Reserve/MNI

NY Fed reverse repo usage climbs to $1,354.059B from 75 counterparties vs. $1,348.539B on Thursday. Record high remains at $1,604.881B from Thursday, September 30.

EURODOLLAR/TREASURY OPTIONS SUMMARY

Eurodollar Options:- +10,000 Sep 99.12/99.25/99.37/99.50 put condors, 2.0

- Block, +20,000 Red Dec 98.50/98.75 put spds, 3.5 vs. 99.21/0.08%

- -15,000 short Jan 98.62/98.87 put spds, 5

- +9,000 Blue Dec 98.00 puts, 2.5

- 9,200 Dec/Mar 99.87 call spds pre-data

- Overnight trade

- 4,000 Jun 99.43/99.62 put spds

- 2,200 Blue Mar 97.87/98.00/98.12/98.25 put condors

- +13,000 wk2 TY 132.75 calls, 6

- Block, +90,000 wk2 TY 132.75 calls, 4

- +33,000 wk2 TY 133.5 calls, 5

- 7,000 wk2 TY 133 calls, 3

- +12,000 wk2 TY 130.75 puts, 6-7

- 20,000 TYZ 133 calls, 3

- Overnight trade

- 14,000 wk2 TY 131/131.5 call spds

- 5,000 wk2 TY 121.5/121.75 put spds, 3

- 3,700 USZ 165 calls, 12

EGBs-GILTS CASH CLOSE: BoE Fallout Continues

UK yields continued to drop sharply Friday following Thursday's unexpected BoE rate hold, once again dragging down yields across the European FI space.

- Yields continued their drop in the afternoon despite a better-than-expected US jobs report.

- Among other highlights, 30Y yields outperformed and have now erased all the late Sep/Oct rise, while 2-/5Y yields completed their biggest weekly fall since 2009 (2Y -30.2bp, 5Y -27.1bp).

- Though Bund 10Y yields fell sharply (w biggest weekly drop since the pandemic), periphery EGBs kept pace, with spreads flat/only slightly wider.

- Note, Moody's reviews Italy after the close, though stable outlook.

Closing Yields / 10-Yr Periphery EGB Spreads To Germany

- Germany: The 2-Yr yield is down 1.9bps at -0.729%, 5-Yr is down 2bps at -0.579%, 10-Yr is down 5.6bps at -0.28%, and 30-Yr is down 9.2bps at 0.067%.

- UK: The 2-Yr yield is down 9bps at 0.408%, 5-Yr is down 9.5bps at 0.565%, 10-Yr is down 9.9bps at 0.845%, and 30-Yr is down 12.8bps at 1.016%.

- Italian BTP spread unchanged at 115.7bps / Greek up 2.9bps at 136.9bps

EGB Options: Mixed Sterling Trade Post-BoE

Friday's rates / bonds options flow included:

- DUZ1 112.20/30/40 call fly sold at 3.5 in 1.5k

- RXZ1 174 call bought for 5 in 4k

- RXF2 173/175 1x2 call spread sold at 28.5/29 in 1.5k

- ERZ1 100.62/100.87cs, bought for 0.25 in 20k (vs 100.48 in June22, 5del)

- SFHI2 99.85/99.95/100 broken call flys sold at 0.5 exit, in 59k

- SFIH2 99.50/99.65/99.80c fly, bought for 3 in 3k

- 2LZ1 99.12/99.00ps sold at 10.25 in 10k

- 2LZ1 98.75/98.50ps, bought for 6 in 5k

- 3LZ1 98.62/97.75 p strip, bought for 8.5 in 5k

FOREX: Narrow Ranges for G10FX, EURUSD Fresh Year Lows As 1.1500 Support Holds

- A solid NFP print with complimentary stellar revisions initially boosted the US dollar on Friday. However, major currencies lacked the appetite for any sustained reactions, prompting the greenback to gradually unwind throughout the remainder of the session.

- This price action was mirrored by EURUSD, making fresh 2021 lows post the data at 1.1514. Strong support at the 1.15 handle capped the dollar strength and the pair reversed back to 1.1550. The focus will remain on 1.1493, the 50.0% retracement of the Mar '20 - Jan '21 bull phase. A break of this level will be needed to confirm the resumption of the underlying downtrend.

- The gradual unwinding of dollar strength supported the Japanese Yen, which was the clear outperformer on Friday, rising 0.35%. If USDJPY were to close here around 1.1340, it would be the lowest daily close since October 13. Clearance of the 1.1300 support zone would signal scope for a deeper pullback and open 112.08, Sep 30 high and a recent breakout level.

- The bolstered risk profile was most evident in the emerging market currency space, with the JPMorgan EM Currency Fund up 0.62% approaching the close. Notable +1% rallies in MXN and ZAR underpinned the improved sentiment.

- Lots of Fed speakers, including Chair Powell, kick off a data light Monday next week. Wednesday's US CPI data will headline the calendar before the North American holiday on Thursday.

EQUITIES

Key late session market levels

- DJIA up 195.54 points (0.54%) at 36328.02

- S&P E-Mini Future up 17.75 points (0.38%) at 4691.75

- Nasdaq up 28.5 points (0.2%) at 15970.8

- EuroStoxx 50 up 29.7 points (0.69%) at 4363.04

- FTSE 100 up 24.05 points (0.33%) at 7303.96

- German DAX up 24.71 points (0.15%) at 16054.36

- French CAC 40 up 53 points (0.76%) at 7040.79

COMMODITIES

- WTI Crude Oil (front-month) up $2.57 (3.26%) at $81.32

- Gold is up $22.29 (1.24%) at $1814.32

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok