Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

US TSYS: Tsy Futures Back To Early Nov Levels, Data Picks Up Tuesday

Carry-over moderate support for rates overnight dissipated quickly after the NY open, initially triggered by weaker German Bunds Monday. No obvious headline trigger on moves as rate futures continued to make new lows after the close while equities traded mildly lower (ESZ1 -2.5).- Some desks cited higher yields for weaker stocks, while former Fed pres' Dudley and Lacker interview on Bbg TV didn't help: estimated rates could rise to 3-4% while Lacker said "It seems to be plausible we get to 3.5% or 4% and in addition that we push the economy into a recession."

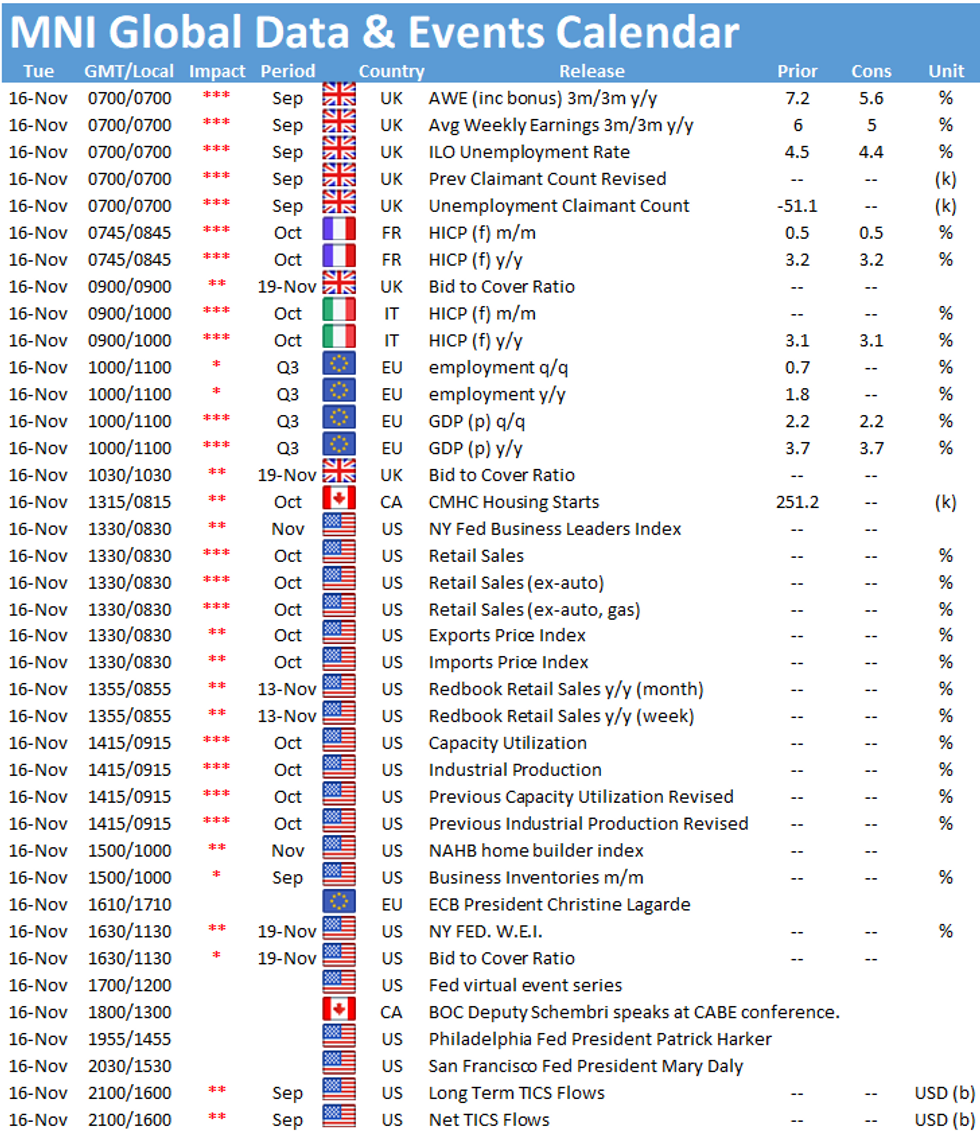

- Limited data: NY Empire State Manufacturing survey was stronger than expected in November, bringing with it further inflationary pressures; mfg business conditions index was above consensus in Nov, up from 19.8 to 30.9 (survey 22). Focus on Tue's Retail Sales, Import/export prices, IP/Cap-U.

- Tsys drew sporadic fast$ buying covering tactical shorts, two-way deal-tied hedging/unwinds, while larger theme remains better real$ and bank portfolio selling in 10s and 30s as volumes gradually improved. Yield curves bear steepened as Tsy futures slipped back to early Nov levels (5s30s well off early Fri's 63.704 low to 75.673 in late trade).

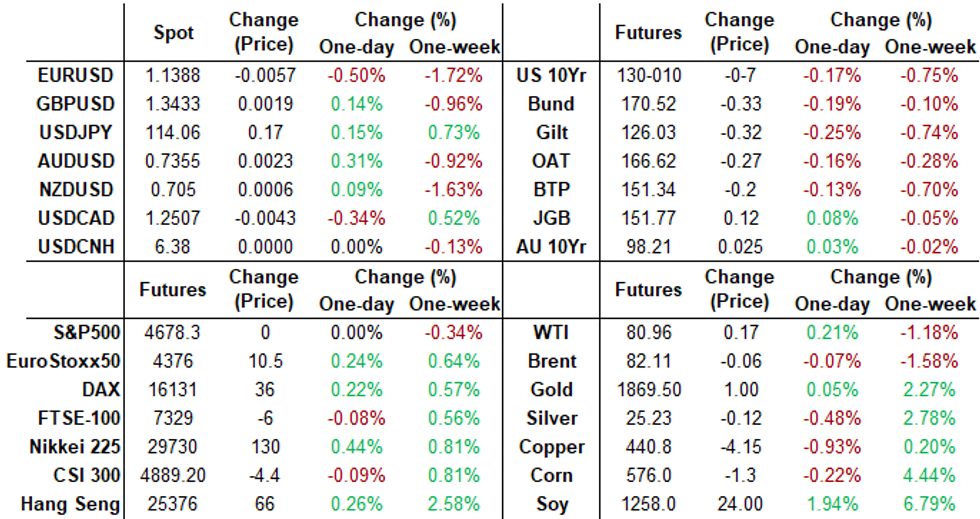

- The 2-Yr yield is up 0.6bps at 0.5177%, 5-Yr is up 3.1bps at 1.2522%, 10-Yr is up 5.7bps at 1.618%, and 30-Yr is up 7bps at 2.0008%.

SHORT TERM RATES

US DOLLAR LIBOR: Latest settlements

- O/N +0.00025 at 0.07500% (+0.00212 total last wk)

- 1 Month +0.00200 to 0.09113% (+0.00050 total last wk)

- 3 Month +0.00288 to 0.15788% (+0.00550 total last wk) ** Record Low 0.11413% on 9/12/21

- 6 Month -0.00062 to 0.22538% (_0.01087 total last wk)

- 1 Year -0.00425 to 0.39425% (+0.04875 total last wk)

- Daily Effective Fed Funds Rate: 0.08% volume: $74B

- Daily Overnight Bank Funding Rate: 0.07% volume: $264B

- Secured Overnight Financing Rate (SOFR): 0.05%, $868B

- Broad General Collateral Rate (BGCR): 0.05%, $343B

- Tri-Party General Collateral Rate (TGCR): 0.05%, $324B

- (rate, volume levels reflect prior session)

- Tsy 0Y-2.25Y, $10.851B accepted vs. $39.274B submission

- Next scheduled purchases

- Tue 11/16 1010-1030ET: Tsy 4.5Y-7Y, appr $5.275B

- Tue 11/16 1100-1120ET: Tsy 10Y-22.5Y, appr $1.425B

- Thu 11/18 1010-1030ET: Tsy 22.5Y-30Y, appr $1.600B

- Fri 11/19 1010-1030ET: TIPS 1Y-7.5Y, appr 1.775B

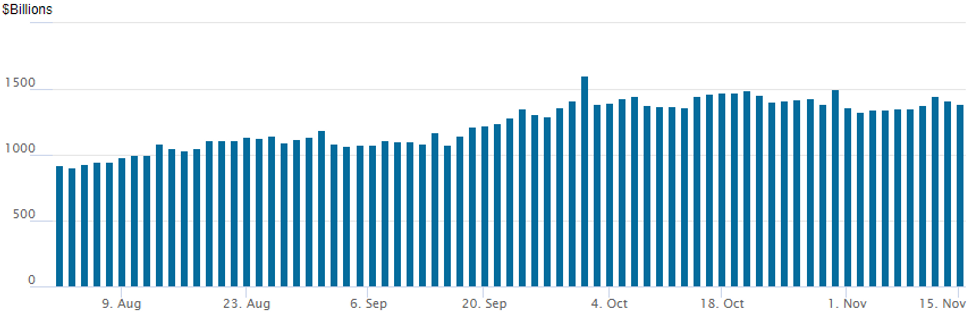

FED Reverse Repo Operation

NY Fed reverse repo usage recedes: $1,391.657B from 78 counterparties vs. $1,417.643B on Friday. Record high remains at $1,604.881B from Thursday, September 30.

EURODOLLAR/TREASURY OPTIONS SUMMARY

Eurodollar Options:- Block, 13,125 1Y midcurve wk4 99.12 calls, 4.5 at 1109:08ET

- 4,750 short Dec 98.81/99.00 2x1 put spds

- Block, 10,000 Green Dec 98.00/98.18/98.37 put trees, 4.0 at 0913:46ET

- Block, 10,000 Green Dec 98.00/98.18/98.37 put trees, 4.0

- Overnight trade

- 7,880 Apr 99.00/99.25/99.37 put flys

- 8,000 short Dec 98.87/99.00 put spds

- 3,650 short Mar 98.75/99.00/99.25 put flys

- Block: 6,000 short Dec 98.87/99.00 put spds, 3.0 at 0542:28ET

- 4,000 FVF 122 calls, 9.5, total volume>17.2k

- total 24,000 TYF 129.5 puts, 52-56

- 6,000 TYF 127.5 puts, 17

- +9,000 TYH2 127 puts, 34 (open interest only 15,569 coming into the session)

- Block +10,000 TYZ 130 puts, 12 at 0736:41ET

- +10,000 TYZ 129.5/130/130.5 put flys, 4.0

- +10,000 TYZ 129 puts, 3

- +7,000 TYZ 130.25 puts, 14-15

FOREX: Single Currency Spiked on Re-Routing of Rate Expectations

- Several central bankers further reinforced the yawning gap in EZ/UK rate expectations Monday, with the ECB President Lagarde stating that a rate hike in 2022 - as markets are currently pricing - would be very unlikely. This was in stark contrast to an appearance from the BoE governor Bailey, who stressed that a December rate hike was still in play, with incoming labour market data crucial for the next decision.

- EUR/GBP resultingly corrected lower, with the 50-day EMA support giving way ahead of the close. Recent price action has worked well against a previously bullish near-term outlook, opening initial firm support at 0.8463, Nov 3 low.

- Elsewhere, a re-steepening of the US yield curve worked in favour of the greenback, which rose against most others and got a decent leg up from the downside in EUR/USD. The USD Index now sits at its best levels since mid-2020, prompting focus to turn to the Fed speakers due throughout the week, with Clarida's appearance Friday possibly being most interesting.

- UK jobs data takes focus Tuesday, with US retail sales and import/export price indices also on the docket. Markets see little progress being made between Xi and Biden at their virtual summit, but markets will be on watch for any comments on trade or diplomatic relations.

- Central bank speakers include Fed's Bullard, ECB's Lagarde and BoC's Schembri.

FX: Expiries for Nov16 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1450(E695mln), $1.1539-50(E892mln), $1.1600-25(E1.4bln)

- USD/JPY: Y113.40-50($1.3bln), Y114.30($1.6bln)

- GBP/USD: $1.3495-00(Gbp500mln)

- EUR/GBP: Gbp0.8525(E791mln)

- AUD/USD: $0.7300-15(A$757mln)

- USD/CAD: C$1.2370-90($830mln)

- USD/CNY: Cny6.4000($2.3bln); Cny6.4390-00($1.3bln)

EQUITIES: Growth Stocks Lead Decline as Yield Curve Steepens

- Worth noting the pullback in US equity prices in recent trade - no headlines crossing to prompt the move but does coincide in a decent uptick in volumes. Just over 10k contracts in the e-mini S&P changing hands at 1642GMT/1142ET which appeared to trigger weakness.

- No material newsflow or headlines behind the break lower for stocks but worth noting the underperformance in the NASDAQ future - so growth names particularly hurt by the run-up in US yields/steepening of the curve.

- US 10y yield remains highers by over 5bps on the session as the curve steepens - 10y yield now highest since late October.

COMMODITIES: WTI, Brent Roll Off Friday High as USD Bears Down

- WTI and Brent crude futures traded in negative territory Monday, with both benchmarks shedding around 1%, with the largest pullbacks noted in the front-end of the futures curve.

- USD strength and a moderation in equity prices was largely to blame, easing WTI futures to drop below $80/bbl for the first time since Nov 5. Key short-term support has been defined at $78.25 Nov 4 low. A break would be bearish.

- Gold rallied sharply higher last week and remains firm. The move higher resulted in a clear break of resistance at $1834.0, Sep 3 high. The breach of this hurdle reinforces current bullish conditions and paves the way for further strength. Note too that the yellow metal has also breached $1863.3, 76.4% of the Jun - Aug sell-off. The focus is on $1877.7 next, Jun 14 high.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok