Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

US TSYS: Risk Appetite Improves Ahead Holidays

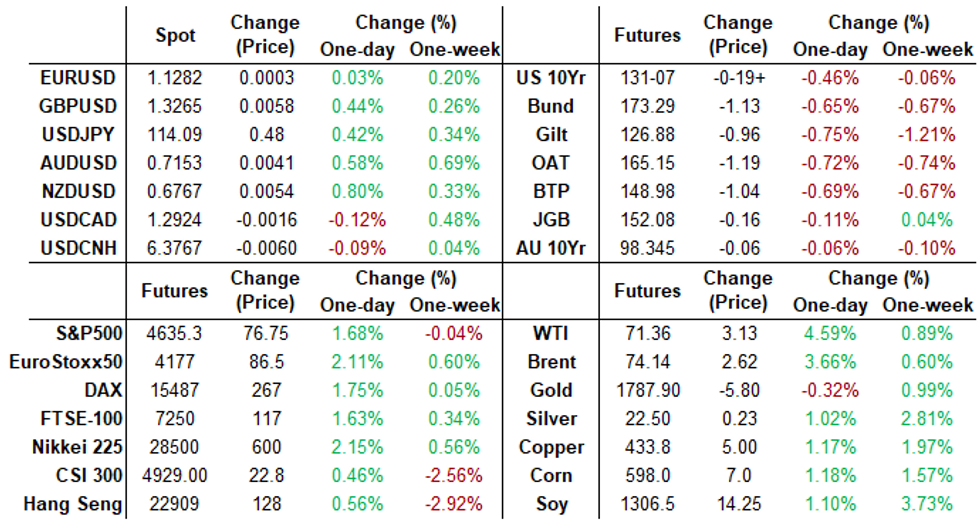

Risk appetite improved early Tuesday amid cooling concerns over Covid curbs in London: UK PM Johnson stating no new restrictions before Christmas. Meanwhile, World Health Organization message a little darker: Meanwhile WHO message: "Omicron is gaining ground: PROTECT, PREVENT, PREPARE".- Risk-on tone carried over to US markets with Tsys yields climbing (30YY tapped 1.9246% high) and stocks climbing: ESH2 climbed to 4638.75 high in late trade, DJIA up over 500.0, and West Texas Crude held near 71.50 high (+2.89).

- US Pres Biden address re: Covid response not market moving as he reiterated importance of being vaccinated and receiving booster; +10,000 new vaccine sites to 90k, more pop-up sites coming in January 2022.

- Rates bounced off lows (yield curves reversed steeper levels) amid moderate hedge unwind volumes after the 20Y Bond performed better than expected (1.942% high yield vs. 1.964% WI). Indirect take-up climbed to yr high of 64.83% (matching October's) vs. Nov's 60.18%; direct bidder take-up also yr high of 20.83% while primary dealer take-up receded to yr low of 14.34% vs. 19.36% 5-month avg.

- The 2-Yr yield is up 3.7bps at 0.6685%, 5-Yr is up 5.7bps at 1.2238%, 10-Yr is up 5.1bps at 1.4737%, and 30-Yr is up 2.9bps at 1.8805%.

SHORT TERM RATES

US DOLLAR LIBOR: Latest settlements

- O/N +0.00038 at 0.07288% (-0.00138/wk)

- 1 Month +0.00075 to 0.10425% (+0.00175/wk)

- 3 Month +0.00175 to 0.21600% (+0.00338/wk) ** Record Low 0.11413% on 9/12/21

- 6 Month +0.00887 to 0.32550% (+0.01275/wk)

- 1 Year +0.01012 to 0.54200% (+0.01238/wk)

- Daily Effective Fed Funds Rate: 0.08% volume: $72B

- Daily Overnight Bank Funding Rate: 0.07% volume: $259B

- Secured Overnight Financing Rate (SOFR): 0.04%, $905B

- Broad General Collateral Rate (BGCR): 0.05%, $337B

- Tri-Party General Collateral Rate (TGCR): 0.05%, $324B

- (rate, volume levels reflect prior session)

- TIPS 7.5Y-30Y, appr $899M accepted vs. $979M submission

- Next scheduled purchases

- Wed 12/22 1010-1030ET: Tsy 10Y-22.5Y, appr $1.625B

- NY Fed buy-operations pause for holidays, resume Jan 3

FED Reverse Repo Operation

NY Federal Reserve/MNI

After climbing to four consecutive new highs, NY Fed reverse repo usage recedes to $1,748.285B from 77 counterparties vs. Monday's record high of $1,758.041B.

EURODOLLAR/TREASURY OPTIONS SUMMARY

Eurodollar Options:- 8,300 Dec 99.75 calls, 2.5

- 2,500 Mar 99.81/99.87 call spds

- Update, +30,000 short Jan 98.56/98.68 put spds, 3

- -5,000 Green Mar 97.75/98.00 put strip, 7.5

- -2,000 Sep 99.00/99.25/99.50 put flys, 5

- Overnight trade

- 10,850 Jun 99.43/99.62 put spds

- 2,500 short Mar 98.50 puts

- -5,000 TYG 132.5/133.5 call spds, 6.0

- -5,000 TYH 129/133.5 strangles, 39-40

- -2,000 TYH 128.5/129.5 put spds, 14 vs. 130-28/0.10

- +2,500 USH 168 calls, 32

- +5,000 TYH 127.5/128.5 put spds, 9

- Overnight trade

- 7,000 TYF 131 puts, 14 last

- 6,600 TYF 130.5 puts, 3

- 5,200 TYF 131.5 calls, 3

- +3,500 TYG 130.5 puts. 34

- 3,400 TYH 131.5 calls, 49 last

- 4,100 FVG 122 calls, 11.5-12.5

EGBs-GILTS CASH CLOSE: No Lockdown For Core Yields

European yields rose sharply Tuesday with bear steepening in Gilts and Bunds as equities gained, energy prices soared, and concerns over arduous holiday season lockdowns eased.

- Europe gas and power prices hit fresh all-time highs, weighing particularly on Bunds.

- The Sun reported UK PM Johnson would announce within 48 hours whether the gov't was initiating a "circuit breaker"; on the cash close he confirmed prevailing wisdom that there would be no further restrictions before Christmas. Gilts underperformed Bunds; FTSE futures reached best levels since Dec 13; European stocks 1-2% higher.

- ECB's Kazimir warned of risks of higher inflation in the near term. And the ECB made its final asset purchases of 2021 today.

- Germany: The 2-Yr yield is up 3.4bps at -0.698%, 5-Yr is up 5bps at -0.562%, 10-Yr is up 6.2bps at -0.304%, and 30-Yr is up 7.7bps at 0.068%.

- UK: The 2-Yr yield is up 7.5bps at 0.617%, 5-Yr is up 8.2bps at 0.722%, 10-Yr is up 10.1bps at 0.873%, and 30-Yr is up 10.7bps at 1.059%.

- Italian BTP spread up 1.7bps at 131.3bps / Greek down 1.3bps at 159.2bps

EGB Options: Several German Put Spreads

Tuesday's Europe rates / bond options flow included:

- RXG2 173.00/171.00 1x2 put spread bought for 23 in 2k

- RXG2 172.50/171.00 put spread bought for 36.5 in 3k

- DUG2 112.20/112.00 put spread bought for 6 in 6.7k

- DUH2 112.10/112.00/111.90 put fly bought for 1.25 in 3.5k

FOREX: Risk-On Bolsters Cross-JPY Recovery

- After treading water for the majority of European trade, USDJPY surged back above 114 as markets welcomed a firmer session for risk sentiment, evident by higher equity and commodity indices.

- The half percent rally fell just short of the December highs. Clearance of 114.26, Dec 15 high is needed to offset any developing bearish technical concerns.

- Stronger gains were seen in cross-yen as the Australian dollar, Kiwi and GBP all benefitted substantially from the renewed optimism in global markets. NZDJPY was the strongest on the board, rising 1.2% with the others following close behind. Firmer crude futures also boosted the Norwegian Krona over 1%.

- For a second consecutive session, the dollar index registered marginal losses, as the greenback lacks momentum in either direction as the holiday approaches.

- In similar fashion, EURUSD obeyed narrow parameters between 1.1260-1.1300 as the bounce in commodity/risk tied FX remained in focus.

- Another wild ride in emerging markets as USDTRY continues to trade in a very volatile manner, following Erdogan’s new plans to halt dollarization. Posting just shy of a 23% intra-day range, the pair looks likely to close the day 3% lower around 12.95.

- BoJ minutes overnight before some final GDP readings out of the UK and the US, however, the data docket remains light. Thursday’s US Core PCE Price Index will be the final point of focus before the extended break.

FX: Expiries for Dec22 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1190-05(E1.0bln), $1.1245-50(E939mln), $1.1280-00(E891mln), $1.1335-50(E1.3bln)

- GBP/USD: $1.3245(Gbp659mln), $1.3265-90(Gbp1.1bln)

- USD/JPY: Y113.00($638mln), Y113.45-50($870mln), Y113.70-85($711mln)

EQUITIES: Stocks Rebound Off Monday Lows, But Bounce Remains Shallow

- Wall Street equity markets traded uniformly positively Tuesday, staging a bounce off the Monday lows to boost the three major indices by as much as 1.5%. The S&P 500 traded a good 2% or more above the Monday lows, although the rally stopped short of challenging Friday's highs and Friday's open, which hold at 4668.00 and 4664.00. These levels need to give way before a more solid recovery can set in.

- Given the stabilisation in headline equity markets, the VIX extended the slip off the Monday high, dropping near 2 points to trade either side of the 21 handle.

- Monday's laggards, the financials and energy sector, were the outperformers Tuesday, driving the bounce as crude oil prices recovered and the US sovereign curve steepened. Re-opening names traded particularly well, with the likes of Live Nation Entertainment, Norwegian Cruiselines and United Airlines among the index's best performers. Conversely, vaccine makers Pfizer and Moderna were the two worst performing stocks on the day, dropping over 4% apiece.

- Europe follows the lead in the US, with continental markets finishing with solid gains. Peripheral Europe rallied sharply, with Italian and Spanish bourses adding 1.8%.

COMMODITIES: Oil Up With Risk-On But Overshadowed By Gas

- Oil futures are up ~3.5% today on broader risk-on sentiment that has extended throughout the day.

- WTI is +3.7% at $71.2, moving through the initial resistance of $69.98 and next eyeing up $73.13/14 (Dec 9 high/50-day EMA). Support is seen at $66.12 (Dec 20 low).

- $75/bbl calls have been the most active strikes today for the G2 (Feb’22) contract, followed by $60/bbl puts.

- Brent +3.3% at $73.9, with resistance seen at $74.68 (20-day EMA) and first support at $69.24 (Dec 3 low).

- Gas prices meanwhile have spiked more than 20% in Europe on a combination of Russia reducing gas flows and higher demand from both colder temperatures and plugging the renewables gap from low winds.

- US heating gas is up a more modest +1% on cooler weather forecast but remains relatively depressed compared to the elevated Sep-Nov levels.

- Gold has softened in recent trading to be down -0.2% on the day at $1787.2. It eyes $1771.4, the base of the bull channel drawn from the Aug 9 low, whilst resistance is seen at $1815.6, the Nov 26 high.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok