Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

US TSYS: Rates Surge, March 50Bp Liftoff Cools, Geopol, Policy Risk Events Ahead

FI Markets very well bid after the bell, 30Y Bonds topping early overnight gap bid late; yield curves bull steepening: 5s30s +4.081 at 44.62. 30YY currently 2.1674% -0.1064 vs. 2.1618% late session low (2.2507% high).

- Russia invasion of Ukraine main driver for risk-off support in rates. Trading desks report preop, fast- and real$ buying 5s, continued foreign and domestic real$ and bank portfolio buying in 10s-30s.

- Short end funding concerns heat up w/3M FRA/OIS gap wider overnight, tapped 23.80 around Asia/London cross, gradually receding since: currently 18.40 +5.30 vs. late Fri.

- Bostic reiterated need to "move off emergency rate stance", is supportive of 25bps hike at the March 16 FOMC -- unless inflation measures continue to climb -- opens the possibility of 50bp liftoff.

- Wide, near 0.100 range in lead quarterly Mar'22 Eurodollar futures, near highs as 50bps liftoff inches lower. Reds-Gold surge 0.14-0.20 higher by the close. Large Block buys+50k EDH2 99.335, +50K EDU2 98.525, +20k EDM 98.92.

- US Pres Biden State of the Union Address Tue evening 2100ET

- Fed Chair Powell will be giving the semi-annual monetary policy report testimony to the House Financial Services Committee on Weds March 2 and the Senate Banking Committee on Thu March 3 - 1000ET.

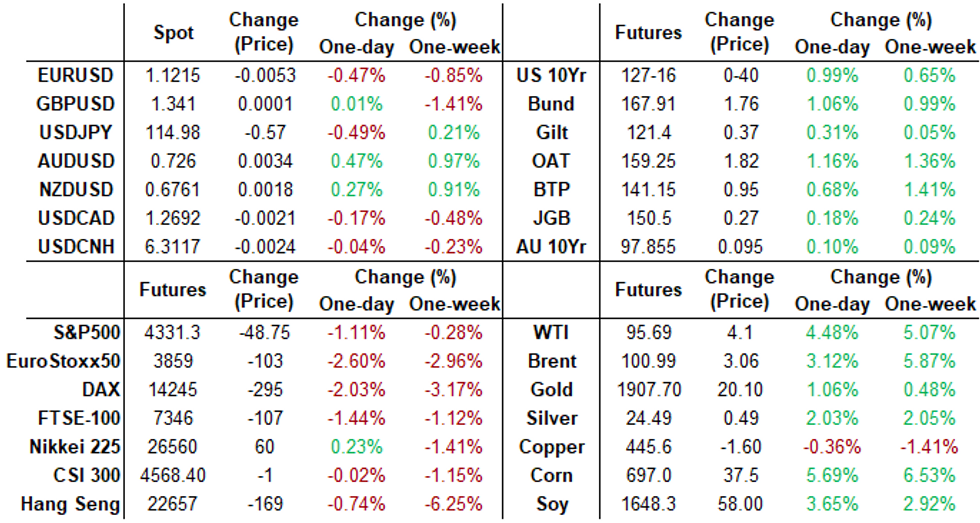

- The 2-Yr yield is down 14.1bps at 1.4283%, 5-Yr is down 14.6bps at 1.7194%, 10-Yr is down 12.6bps at 1.8353%, and 30-Yr is down 9.9bps at 2.1745%.

SHORT TERM RATES

US DOLLAR LIBOR: Latest settlements:

- O/N +0.00000 at 0.07714% (+0.00157 total last wk)

- 1 Month +0.01086 to 0.24143% (+0.05986 total last wk)

- 3 Month -0.01871 to 0.50429% (+0.04343 total last wk) ** Record Low 0.11413% on 9/12/21

- 6 Month -0.02400 to 0.80471% (+0.04742 total last wk)

- 1 Year -0.04271 to 1.28800% (+0.04485 total last wk)

STIR: FRBNY EFFR for prior session:

- Daily Effective Fed Funds Rate: 0.08% volume: $69B

- Daily Overnight Bank Funding Rate: 0.07% volume: $249B

US TSYS: Repo Reference Rates

- Secured Overnight Financing Rate (SOFR): 0.05%, $962B

- Broad General Collateral Rate (BGCR): 0.05%, $364B

- Tri-Party General Collateral Rate (TGCR): 0.05%, $347B

- (rate, volume levels reflect prior session)

NY Fed Purchase Operation: The Desk plans to purchase approximately $20 billion, ending Thu, March 9.

- Next scheduled purchases

- Tue 03/01 1100-1120ET: TIPS 7.5Y-30Y, appr $0.625B vs. $1.225B prior

- Thu 03/03 1100-1120ET: Tsy 7Y-10Y, appr $1.625B vs. $3.225 prior

- Tue 03/08 1010-1030ET: Tsy 22.5Y-30Y, appr $1.825B steady

- Thu 03/09 1010-1030ET: Tsy 2.25Y-4.5Y, appr $4.025B

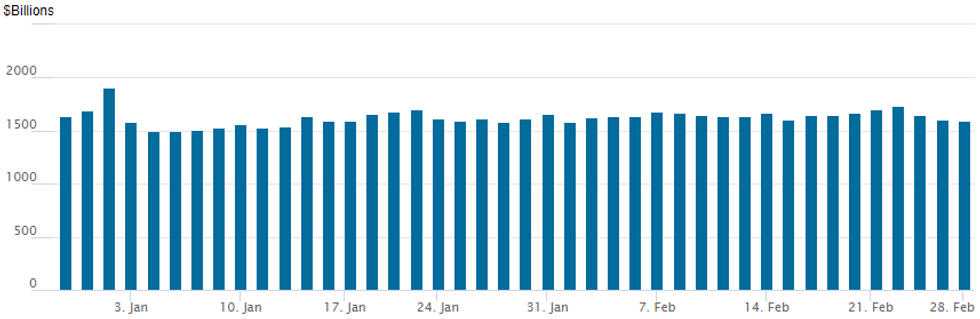

FED Reverse Repo Operation

NY Federal Reserve/MNI

NY Fed reverse repo usage recedes to $1,596.052B w/ 82 counterparties vs. $1,603.349B prior session -- remains well off all-time high of $1,904.582B on Friday, December 31.

EURODOLLAR/SOFR/TREASURY OPTIONS SUMMARY

SOFR Options- Block, 10,000 SFRM2 98.00 straddles, 91.0

- Block, 10,000 SFRH2 98.12 straddles, 80.0

- Block, 10,000 Dec 98.12/98.75 put spds, 34.5 vs. 98.24/0.26%

- +10,000 short Jun 99.00 calls, 2.0 vs. 97.92/0.05%

- +5,000 Dec 98.00/98.25 0.0 over 99.00 calls vs. 98.235/0.25%

- +10,000 Dec 99.62 calls, 3.0-3.5

- -8,000 Jun 97.62/97.87 put spds, 8.5-8.0

- -10,000 Jun 98.81/98.93/99.00/99.18 call condors, 1.0 (unwind), paper also long May condor in size

- +10,000 Dec 99.00 calls, 9.5-8.5 vs. 98.18-.21

- +1,000 Jun 98.87 straddles, 37.0

- Overnight trade

- +4,000 Mar 99.31/99.37 1x2 call spds, 0.25

- +7,500 Dec 99.00 calls, 8.5 vs. 98.17/0.17%

- +8,000 Dec 97.00/98.87 call over risk reversals, 0.0

- +4,000 Green Mar 97.50/97.62/97.75 put flys, 1.5-2.0

- +15,000 TYJ 130 calls, 12-13

- +22,500 TYJ 130 calls, 10 after buying 4k at 9

- +4,000 TYJ 130 calls, 9

- -10,000 FVK 114.5/116 put spds, 6.5-6.0

- 3,000 FVK 115.75/116.5 put spds

- -12,000 TYM 127/129 1x2 call spds, 9-8 1-leg over

- +5,000 TYM 129 calls, 39

- Overnight trade

- +30,000 TYJ 129 calls, 11-12

- -7,000 wk1 TY 126.5/127 call spds, 17-16

FOREX: Initial USD Strength Unwinds, Swiss Franc Outperforms

- The US Dollar Index gapped higher at the Sunday night open amid severe pressure on equities as geopolitical developments weight on global risk sentiment over the weekend.

- Throughout the course of Monday trading, amid the recovery in global equity benchmarks, the greenback gradually edged lower, erasing almost the entirety of the gap to Friday’s close.

- The Swiss Franc had the most notable move on Monday with EURCHF currently within a few pips of Thursday’s lows at 1.0279, a breach of which would see the pair at the lowest levels since 2015.

- Commodity gains, and in particular the four percent gains in crude futures, prompted strong recoveries from the likes of AUD, NZD and CAD, all bridging the gaps at the open and extending their resilient performances throughout US trading hours.

- Despite a firm bounce for the euro, the single currency remains around 0.5% lower against the dollar. EUR underperformance largely down to the struggling crosses such as EURJPY (-1.05%) and EURCHF (-1.42%).

- FX hedging activity via options surged on Monday, with markets rushing to hedge EUR exposure vs. both USD and AUD aswell as USD/CNY across Asia-Pac hours.

- Options volumes are running higher alongside implied volatility metrics, with front-month implieds for EUR/USD nearing 8.50 points for the first time since H2 2020.

- Risk reversals contracts tell us that markets are favouring EUR/USD downside protection, with markets now pricing a 29.3% implied probability for the pair to trade below 1.11 in one month's time (a horizon that captures both the next Fed and ECB rate decisions). This implied probability was just 16.6% this time last week.

- While the USD/RUB rate did gain as much as 35%, the CBR's snap decision to more than double domestic interest as well as the rebound in broader sentiment did support the Ruble off it’s worst levels as Monday progressed.

- Overnight Chinese manufacturing PMI data will kick off the Asia-Pac session before the March RBA meeting/decision, where little adjustment to the RBA’s tone is expected.

EQUITIES: More Sell-Programs After Attempting Revisit Midday Highs

Stocks modestly weaker, Dow underperforming with global bank shares w/exposure to Russia under pressure (JPM -3.58% at 142.66; GS -2.56 at 341.23) . Nasdaq leading SPX again as pair see renewed pressure: recent sell programs

Inside session range for Tsys near highs w/ yield curves bull steepening (30YY currently 2.1928, -.0810), Gold off highs +$9.34 (0.49%) at $1898.68, WTI crude +$4.64 (5.07%) at $96.26.

- SPX Eminis tapped 4384.25 earlier, currently 54.75 points (-1.25%) at 4337.75; Dow Industrials -396.21 points (-1.16%) at 33658.23; NASDAQ 54.6 points (-0.4%) at 13638.3.

- SPX leading sectors:

- Energy +1.41%

- Industrials +.07%

- Lagging: Real Estate -1.99%, Consumer Staples -1.92%

COMMODITIES: Oil And Gold Ease Intraday, But Still Up Strongly

- Crude oil has traded flat to lower for most of today but is still up sharply from Fri close levels following new sanctions over the weekend including the targeted use of SWIFT withdrawal.

- Peace talks between Russia-Ukraine finished with Russia saying Ukraine has agreed to another round of talks. Earlier news of the U.S. and allies considering the release of 60 million barrels to combat high prices made relatively little impact.

- WTI is +4.3% at $95.5 and has confirmed a resumption of the underlying uptrend and an extension of the bullish price sequence of higher highs and higher lows. Resistance remains $100.54 (Feb 24 high) whilst key support is seen at $90.06 (Feb 23 low).

- Brent is +3.2% at $101.1, also in an uptrend for now even if prices continue to trade below the Feb 24 high of $105.79. Support is seen at $96 (Feb 25 low).

- Gold has fluctuated today on perceived progress with the peace talks but has remained above Friday's close the whole time, currently up strongly with +0.7% at $1903.34. The outlook remains bullish following recent gains but its back inside its bull channel drawn from the Aug 9, 2021 low, which gives key short-term resistance at $1940.1.

- Elsewhere, European natural gas prices saw further large increases, with Apr22 contracts up nearly 6% on the day and standing 40% higher ytd.

Tuesday Data Calendar

| Date | GMT/Local | Impact | Flag | Country | Event |

| 01/03/2022 | 0030/1130 |  | AU | Balance of Payments: Current Account | |

| 01/03/2022 | 0030/1130 | ** | | AU | Lending Finance Details |

| 01/03/2022 | 0030/0930 | ** |  | JP | IHS Markit Final Japan Manufacturing PMI |

| 01/03/2022 | 0145/0945 | ** |  | CN | IHS Markit Final China Manufacturing PMI |

| 01/03/2022 | 0330/1430 | *** | | AU | RBA Rate Decision |

| 01/03/2022 | 0730/0730 |  | UK | DMO Gilt Operations Announcement W/C 4/11 April | |

| 01/03/2022 | 0815/0915 | ** |  | ES | IHS Markit Manufacturing PMI (f) |

| 01/03/2022 | 0845/0945 | ** |  | IT | IHS Markit Manufacturing PMI (f) |

| 01/03/2022 | 0850/0950 | ** |  | FR | IHS Markit Manufacturing PMI (f) |

| 01/03/2022 | 0855/0955 | ** |  | DE | IHS Markit Manufacturing PMI (f) |

| 01/03/2022 | 0900/1000 | ** |  | EU | IHS Markit Manufacturing PMI (f) |

| 01/03/2022 | 0900/1000 | *** | | DE | Bavaria CPI |

| 01/03/2022 | 0930/0930 | ** | | UK | BOE M4 |

| 01/03/2022 | 0930/0930 | ** | | UK | IHS Markit/CIPS Manufacturing PMI (Final) |

| 01/03/2022 | 0930/0930 | ** | | UK | BOE Lending to Individuals |

| 01/03/2022 | 1000/1100 | *** | | IT | HICP (p) |

| 01/03/2022 | 1000/1100 | *** | | DE | Saxony CPI |

| 01/03/2022 | - | | EU | ECB Panetta at G7 Finance Ministers/CB Governors Meeting | |

| 01/03/2022 | - | *** |  | US | domestic made vehicle sales |

| 01/03/2022 | 1300/1400 | *** | | DE | HICP (p) |

| 01/03/2022 | 1300/1400 | | EU | ECB Lagarde visits Chancellor Scholz | |

| 01/03/2022 | 1330/0830 | * | | US | construction spending |

| 01/03/2022 | 1330/0830 | *** |  | CA | GDP - Canadian Economic Accounts |

| 01/03/2022 | 1355/0855 | ** | | US | Redbook Retail Sales Index |

| 01/03/2022 | 1445/0945 | *** | | US | IHS Markit Manufacturing Index (final) |

| 01/03/2022 | 1500/1000 | *** | | US | ISM Manufacturing Index |

| 01/03/2022 | 1830/1830 | | UK | BOE Saunders speech at East Anglia University | |

| 01/03/2022 | 1900/1400 | | US | Atlanta Fed's Raphael Bostic | |

| 01/03/2022 | 1900/1900 | | UK | BOE Mann panels Cleveland Fed discussion | |

| 01/03/2022 | 1900/1400 | | US | Cleveland Fed's Loretta Mester |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.