Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

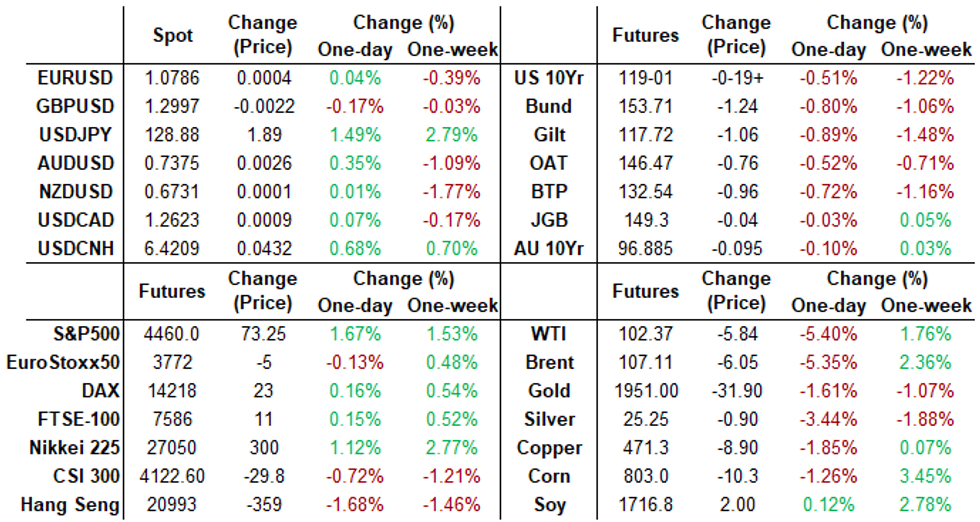

US TSYS: Tsy Yld Surge: 30YY at 3.016%, 3Y Highs

Rates trading near session lows after the bell -- yield curves bear flattening after tapping 2-week highs in early trade.

- Fresh cycle lows after slightly stronger than forecasted Housing Starts (1.793M) and Building Permits (1.873M) for March.

- Yield curves reversed late overnight steepening, extending flatter amid heavy selling in short end since the open: 2YY surging to 2.6102% high from 2.4273% low. 2s10s curve hit inverted low of -9.561 two weeks ago topped out at 42.897 this morning is trading 33.590 at the moment. 30YY tops 3.0161% - appr 3-year highs.

- Early blocks contributing (-2s/ultra bond, outright sale 2s) as recession concerns, ability of Fed to engineer a soft landing being sapped after leading hawk StL Fed Bullard opened dialog on chance of 75bp hike at May 4 FOMC late Monday.

- Late rebuttal from Chicago Fed Evans and Atl Fed Bostic -- neither see more than a 50bp hike in the near term as necessary.

- Meanwhile, IMF joined World bank opinion from late Monday: knock-on effect of Russia invasion reducing global growth/increase inflation forecasts.

- Cross asset levels: Gold selling off after nearly topping $2,000 Mon, -31.3 at 1947.5; support for Crude cools: WTI -5.53 at 102.68.

- On tap for Wednesday: Existing Home Sales (6.02M, 5.78M); MoM (-7.2%, -4.0%) at 1000ET, more Fed speak ahead late Friday blackout.

SHORT TERM RATES

US DOLLAR LIBOR:Latest settlements resume with London back from holiday

- O/N +0.00871 at 0.33100% (-0.00529 total last wk)

- 1 Month +0.03028 to 0.62471% (+0.08043 total last wk)

- 3 Month +0.03558 to 1.09829% (+0.05200 total last wk) ** Record Low 0.11413% on 9/12/21

- 6 Month +0.05043 to 1.60714% (+0.01628 total last wk)

- 1 Year +0.08100 to 2.30257% (-0.05000 total last wk)

STIR: FRBNY EFFR for prior session:

- Daily Effective Fed Funds Rate: 0.33% volume: $76B

- Daily Overnight Bank Funding Rate: 0.32% volume: $263B

US TSYS: Repo Reference Rates

- Secured Overnight Financing Rate (SOFR): 0.29%, $896B

- Broad General Collateral Rate (BGCR): 0.30%, $349B

- Tri-Party General Collateral Rate (TGCR): 0.30%, $338B

- (rate, volume levels reflect prior session)

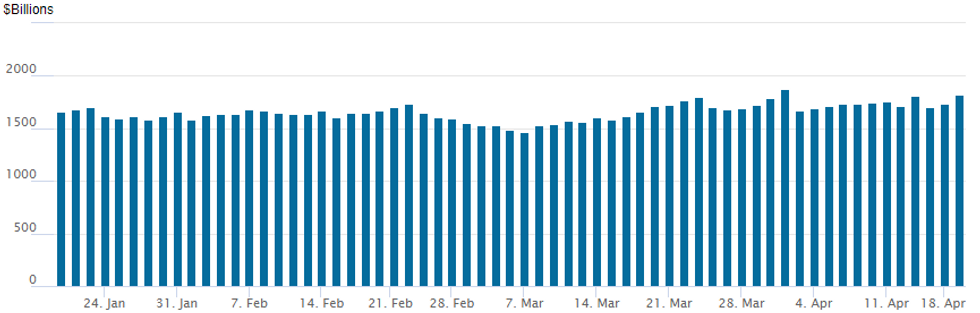

FED Reverse Repo Operation

NY Federal Reserve/MNI

NY Fed reverse repo usage climbs to 1,817.292B w/ 80 counterparties from prior session 1,738.379B. Compares to all-time high of $1,904.582B on Friday, December 31.

EURODOLLAR/SOFR/TREASURY OPTIONS SUMMARY

Option volumes resumed more normal levels as European markets returned from extended Easter Holiday weekend.- A quick overview of Tuesday's trade: Eurodollar options saw much better call buying, primarily in 1- and 3Y midcurves -- buying insurance or fading the sell-off in underlying as futures priced in more aggressive rate hikes after StL Fed Bullard opened dialog on chance of 75bp hike at May 4 FOMC late Monday.

- Weighing on short end and contributing to inverted prices in Eurodollar Reds (EDM3-EDH4) through Blues (EDM5-EDH6) as rising recession concerns and/or ability of Fed to engineer a soft landing continues. Adding to the weaker tone (higher rates) IMF joined World bank opinion from late Monday: knock-on effect of Russia invasion reducing global growth/increase inflation forecasts.

- Similarities and differences for Treasury derivatives - Treasury futures traded weaker all day while curves reversed steeper profiles after the early IMF global growth downgrade, extended flatter in late trade (2s10s -6.05 at 33.79 in late trade compares to +42.89 early high -- this in itself quite a feat after the pare traded inverted low of -9.561 just two weeks ago. Treasury option volumes slipped in the current session vs. Monday with put structures drawing better interest.

- +7,500 SFRU2 96.87 puts, 3.25 vs. 97.86/0.05%

- Block, 5,000 SFRQ2 97.43/97.68 put spds, 6.5 vs. 97.89

- +5,000 Jun 97.87/98.00/98.12 put flys, 2.25

- +20,000 Blue Jun 98.00 calls, 1.5

- +5,000 Red Jun'23 95.62/96.37 put spds, 24.0

- +2,500 Red Dec'23 96.62 straddles, 140-141.5

- +5,000 short Jul 97.62/98.00 call spds, 1.5 ref 96.58

- +5,000 short Dec 97.37/97.62/98.00/98.25 call condors, 3.5 ref 96.68

- -1,000 short Dec 96.75 straddles, 89.5 vs. 91.0 Mon' settle

- 4,000 short Aug 97.87/98.37 call spds

- +4,000 Jul 97.62/97.75 put spds, 7.25

- Overnight trade

- 1,000 Sep 97.56/97.68/97.75/97.87 put condors

- 5,000 FVK 112.75/113 call spds, 13.5

- +2,000 TYN 121.5 calls, 35 ref 118-25.5

- -3,000 USM 132/136/138 2x2x1 put flys, 19

- +3,000 USM 132/136 put spds, 48

- +5,000 FVM 111.5/112.25/113 broken put flys, 6.5-7

- Overnight trade

- -2,000 TYM 119.5 straddles, 2-12 ref 119-15.5

- 4,000 TYK 119.75 calls, 17

- 3,000 TYM 122/122.5 call spds, 5

- 1,500 TYK 119.25/120 put spds

FOREX: JPY Continues Downward Trajectory, CNH Weakens To Six-Month Low

- USDJPY continues to defy gravity and maintains this week’s extension of its current uptrend, trading to a fresh cycle high, just below the 129.00 mark. The break higher has reinforced underlying bullish technical conditions and signals potential for a continuation of the bull cycle towards 129.44, a Fibonacci projection, and the psychological 130.00 handle.

- However, the trend condition is overbought and it should be noted that warnings from Japanese officials over the sharp depreciation have intensified.

- Fed rhetoric has kept upward pressure on US Treasury yields and dollar indices look set to extend their winning streak to four, gradually improving on last Thursday’s impressive advance.

- The Chinese yuan slipped to its weakest level in six months, pressured by additional concern surrounding China’s growth outlook. China’s central bank unveiled nearly two dozen measures and promises intended to boost lending and support industries that have been beaten down by recent Covid lockdowns, including a pledge to guide banks to expand loan extensions.

- Furthermore, amid this surge in U.S. yields, there was considerable pressure on emerging market currencies, with notable downswings in both ZAR (-2.15%) and MXN (-1.12%).

- Elsewhere in the G10 space, the Swiss Franc also came under pressure on Tuesday, with USDCHF breaking a significant horizontal resistance area, dating back to July 2020, around 0.9470. A clean break has seen the pair rise to highs of 0.9520 and consolidate these gains above the 0.95 handle. AUD was the clear outperformer with the late boost in equity indices underpinning the relative strength.

- A relatively quiet overnight data docket on Wednesday should place the focus on Canadian CPI, with US existing home sales and the Fed’s Beige Book headlining the US calendar.

FX: Expiries for Apr20 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.0790-11(E1.5bln), $1.0875(E588mln)

- AUD/USD: $0.7400-20(A$909mln)

- USD/CAD: C$1.2600-15($680mln)

EQUITIES: Late Equity Roundup: SPX Through 50-Day EMA Resistance

Stocks making late headway, SPX eminis through key resistance: ESM2 at 4462.0 +75.25, breach of 50-day EMA key resistance at 4446.83.

- Opens next key level of 4519.75/4588.75 (Apr 8/Apr 5 high) where a break would ease the bearish threat.

- Various drivers: early support appeared to be driven by better than expected earnings releases ahead the open from: JNJ, CFG, HAL, TFC, PLD, SI, LMT, SBNY (Hasbro and Fifth Third missing est). After the bell: Netflix and IBM.

- Desks also cite strong housing starts at 16Y high as not recessionary, weaker crude; no mask mandate helping airline shares.

- SPX leading/lagging sectors extending early gains: Consumer Discretionary (+2.94%) with durables and apparels outpacing autos, retailing and consumer services. Real Estate sector (+2.26%) outpacing Communication Services (+2.13%).

- Laggers: Energy sector (-0.73%) continues to underperform with oil/gas, consumable fuels underperforming with drop in crude (WTI -5.93 at 102.38)

- Meanwhile, Dow Industrials currently trades +527.49 (1.53%) at 34940.29, Nasdaq +298.4 (2.2%) at 13630.51.

- Dow Industrials Leaders/Laggers: Home Depot (HD) leads +6.42 at 306.63. Boeing (BA) +6.37 at 186.22 outpaces Goldman Sachs (GS) +6.11 at 335.99. Travelers Ins extends sell-off -9.58 at 175.64 despite beating earnings est, forward guidance in question.

E-MINI S&P (M2): Through 50-Day EMA Resistance Late

- RES 4: 4663.50 High Jan 18

- RES 3: 4631.00 High Mar 29 and a key resistance

- RES 2: 4519.75/4588.75 High Apr 8 / High Apr 5

- PRICE: 4465.00 @ 1530ET Apr 19

- RES 1: 4446.83 50-day EMA

- SUP 1: 4355.50 Low Apr 18

- SUP 2: 4321.07 61.8% retracement of the Mar 15 - Mar 29 rally

- SUP 3: 4247.89 76.4% retracement of the Mar 15 - Mar 29 rally

The S&P E-Minis short-term condition remains bearish. The contract recently traded through its 50-day EMA, which intersects at 4446.83, and this has reinforced the current bearish threat. The move below 4400.00 signals scope for weakness towards 4321.07 next, a Fibonacci retracement. Initial firm resistance has been established at 4519.75, Apr 8 high A break would ease the bearish threat.

COMMODITIES: WTI and Gold Both Test 20-day EMAs

- Oil prices have slid throughout most of the session as Fed hiking expectations bite and the IMF downgrades its global growth forecast, before only seeing a modest rise on the US eyeing up fresh Russian sanctions potentially this week.

- WTI is -5.0% at $102.8, having earlier nudged below the 20-day EMA of $102.62. A clear break would open the 50-day EMA at $98.67 whilst resistance remains yesterday’s high of $109.81.

- Unusually, today’s most active strikes in the M2 contract have been $90/bbl and $80/bbl calls.

- Brent is -5.0% at $107.5, having stopped just shy of the 20-day EMA of $106.63, which continues to form support.

- Gold is -1.3% at $1953.2 as Treasury yields surge and compete for safe haven demand. It earlier tested initial support at the 20-day EMA of $1951.6, a clear break of which could open the 50-day EMA of $1924.2. Resistance is yesterday’s high of $1998.4.

Wednesday Data Calendar

| Date | GMT/Local | Impact | Flag | Country | Event |

| 19/04/2022 | 0000/2000 |  | US | Minneapolis Fed's Neel Kashkari | |

| 20/04/2022 | 2350/0850 | ** |  | JP | Trade |

| 20/04/2022 | 0600/0800 | ** |  | DE | PPI |

| 20/04/2022 | 0845/0945 |  | UK | BOE Mutton Panelist on Central Bank Digital Currencies | |

| 20/04/2022 | 0900/1100 | ** |  | EU | industrial production |

| 20/04/2022 | 0900/1100 | * | | EU | Trade Balance |

| 20/04/2022 | 0900/1000 | ** | | UK | Gilt Outright Auction Result |

| 20/04/2022 | 1100/0700 | ** | | US | MBA Weekly Applications Index |

| 20/04/2022 | - | | EU | ECB Lagarde & Panetta in IMF/World Bank Meetings | |

| 20/04/2022 | - | | EU | ECB Lagarde & Panetta at G7 &G20 Finance Ministers' Meetings | |

| 20/04/2022 | 1230/0830 | *** |  | CA | CPI |

| 20/04/2022 | 1400/1000 | *** | | US | NAR existing home sales |

| 20/04/2022 | 1430/1030 | ** | | US | DOE weekly crude oil stocks |

| 20/04/2022 | 1430/1030 | | US | Chicago Fed's Charles Evans | |

| 20/04/2022 | 1430/1030 | | US | San Francisco Fed's Mary Daly | |

| 20/04/2022 | 1700/1300 | ** | | US | US Treasury Auction Result for 20 Year Bond |

| 20/04/2022 | 1700/1300 | | US | Atlanta Fed's Raphael Bostic | |

| 20/04/2022 | 1800/1400 | | US | FOMC Beige Book | |

| 21/04/2022 | 2245/1045 | *** |  | NZ | CPI inflation quarterly |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok