Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

US TSYS: Data-Driven Vol, Yields Higher, Stocks Extend Wk Lows

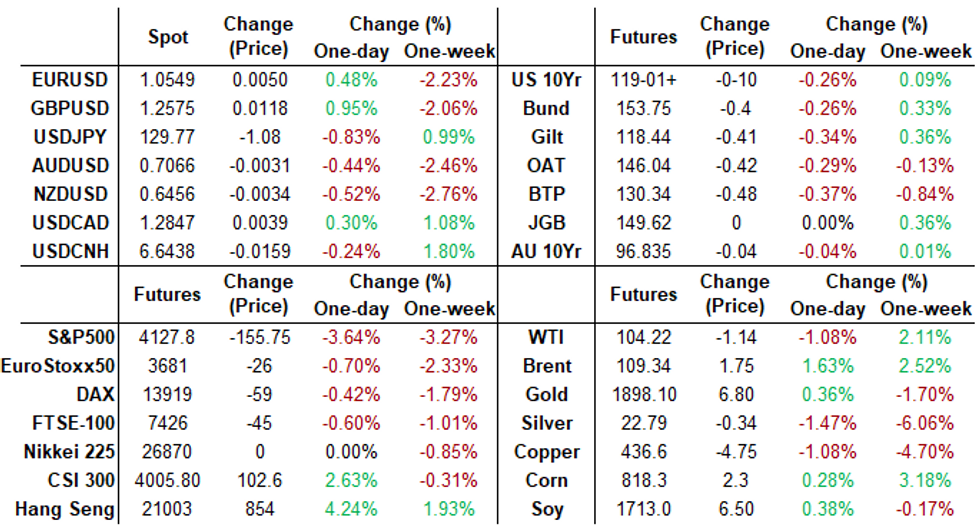

FI markets traded weaker after the bell, off early session lows amid data-driven vol in the first half. Quiet second half trade ensued even as equities fell back to late Tuesday levels (SPX -3.6% to 4128.0)- Rates trade weaker, curves bear flattening with short end underperforming (Block sale: -10,000 TUM2 105-10.88, sell through 105-11 post-time bid at 0841:030ET) after Personal Income: +0.5%/MoM vs. +0.4% est, Spending +1.1%MoM vs. +0.6% est, PCE Deflator in line at +0.9%, Employment Cost Index is +1.4% vs. 1.1% est.

- FI levels rebounded sharply after April Chicago Business Barometer™ fell to 56.4 vs. 62.0 est. Prices Paid ticked up a modest 0.4 points to 86.1 with over three-quarters of firms citing higher prices this month. The Ukraine war was cited as inflating steel, plastics and lumber costs.

- Data driven volatility evaporated by midday with rates hold to a relative narrow range, yield curves flatter but off lows (2s10s -1.116 at 18.994 vs. 13.399L; 5s30 -1.867 at -3.742 vs. -6.508L).

- Focus turns to next Wednesday's FOMC policy annc, 50bp expected, Tsy refunding early Wednesday as well.

- The 2-Yr yield is up 7.7bps at 2.6943%, 5-Yr is up 7.3bps at 2.9124%, 10-Yr is up 5.9bps at 2.8811%, and 30-Yr is up 4.9bps at 2.9413%.

SHORT TERM RATES

US DOLLAR LIBOR: Latest settlements

- O/N +0.00500 to 0.33000% (+0.00357/wk)

- 1M +0.00329 to 0.80329% (+0.09986/wk)

- 3M +0.04886 to 1.33486% (+0.12125/wk) ** Record Low 0.11413% on 9/12/21

- 6M +0.06257 to 1.91071% (+0.08700/wk)

- 12M +0.07943 to 2.54914% (+0.02186/wk)

STIR: FRBNY EFFR for prior session:

- Daily Effective Fed Funds Rate: 0.33% volume: $81B

- Daily Overnight Bank Funding Rate: 0.32% volume: $259B

US TSYS: Repo Reference Rates

- Secured Overnight Financing Rate (SOFR): 0.28%, $892B

- Broad General Collateral Rate (BGCR): 0.30%, $337B

- Tri-Party General Collateral Rate (TGCR): 0.30%, $327B

- (rate, volume levels reflect prior session)

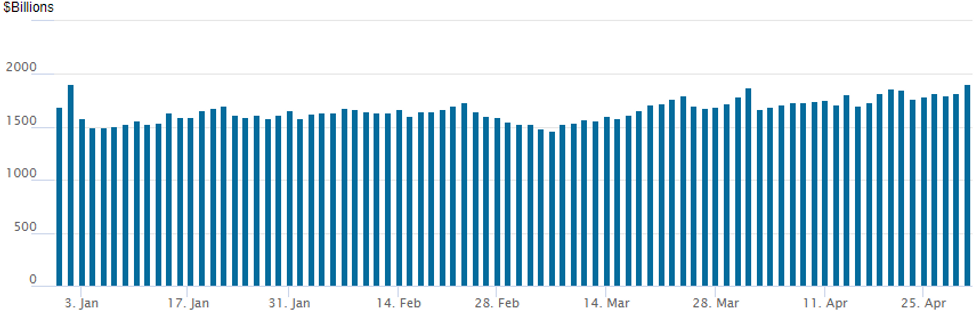

FED Reverse Repo Operation: New All-Time High

NY Federal Reserve/MNI

NY Fed reverse repo usage climbs to new all-time high of 1,906.802B w/ 92 counterparties from prior session 1,818.416B. Compares to prior all-time high of $1,904.582B on Friday, December 31.

EURODOLLAR/SOFR/TREASURY OPTIONS SUMMARY

Overall FI option volumes remained muted Friday while the theme of better put trade continued as underlying rate futures traded back near early week levels, curves flatter (but off lows) amid heavy selling in the short end.- Despite weaker economic data this week, STIR futures are pricing in 200Bp of rate hikes over the next four meetings.

- Not a lot of new put positions being created, late week trade more tied to repositioning strikes via condor sales, or profit taking/position squaring ahead the weekend.

- Block, 4,000 SFRK2 98.12/98.37 put spds 5.25

- Block, 10,000 Sep 99.50/Red Sep 95.00 2x1 put spds, 18.0 net

- Block, 10,000 Jun 98.00/98.12/98.25/98.37 put condors, 7.0

- 1,000 short May 96.25/96.37/96.37 put flys

- +2,000 short Jun 95.68/96.00/96.25 put flys

- +2,500 Dec 97.00/97.50/98.00 put trees, 20.0

- -5,000 Green May 96.31/96.56/96.81 put flys, 5.5

- Update, total -35,000 FVM 113.5/114 call spds, 8.5

- -7,700 USM 132/134/136/138 put condors, 21-17

- Overnight trade

- 3,000 FVM 111.5 puts

- 10,000 FVM 113.5/114 call spds

- +5,000 wk5 FV 112.5 puts, 4-4.5 ref 112-24.5

- +6,500 wk5 TY 119.25 puts, 14

EGB Options: Plenty Of Euribor Put Buying To CLose The Week

Friday's Europe rates / bond options flow included:

- RXN2 156.00/158.00 cs, bought for 66 in 5.4k

- 0RM2 98.25/97.75ps, bought for 5.75 in 2k (also traded yesterday in 8k)

- ERM2 100.125/100.00 put spread bought for 1.5 in 10k

- ERZ2 99.50/99.75/100p fly sold vs buying 99.62/99.37/99.12p fly, net half in 6k

- SFIK2 98.70/98.80, bought for 1 in 3k

FOREX: USD Trims Gains Following Stellar Wkly Performance, Cross/JPY Falters

- The greenback edged lower on Friday, falling against most major currencies as the recent healthy upward momentum stalled approaching the weekend close. The USD Index is 0.7% lower on the day, however, gains for the week remain close to 1.7% and it is important to note the DXY remains over 3% above last week’s low, highlighting the rapidity of the recent broad appreciation.

- Factors contributing to Friday’s USD weakness may have been potential month-end related flows as well as profit-taking dynamics ahead of the weekend.

- Notable strength was seen in both GBP and JPY, both rising over 1% against the greenback as the very sharp weekly declines were partially retraced. In similar vein, EURUSD traded with a much more supportive tone, unable to match yesterday’s lows of 1.0472 and now trading roughly 100 pips higher, approaching the close.

- AUD, NZD and CAD were the anomalies on the day, both residing in marginal negative territory on Friday against the dollar. Even more notable declines against the Japanese Yen is perhaps explained by the renewed weakness in US equity indices that have reversed the entirety of Thursday’s advance, as of writing.

- Final PMI readings on Monday feature on a light economic data calendar. US ISM Manufacturing PMI headlines the US docket. China and the UK are both out for local holidays.

- Heavy central bank week ahead with obvious focus on Wednesday’s Fed meeting. The RBA also meets on Tuesday ahead of the Bank of England on Thursday.

FX: Expiries for May02 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.0600(E684mln), $1.0700-15(E1.1bln), $1.0800(E1.6bln)

Late Equity Roundup: Nearing Lows For Wk, No Month-End Support Yet

About the time when things can get interesting: heading into last couple hours of month-end trade going into the weekend (not to mention more earnings next week, FOMC policy annc next Wednesday).

- SPX eminis continue to extend session lows: ESM2 -109.0 (-2.56%) at 4174.25, below Thursday low, but still off late Tue low around 4138.0. Week’s lows reinforced bearish conditions and confirmed a resumption of the bear cycle w/ initial key support for SPX at 4136.75 Low Apr 26; next key support level at 4129.50 Low Mar 15.

- Month-end factor: In the off chance of a reversal, initial resistance defined at 4303.50, Apr 26/28 high. A break of this hurdle would signal scope for a stronger corrective bounce and expose 4355.50, the Apr 18 low.

- SPX leading/lagging sectors: Materials (-0.76%), Industrials (-1.49%) and Consumer Staples (-1.69%) underperforming the least at the moment.

- Laggers: Consumer Discretionary (-5.34%) weighed down by weaker Amazon (AMZN, -14.23%), ETSY (-6.27%) and Expedia (-4.24%), buffered slightly by Autos (+0.55%) w/ Tesla leads +1.17%.

- Meanwhile, Dow Industrials currently trades -582.67 points (-1.72%) at 33339.52, Nasdaq -384.5 points (-3%) at 12488.29.

- Dow Industrials Leaders/Laggers: Honeywell (+6.71), Merck (+0.18). United Health Care leading laggers (-9.65).

- RES 4: 4631.00 High Mar 29 and key resistance

- RES 3: 4588.75 High Apr 5

- RES 2: 4509.00 High Apr 21 and a key short-term resistance

- RES 1: 4303.50/4355.50 High Apr 26/28 / Low Apr 18

- PRICE: 4152.50 @ 1517ET Apr 29

- SUP 1: 4136.75 Low Apr 26

- SUP 2: 4129.50 Low Mar 15 and a key support

- SUP 3: 4094.25 Low Feb 24 and a bear trigger

- SUP 4: 4063.24 1.618 proj of the Mar 29 - Apr 18 - 21 price swing

S&P E-Minis remain in a downtrend despite the recent recovery from 4136.75, Apr 26 low. This week’s lows reinforced bearish conditions and confirmed a resumption of the bear cycle. This has opened 4129.50, the Mar 15 low. Initial resistance has been defined at 4303.50, Apr 26/28 high. A break of this hurdle would signal scope for a stronger corrective bounce and expose 4355.50, the Apr 18 low.

COMMODITIES: Oil Ends Week Higher With EU Russia Embargo Eyed

- Major oil benchmarks are ending the week on a soft note as they slid into WTI settlement.

- Both look to end the week up circa 2.5% with the main move being Germany giving the green light to the EU embargo of Russia oil plus China demand fears pulling back slightly with some improvement in Covid-cases.

- WTI is -0.6% at $104.72. It earlier cleared triangle resistance drawn from the Mar 15 low of $106.78, next opening $109.2 (Apr 18 high).

- Brent is -0.1% at $107.09, also having cleared initial resistance at $109.8 (Apr 21 high) which opens triangle resistance at $112.08.

- Gold is +0.9% at $1911.48 as today’s slide in the USD helps recover some of the week’s loss from a stronger dollar and rising yields. Initial resistance is eyed at $1932.1 (20-day EMA) with support at $1872.2 (Apr 28 low).

- Week returns: WTI +2.6%, Brent +2.6%, Gold -1.1%, TTF gas +2.7% (in euros).

Monday Data Calendar

| Date | GMT/Local | Impact | Flag | Country | Event |

| 02/05/2022 | 0030/0930 | ** |  | JP | IHS Markit Final Japan Manufacturing PMI |

| 02/05/2022 | 0600/0800 | ** |  | DE | retail sales |

| 02/05/2022 | 0715/0915 | ** |  | ES | IHS Markit Manufacturing PMI (f) |

| 02/05/2022 | 0745/0945 | ** |  | IT | IHS Markit Manufacturing PMI (f) |

| 02/05/2022 | 0750/0950 | ** |  | FR | IHS Markit Manufacturing PMI (f) |

| 02/05/2022 | 0755/0955 | ** | | DE | IHS Markit Manufacturing PMI (f) |

| 02/05/2022 | 0800/1000 | ** |  | EU | IHS Markit Manufacturing PMI (f) |

| 02/05/2022 | 0900/1100 | ** | | EU | Economic Sentiment Indicator |

| 02/05/2022 | 0900/1100 | * | | EU | Business Climate Indicator |

| 02/05/2022 | 0900/1100 | * | | EU | Consumer Confidence, Industrial Sentiment |

| 02/05/2022 | 1345/0945 | *** |  | US | IHS Markit Manufacturing Index (final) |

| 02/05/2022 | 1400/1000 | *** | | US | ISM Manufacturing Index |

| 02/05/2022 | 1400/1000 | * | | US | Construction Spending |

| 02/05/2022 | 1530/1130 | * | | US | US Treasury Auction Result for 13 Week Bill |

| 02/05/2022 | 1530/1130 | * | | US | US Treasury Auction Result for 26 Week Bill |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.