Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

US TSYS: Relief Rally After Fed 50Bp Hike, June QT

Fed hiked rates 50bp Wednesday, the most in 22 years, while leaving the door open for additional 50bp moves over the next few meetings to address surging inflation.The Fed also penciled in June for start of balance sheet drawdown or quantitative tightening. Risk-on after less hawkish forward guidance

- Stocks staged a strong rally after Fed Chairman Powell poured cold water on chances of 75bp hike in the near term, while yield curves re-steepened off lows (2s10s finished at 28.653 after topping 30.0 briefly, compared to early session low of 13.987) as short end rates adjusted higher.

- Earlier session action: Brief two-way trade after April ADP private employ data +247k vs. +385k est, FI trading weaker into the NY open -- bounces after quarterly US Tsy refunding annc.

- Tsy plans to continue reducing auction sizes of coupons during the May-July quarter, but by smaller increments than in previous quarters, and left open the door for additional cuts in future quarters if needed.

- The U.S. Treasury Wednesday said it plans to continue reducing auction sizes of coupons during the May-July quarter, but by smaller increments than in previous quarters, and left open the door for additional cuts in future quarters if needed.

- The department will issue USD103 billion of securities at next week's quarterly refunding, raising USD55.2 billion in new cash. Officials say they plan to sell USD45 billion in 3-year notes on May 10, USD36 billion in 10-year notes on May 11, and USD22 billion in 30-year bonds on May 12.

SHORT TERM RATES

US DOLLAR LIBOR: Latest settlements

- O/N +0.00000 to 0.33029% (+0.00029/wk)

- 1M +0.01343 to 0.84514% (+0.04185/wk)

- 3M +0.04285 to 1.40614% (+0.07128/wk) ** Record Low 0.11413% on 9/12/21

- 6M +0.03871 to 2.01957% (+0.10886/wk)

- 12M +0.05357 to 2.74843% (+0.11986/wk)

STIR: FRBNY EFFR for prior session:

- Daily Effective Fed Funds Rate: 0.33% volume: $79B

- Daily Overnight Bank Funding Rate: 0.32% volume: $260B

US TSYS: Repo Reference Rates

- Secured Overnight Financing Rate (SOFR): 0.30%, $923B

- Broad General Collateral Rate (BGCR): 0.30%, $354B

- Tri-Party General Collateral Rate (TGCR): 0.30%, $343B

- (rate, volume levels reflect prior session)

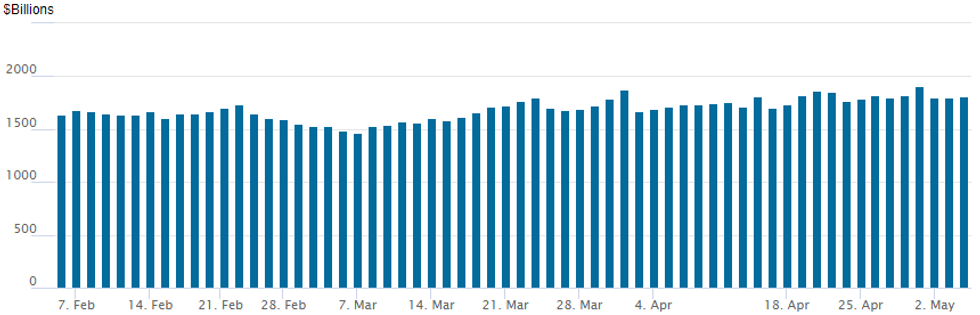

FED Reverse Repo Operation

NY Federal Reserve/MNI

NY Fed reverse repo usage at 1,815.656B w/ 87 counterparties vs. prior session's 1,796.252B (all-time high of $1,906.802B on Friday, March 29, 2022).

EURODOLLAR/SOFR/TREASURY OPTIONS SUMMARY

Short end rates rallied as Fed Chairman Powell ruled out 75bps hikes to address burgeoning inflation, yield curves bull steepened (2s10s +10.358 to 28.830 vs. 13.987 low in the first half!) as a result. Equities liked the less hawkish messaging as well, SPX emini futures ESM2 +130.0 in late trade nearing 4300.- Addressing question over "plausible soft landing" through judicious monetary policy: months of inversion at the front end of Reds (low measure of confidence in forward policy and/or Fed managing a soft landing/avoiding recession) is gradually off lows:

- Red Sep (EDU3) currently trading 96.44 vs. Red Jun (EDM3) at 96.52, -0.080 vs. -0.11 this morning. Levels start to flatten out (dis-invert) around late Blue Dec'25/Mar'26 around 96.985.

- Eurodollar option highlights segued from large put position unwinds well ahead of the FOMC, followed by large upside call buying in late trade.

- Block, 5,000 Aug 97.12/97.37/97.43/97.68 put condors, 5.5

- Block, 4,000 Aug 97.93/98.06/98.12/98.25 call condors, 1.5 adds to 10k Block late Tue at 1.25 with open interest rising to 49k in each strike

- Block, +25,000 Dec 97.00 calls, 29.0

- +20,000 Blue Jun 97.75 calls, 1.5 still offered, ref 96.865

- Block, 60,000 Sep 97.50/97.75 put spds, 18.5, hear unwind/taking profit

- Block, 25,000 Sep 96.62/97.12/97.37 broken put flys, 1.0 cr

- Block, 40,000 Sep 96.75/97.00/97.25/97.50 put condors, 8.5 ref 97.15

- +5,000 Sep 96.75/97.00/97.25/97.50 put condors, 8.0-8.25

- Overnight trade

- 45,000 Jun 98.06/98.18 call spds

- 4,800 Sep 97.25/98.06 call spds

- 7,700 Jun 98.00/98.12 call spds

- 3,000 Green Jun 97.00 calls, 8.0 ref 96.65

- 6,000 TYM 118.5 calls, 48 ref 118-10

- +10,000 FVM 112.25 calls, 35 vs. 112-06

- 3,000 USM 132/134/136/138 put condors ongoing strike roll-down adds to -5k on Monday

- +10,500 TYM 118.5 calls, 52 vs 118-14

- 3,500 TYM2 131/132.5 call spds

- Overnight trade

- Block, 4,721 wk1 TY 119.75 calls, 4

- 10,000 wk1 TY 116.5/117 put spds

- 2,480 TYM 117.25/118.25 2x1 put spds

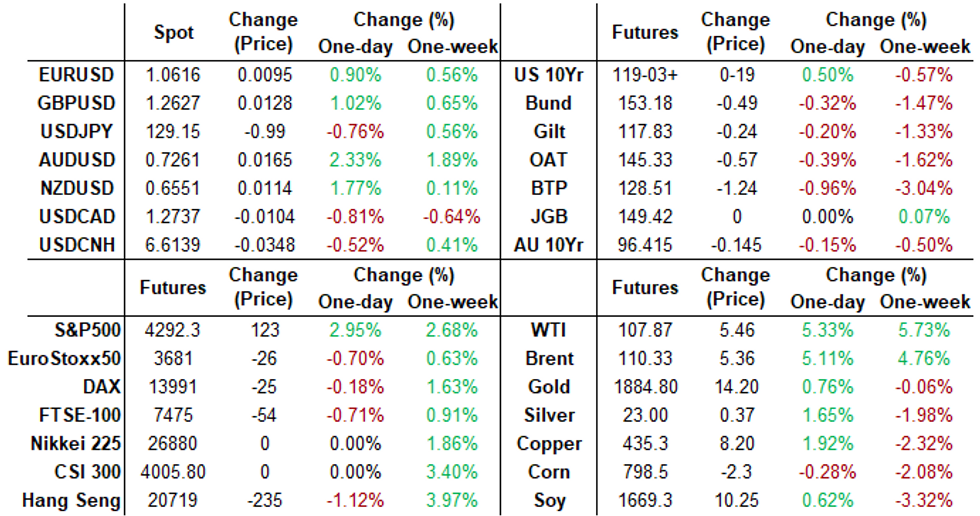

FOREX: Powell Rules Out 75BP Hike Consideration, Greenback Falters

- After some initial two-way price action for the greenback following the FOMC decision and early comments from Chair Powell, the US Dollar came under significant pressure with Dollar Indices retreating close to 1.0%.

- The comment that 50bp hikes "should be on the table at the next couple of meetings" and then dismissing any consideration of a 75bp increase particularly weighed on USD with price action extending throughout the press conference.

- The likes of EURUSD and USDJPY moved in line with this greenback weakness with the former rising back above the 1.06 handle to reach 1.0626 and the latter crashing back below 129.00.

- However, the key outperformers on Wednesday following the decision were Antipodean currencies and in particular the Australian dollar. AUDUSD has rallied close to 2%, benefitting from rallying equities as well as yesterday’s hawkish domestic monetary policy developments.

- Despite the sharp pullback, bearish conditions still dominate the technical outlook which puts particular significance of the nearest resistance points of at 0.7261, Apr 5 high and then firmer resistance at 0.7301, the 50-day EMA.

- USD weakness remained fairly broad based with CHF and CNH relative underperformers, only rising between 0.35-0.4%.

- With a fairly light global economic data calendar on Thursday, focus will be on the Bank of England meeting/decision where markets are expecting a 25bp rate increase by the MPC to 1.00%. The MNI Preview can be found here: https://marketnews.com/markets/central-bank-reports/central-bank-preview/bank-of-england-preview/mni-boe-preview-may-2022-25bp-now-what-next

FX: Expiries for May05 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.0500-10(E1.2bln), $1.0565-85(E995mln), $1.0600(E1.7bln), $1.0750-65(E1.6bln), $1.0800(E1.5bln)

- GBPUSD: $1.2550(Gbp502mln), $1.2900(Gbp1.2bln)

- EUR/GBP: Gbp0.8600(E952mln)

- USD/JPY: Y127.50($685mln)

- EUR/JPY: Y135.00(E523mln)

- AUD/USD: $0.7135-50(A$571mln)

- USD/CAD: C$1.2865-80($869mln), C$1.2890-05($689mln), C$1.3075($1.2bln), C$1.3100($1.8bln)

Late Stock Roundup, Strong Post-FOMC Rally

Stocks staged a strong rally after Fed Chairman Powell poured cold water on chances of 75bp hike in the near term to address surging inflation, equity indexes trading at/near late session highs.

- SPX emini futures ESM2 currently +119.5 points (2.87%) at 4289.75 -- with attention on key resistance of 4303.50/4355.50 High Apr 26/28 / Low Apr 18.

- Large earnings on tap after the bell: Allstate (ALL), GoDaddy (GDDY), MetLife (MET), Ebay, ETSY.

- SPX leading/lagging sectors: Energy sector remains strong (+3.86) as O&G shares outperform energy equipment and servicers. Communication Services (+3.59%) and Information Technology (+3.27%) outperforming late.

- Laggers: Real Estate sector continues to underperform (+0.91%), followed by Consumer Staples (+2.14%) and Utilities (+2.17%).

- Meanwhile, Dow Industrials currently trades +886.99 points (2.68%) at 34022.19, Nasdaq +374.9 points (3%) at 12939.27.

- RES 4: 4631.00 High Mar 29 and key resistance

- RES 3: 4588.75 High Apr 5

- RES 2: 4509.00 High Apr 21 and a key short-term resistance

- RES 1: 4303.50/4355.50 High Apr 26/28 / Low Apr 18

- PRICE: 4283.50 @ 1545ET May 4

- SUP 1: 4056.00 Low May 2

- SUP 2: 4029.25 High May 13 2021

- SUP 3: 4000.00 Psychological round number

- SUP 4: 3958.00 2.00 proj of the Mar 29 - Apr 18 - 21 price swing

S&P E-Minis remain in a downtrend, despite the recovery from Monday’s low. Fresh cycle lows continue to reinforce underlying bearish conditions and Monday’s move lower resulted in a probe of key support at 4094.25, the Feb 25 low. A clear break of this level would reinforce bearish conditions and open the 4000.00 handle. 4056.00, Monday’s low, has also been defined as an important bear trigger. Firm short-term resistance is at 4303.5.

E-MINI S&P (M2): Trend Needle Still Points South

- RES 4: 4631.00 High Mar 29 and key resistance

- RES 3: 4588.75 High Apr 5

- RES 2: 4509.00 High Apr 21 and a key short-term resistance

- RES 1: 4303.50/4355.50 High Apr 26/28 / Low Apr 18

- PRICE: 4155.00 @ 1600 BST May 4

- SUP 1: 4056.00 Low May 2

- SUP 2: 4029.25 High May 13 2021

- SUP 3: 4000.00 Psychological round number

- SUP 4: 3958.00 2.00 proj of the Mar 29 - Apr 18 - 21 price swing

S&P E-Minis remain in a downtrend, despite the recovery from Monday’s low. Fresh cycle lows continue to reinforce underlying bearish conditions and Monday’s move lower resulted in a probe of key support at 4094.25, the Feb 25 low. A clear break of this level would reinforce bearish conditions and open the 4000.00 handle. 4056.00, Monday’s low, has also been defined as an important bear trigger. Firm short-term resistance is at 4303.5.

COMMODITIES: Oil Jumps As EU Eyes Stricter Russia Ban

- Oil prices have increased sharply today as the EU moves to a complete ban of Russian crude and refined oil by the end of this year, with no gradual phase out.

- Separately on diesel, East Coast inventories fell to a record low as US refiners increasingly supply global markets.

- WTI is +5.4% at $107.91, having briefly cleared resistance at the Apr 29 high of 107.99 which next opens $109.2 (Apr 18 high).

- The most active strikes in the M2 contract have been $130/bbl calls.

- Brent is +5.1% at $110.30, having earlier cleared resistance at 110 (Apr 29 high) but not the triangle resistance at $112.00.

- Gold is +0.9% at $1884.5, moving higher through the FOMC presser as Chair Powell pushed back on 75bps with a focus on moving in 50bp clips at coming meetings. It moves closer to initial resistance at $1900.0 (May 2 high) whilst support is at $1854.7 (May 2 low).

Thursday Data Calendar

| Date | GMT/Local | Impact | Flag | Country | Event |

| 05/05/2022 | 0130/1130 | * |  | AU | Building Approvals |

| 05/05/2022 | 0130/1130 | ** | | AU | Trade Balance |

| 05/05/2022 | 0145/0945 | ** |  | CN | IHS Markit Final China Services PMI |

| 05/05/2022 | 0600/0800 | ** |  | DE | manufacturing orders |

| 05/05/2022 | 0630/0830 | *** |  | CH | CPI |

| 05/05/2022 | 0645/0845 | * |  | FR | industrial production |

| 05/05/2022 | 0700/0300 | * |  | TR | Turkey CPI |

| 05/05/2022 | 0730/0930 | ** |  | EU | IHS Markit Final Eurozone Construction PMI |

| 05/05/2022 | 0800/1000 | *** |  | NO | Norges Bank Rate Decision |

| 05/05/2022 | 0830/0930 | ** |  | UK | IHS Markit/CIPS Services PMI (Final) |

| 05/05/2022 | 1000/1200 | | EU | ECB Lane Speech on Euro Area Outlook | |

| 05/05/2022 | 1100/1200 | *** | | UK | Bank Of England Interest Rate |

| 05/05/2022 | 1130/1230 | | UK | BOE post-MPC press conference | |

| 05/05/2022 | 1230/0830 | ** |  | US | Jobless Claims |

| 05/05/2022 | 1230/0830 | ** | | US | Preliminary Non-Farm Productivity |

| 05/05/2022 | 1230/0830 | ** | | US | WASDE Weekly Import/Export |

| 05/05/2022 | 1300/1400 | | UK | Bank of England DMP Survey | |

| 05/05/2022 | 1340/0940 |  | CA | BOC Deputy Schembri speech to Indigenous group. | |

| 05/05/2022 | 1430/1030 | ** | | US | Natural Gas Stocks |

| 05/05/2022 | 1530/1130 | * | | US | US Bill 08 Week Treasury Auction Result |

| 05/05/2022 | 1530/1130 | ** | | US | US Bill 04 Week Treasury Auction Result |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.