Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

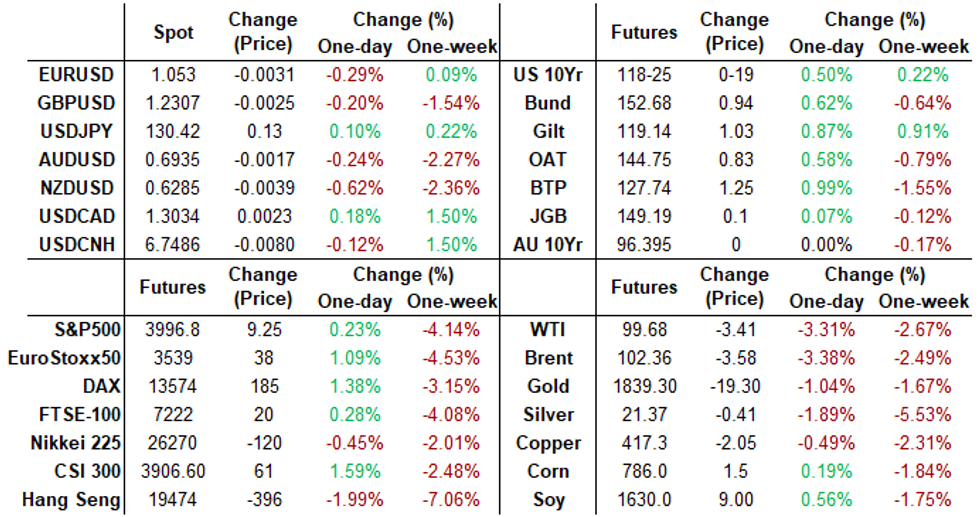

US TSYS: Expeditious Policy and Normal Fed Funds Rates

Rates trade firmer after the bell, Bonds off midday highs to near midmorning levels while yield curves hold flatter profiles as latest round of Fed speak anchors the front end.

- “I expect the FOMC will move expeditiously in bringing the federal funds rate back to more normal levels this year,” New York Fed President John Williams said Tuesday in prepared remarks to the Bundesbank. “Our monetary policy actions will cool the demand side of the equation.”

- Cleveland Fed Mester said 50bp rate increase base case "makes sense" over the next couple meetings. Richmond Fed Barkin said US doesn't "need a recession to contain inflation", adds Fed can reassess once rates are "into range of neutral".

- Treasury futures gradually receded off highs after $45B 3Y note auction (91282CEQ0) trades through: 2.809% high yield vs. 2.812% WI; 2.59x bid-to-cover vs. 2.48x last month.

- Focus turns to Wed' CPI data for April: MoM (1.2%, 0.2%; YoY (8.5%, 8.1%); CPI Ex Food and Energy MoM (0.3%, 0.4%); YoY (6.5%, 6.0%). Next leg Treasury supply: $36B 10Y note auction.

SHORT TERM RATES

US DOLLAR LIBOR: Latest settlements

- O/N -0.00129 to 0.82371% (+0.00514/wk)

- 1M -0.00129 to 0.84314% (+0.00100/wk)

- 3M +0.00129 to 1.39986% (-0.00200/wk) * / **

- 6M -0.04814 to 1.93200% (-0.03257/wk)

- 12M -0.08657 to 2.58829% (-0.10642/wk)

- * Record Low 0.11413% on 9/12/21; ** 2Y high 1.40614% on 5/4/22

STIR: FRBNY EFFR for prior session:

- Daily Effective Fed Funds Rate: 0.83% volume: $75B

- Daily Overnight Bank Funding Rate: 0.82% volume: $270B

US TSYS: Repo Reference Rates

- Secured Overnight Financing Rate (SOFR): 0.78%, $931B

- Broad General Collateral Rate (BGCR): 0.80%, $354B

- Tri-Party General Collateral Rate (TGCR): 0.80%, $343B

- (rate, volume levels reflect prior session)

FED Reverse Repo Operation

NY Federal Reserve/MNI

NY Fed reverse repo usage at 1,864.225B w/ 87 counterparties vs. prior session's 1,858.995B (all-time high of $1,906.802B on Friday, March 29, 2022).

EURODOLLAR/SOFR/TREASURY OPTIONS SUMMARY

Tuesday's FI option trade was a mixed bag of two-way Eurodollar calls, SOFR and 5Y call buyers while put buyers hedging higher yields in 5s were reported.

Highlight Eurodollar option trade included a Block sale of 50,000 December 97.00 calls at 0.5 followed by limited upside hedge via 15,000 Dec 99.37/99.50/99.87 call flys. Salient SOFR option Block included a purchase of 30,000 SFRH3 98.25 calls at 13.0.

Notable Treasury options centered on 5s with paper buying over 30,000 FVM 114 calls at 5.5, while paper bought 10,000 FVM 110.5/111.5/112/112.5 put condors at 5.5 in the second half.

- +5,000 SFRK2 98.25/98.37 put spds, 0.5

- Block, 30,000 SFRH3 98.25 calls, 13.0 vs. 97.02/0.16%

- +5,000 short Jun 96.25/96.50 put spds, 7.5 vs. 96.625/0.16%

- +15,000 Dec 99.37/99.50/99.87 call flys, 0.5

- Block, -50,000 Dec 97.00 calls, 34.0

- Block 48,500 Green Dec 97.37/97.62 strangles, 86.0-87.0

- Overnight trade

- 5,000 Jul 97.25/97.50 call spds

- Block, 7,500 Jun 97.00/97.25 put spds, 4.25

- 4,800 short May 96.00/96.12/96.37/96.50 put condors

- 3,000 short Aug 97.37/97.62 2x3 call spds

- 2,000 Mar 96.37/96.75 put spds

- +10,000 FVM 110.5/111.5/112/112.5 put condors, 5.5

- Update +30,000 FVM 114 calls, 5.5,

- 9,800 FVM 114.5/114.75 call spds

- 18,000 FVM 114 calls, 4, current bid

- -15,000 TYM 119.5 calls, 30

- 1,500 TYN 115.5/117 put spds

- 1,000 TYM 120.25/120.75/121.25 call flys

- Overnight data

- 2,250 USN 126/130/134 put flys, 48

- +3,500 TYM 117.5/117.75 put spds, 5 vs. 118-16

- +2,000 TYM 115.5/116/117 broken put flys, 12-13

EGBs-GILTS CASH CLOSE: BTPs Gain As Risk Appetite Stabilises

Core bond yields continued to fall Tuesday but closed a bit off session lows. The UK and German curves bull flattened, but BTPs led the charge, with 10Y yields falling as much as 21bp as risk appetite stabilised following Monday's broader market rout.

- Bundesbank chief Nagel said he supported a July rate hike, while saying he was skeptical of addressing eurozone fragmentation with a new tool.

- Periphery EGBs did little on those typically hawkish Nagel comments, with 10Y BTP spreads having already bounced higher from session lows below 200bp.

Closing Yields / 10-Yr Periphery EGB Spreads To Germany:

- Germany: The 2-Yr yield is down 6.4bps at 0.165%, 5-Yr is down 7.7bps at 0.691%, 10-Yr is down 9.3bps at 1.002%, and 30-Yr is down 9.2bps at 1.142%.

- UK: The 2-Yr yield is down 6.4bps at 1.329%, 5-Yr is down 9.5bps at 1.484%, 10-Yr is down 10.8bps at 1.848%, and 30-Yr is down 10.3bps at 2.056%.

- Italian BTP spread down 5.5bps at 200bps / Greek down 2.4bps at 250.8bps

EGB Options: Vol Buying, Bund Put Selling

Tuesday's Europe rates / bond options flow included:

- RXM2 152.50/151.00ps, sold at 63 in 4k (ref 152.29)

- RXM2 154.5/152.5/150.5p fly 2x3x1, sold at 83.5/83 in 1.5k

- DUM2 110.50/110.80/111.10c fly, sold at 3.25 in 2k

- DUN2 109.60/109.20ps vs 110.20c, bought the ps for 2 and 2.5 in ~6.3k

- 0RU2 98.25/98.00/97.87 broken p fly, bought for 6 in 5k

- ERU2 99.75 c fly, bought for 2.25 in 8k

- ERU2 99.75^, bought for 25 in 4k

- SFIK2 98.65c, bought for 2.75 in 2k

FOREX: USD, JPY Hold Recent Strength as Equities Show at a New Low

- Risk aversion remained the theme for currency markets Tuesday, with another downtick in equity markets resulting in a fresh low print for the e-mini S&P. This helped both the JPY and greenback hold recent strength, leaving the two currencies close to the top of the G10 table.

- SEK was the strongest, however, with markets watching comments from Riksbank's Ingves, who stated that a 'systematically' weaker SEK would be undesirable from a policy perspective. EUR/SEK reversed off a multi-month high printed in overnight trade at 10.6793.

- Gold also sold off alongside energy products, putting commodity-tied currencies at a disadvantage and resulting in AUD, NZD and CAD undperforming most others.

- Chinese inflation data crosses during the Wednesday Asia-Pac session, with markets expecting CPI to creep higher to touch 1.8%, while PPI moderates to 7.8%. US CPI then takes focus.

- Consensus has core inflation firming to +0.4% M/M from the +0.32% M/M in March, driven by a smaller decline or possibly a rise in used autos after sliding nearly 4%. Meanwhile headline is seen weaker at +0.2% M/M as large declines in gasoline weigh on energy whilst food inflation maintains its recent strong pace.

- Outside of macro data, a slew of ECB speakers are due throughout the day, with the highlights including Lagarde, Nagel, Makhlouf, Schnabel and Knot among many others.

FX: Expiries for May11 NY cut 1000ET (Source DTCC)

- USD/CAD: C$1.2765($1.2bln), C$1.2950($1.9bln), C$1.3000($1.4bln)

EQUITIES

E-MINI S&P (M2): Outlook Remains Bearish

- RES 4: 4588.75 High Apr 5

- RES 3: 4509.00 High Apr 21 and a key short-term resistance

- RES 2: 4342.20 50-day EMA

- RES 1: 4099.00/4303.50 High May 9 / High Apr 26/28

- PRICE: 4035.0 @ 1400ET May 10

- SUP 1: 3961.75 Intraday low

- SUP 2: 3958.00 2.00 proj of the Mar 29 - Apr 18 - 21 price swing

- SUP 3: 3892.98 2.23 proj of the Mar 29 - Apr 18 - 21 price swing

- SUP 4: 3843.25 Low Mar 25 2021 (cont)

S&P E-Minis remain vulnerable following last week’s sharp reversal from 4303.00, the May 4 high. Monday’s move lower resulted in a breach of support at 4056.00, the May 2 low. A clear break of this support confirms a resumption of the underlying downtrend and opens 3958.00 next, a Fibonacci projection. On the upside, key resistance has been defined at 4303.50, the Apr 26/28 high.

COMMODITIES: Crude Oil Eyes Next Key Near-Term Support Levels

- Oil prices slide further on continued growth fears although a worsening supply squeeze pushing US natural gas prices to a 14-year high.

- WTI is -2.9% at $100.07 having cleared initial support at $100.28 (May 2 low) which opens key near-term support at $95.28 (Apr 25 low).

- Puts replace calls as most active strikes today for the CLM2 contract, with $100/bbl followed by $95/bbl.

- Brent is -3.0% at $102.77, also through support at $103.1 (May 2 low) and opening key near-term support at $99.25 (Apr 25 low).

- Demonstrating the range to today’s moves, the most active strikes in the CLM2 contract have been $120/bbl calls followed by $105/bbl calls.

- Brent is -5.8% at $105.93, also through the 20-day EMA at $107.13, opening $103.1 (May 2 low).

- Gold sits -0.7% at $1841.87, just off session lows and the lowest print since February having erased the entire move higher since the Russian invasion of Ukraine. The 200-dma undercuts as support here ($1836.7) but weakness below that level opens $1828.42, the 76.4% retracement of the Dec - Mar rally.

Wednesday Data Calendar

| Date | GMT/Local | Impact | Flag | Country | Event |

| 11/05/2022 | 0030/1030 |  | AU | Westpac-MI Consumer Sentiment | |

| 11/05/2022 | 0600/0800 | *** |  | DE | HICP (f) |

| 11/05/2022 | 0600/0800 |  | EU | ECB Elderson Fireside Chat with Sonja Gibbs | |

| 11/05/2022 | 0800/1000 | | EU | ECB Lagarde Speech at 30th anniversary of Banka Slovenije | |

| 11/05/2022 | 0900/1000 | ** |  | UK | Gilt Outright Auction Result |

| 11/05/2022 | 1100/0700 | ** |  | US | MBA Weekly Applications Index |

| 11/05/2022 | 1220/1420 | | EU | ECB Schnabel Keynote Speech at Austrian National Bank | |

| 11/05/2022 | 1230/0830 | *** | | US | CPI |

| 11/05/2022 | 1430/1030 | ** | | US | DOE weekly crude oil stocks |

| 11/05/2022 | 1600/1200 | | US | Atlanta Fed's Raphael Bostic | |

| 11/05/2022 | 1700/1300 | ** | | US | US Note 10 Year Treasury Auction Result |

| 11/05/2022 | 1800/1400 | ** | | US | Treasury Budget |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.