Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

US TSYS: How Long Will Inflation Last?

FI futures trade firmer after the bell, off midday highs on moderate volumes (TYM2 just over 1M), yield curves flatter on narrow range (2s10s -2.58 at 30.65) with short end lagging despite several block buy in 5s on the session.- No obvious headline trigger, Tsys broke upside range soon after the equity open. Little react to morning data (NY Empire mfg index -11.6, new orders -8.8) with two-way trade/inside range by midmorning.

- Nothing really new from NY Fed Williams espousing 50bp hikes next couple meetings, comment "WE DON'T KNOW EXACTLY HOW LONG INFLATION WILL STAY HIGH" not exactly confidence inspiring.

- MNI exclusive w/ Loretta Mester: "With inflation as high as it is, and with expectations for inflation above 2%, you need to take into account that -- at least on the short end -- we’re still at an accommodative stance of policy. And even if we get up to 2.5%, depending on what’s happening on the inflation and expected inflation, we may still be accommodative," she said in an interview.

- Fed speakers resume Tuesday: Bullard, Harker, Kashkari, Mester, Evans through the session, Chairman Powell headlining at 1400ET.

- Deal-tied flow in the mix Monday with just under $10B swappable corporate issuance lead by $3B Paypal 4pt on the day. Gradual start to Jun/Sep Tsy futures rolling kicked off while June option expiration this Friday also added to volume trade.

SHORT TERM RATES

US DOLLAR LIBOR: Latest settlements

- O/N -0.00342 to 0.82229% (+0.00714 total last wk)

- 1M +0.04886 to 0.93557% (+0.04457 last wk)

- 3M +0.01129 to 1.45500% (+0.04185 last wk) * / **

- 6M +0.02200 to 2.01700% (+0.03043 last wk)

- 12M +0.00472 to 2.65686% (-0.04257 last wk)

- * Record Low 0.11413% on 9/12/21; ** New 2Y high: 1.45500% on 5/16/22

STIR: FRBNY EFFR for prior session:

- Daily Effective Fed Funds Rate: 0.83% volume: $84B

- Daily Overnight Bank Funding Rate: 0.82% volume: $266B

US TSYS: Repo Reference Rates

- Secured Overnight Financing Rate (SOFR): 0.79%, $917B

- Broad General Collateral Rate (BGCR): 0.80%, $356B

- Tri-Party General Collateral Rate (TGCR): 0.80%, $341B

- (rate, volume levels reflect prior session)

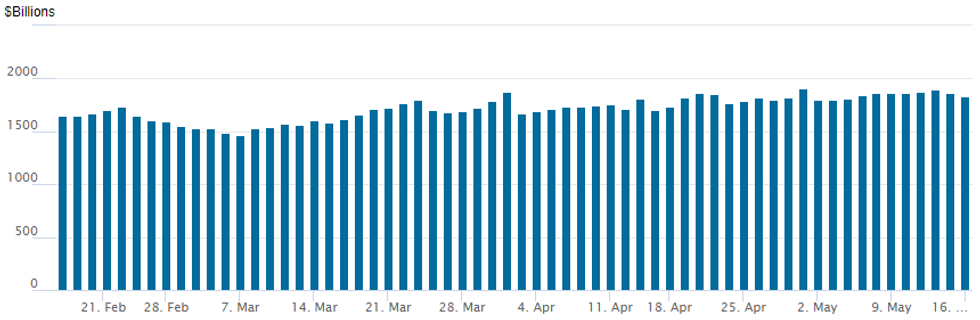

FED Reverse Repo Operation

NY Federal Reserve/MNI

NY Fed reverse repo usage currently 1,833.152B w/ 92 counterparties vs. prior session's 1,865.287B (all-time high of $1,906.802B on Friday, March 29, 2022).

EURODOLLAR/SOFR/TREASURY OPTIONS SUMMARY

Despite the rebound in FI futures Monday, listed option trade continued to favor downside/rate hike insurance buying via puts across the curve. Underlying driver: the Federal Reserve likely needs to move monetary policy to a restrictive stance to contain inflation, Cleveland Fed President Loretta Mester told MNI Monday, warning that the Fed's estimate of the nominal longer run fed funds rate of 2% to 3% might still leave policy too accommodative.

SOFR Options:

Total 11,000 SFRQ2 97.25/97.43/97.50/97.62 2x2x1x1 put condors, for net level 1.0/belly over at 1156:00ET.

Same structure Blocked early Friday 6.3k from 0.75-1.0 as acct loads up on downside/rate hike insurance. SFRU2 futures currently trading 97.665 (+0.010)

- +10,000 Jun 96.25/96.50/97.00 broken put flys, 3.5 vs. 97.40/0.10%

- -3,000 Jun 98.25 straddles, 11.0

- +5,000 short Jun 96.25/96.50/96.75 2x3x1 put flys, 1.0

- 1,000 short Jun 96.12/96.25/96.37/96.50 2x2x1x1 put condors

- -4,000 short Dec 97.50 calls, 20.5 vs. 96.885/0.26%

- Overnight trade

- 2,000 Aug 96.62/96.87/97.12 put flys

- +30,000 TYM 117.5/118 put spds vs. wk4 TY 117/117.5 put spds, 2 net db/midcurve over

- +10,000 FVM 113.5 calls, 10 some vs. 113.75 calls at 5.5

- 3,200 FVM 115 calls, 0.5

- 1,700 FVM 113.25 straddles

- Update, total +10,000 TYN 121/122 call spds, 11

- Overnight trade

- 3,300 TYN 121 calls

- 5,500 TYU 123.5 calls, 28 ref 118-24 to -24.5

- 4,500 TYM 118 puts, 4

EGBs-GILTS CASH CLOSE: Flatter As Hike Expectations Rise

European yields retreated from early highs in the afternoon, with periphery EGB spreads generally wider.

- EGBs flattened in early trade as ECB's Villeroy saying he was eyeing EUR weakness, and expected June's meeting to be "decisive" for normalising policy. 2022 ECB hike expectations closed at fresh highs.

- BTP spreads pushed higher (10Y nearing 195bp) on those remarks, though narrowed over the course of the session. Greece underperformed.

- Gilts strengthened but the short-end underperformed as BoE TSC testimony highlighted familiar themes on growth and inflation concerns.

Closing Yields / 10-Yr Periphery EGB Spreads To Germany:

- Germany: The 2-Yr yield is up 3bps at 0.136%, 5-Yr is up 0.7bps at 0.606%, 10-Yr is down 1.1bps at 0.937%, and 30-Yr is down 1.9bps at 1.104%.

- UK: The 2-Yr yield is down 1.2bps at 1.237%, 5-Yr is down 1.9bps at 1.363%, 10-Yr is down 1.4bps at 1.73%, and 30-Yr is down 2.1bps at 1.977%.

- Italian BTP spread up 0.2bps at 190.6bps / Greek up 5.8bps at 259.7bps

Euribor Vol Trade And Bund Calls

Monday's Europe rates / bond options flow included:

- RXM2 158.00c, bought for 3 in 2k

- RXM2 154.5/156.00cs 1x1.5, bought for 11 in 1k

- RXM2 153.5/154.00cs, bought for 22 in 1.9k

- ERU2 99.75^, trades 22 in 2k

- ERZ2 99.37p vs 2RZ2 98.00p, bought the front for flat in 5k

- ERZ2 99.625/99.50/99.25/99.00p condor, bought for 1 in 10k

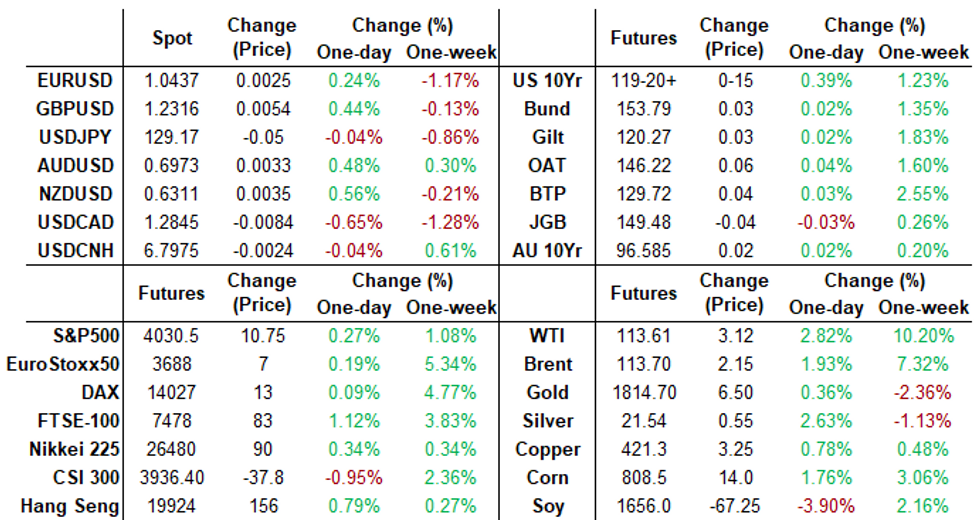

FOREX: Greenback Edges Lower To Start The Week, CAD Tops G10 Leaderboard

- Broadly the US Dollar traded in a fairly tight range on Monday as the USD index looks to finish 0.2% lower after being confined to a 32-pip range on the day.

- At the same time, USDJPY experienced a decent amount of intra-day volatility as markets have become accustomed to over recent weeks. Risk-off flows overnight following the bleak Chinese activity data had prompted a move down to 128.70 for the pair, however these Yen gains were slowly unwound throughout European trade, with the move extending into the early NY session.

- The pair peaked two pips shy of the day’s high at 129.64 before reversing once more to trade around unchanged circa 129.20 approaching the APAC crossover.

- With the Euro still trading close to cycle lows, it is worth noting that technically, EURJPY remains vulnerable with the move lower last week marking an extension of the reversal from Apr 21.

- The cross has breached a number of important S/T support levels and additional weakness at this juncture would turn the focus to an important cluster of support between 132.66 and 1.3220.

- CAD (+0.44%) is the top performer of the majors today despite some signs of moderation in the housing market. Higher oil prices acting as a tailwind for the loonie as well as rising expectations of potentially bolder future action from the BOC. Initial support eyed at the 20-day EMA of 1.2842 for USDCAD will be eyed given the overall bullish outlook in place.

- RBA minutes are scheduled overnight before a busy European and US economic data docket. This includes UK and Eurozone unemployment as well as US retail sales for April.

- Fed Chairman, Jerome Powell, is due to speak on inflation at Wall Street Journal's Future of Everything Festival, in New York. Currently scheduled for 1400ET - audience questions are expected.

Late Equity Roundup: Late Rally for Modest Gains

After trading moderately weaker most of the session, stock indexes see-sawed off lows in the second half, still an inside session range for some: SPX emini futures currently +21.5 (0.53%) at 4041.25, Dow Industrials +302.43 (0.94%) at 32495.23, Nasdaq -14.6 (-0.1%) at 11789.37.

- Earning cycle winding down w/ some big names still on tap: Home Depot and Walmart early Tuesday, Target early Wednesday; Techs: Applied Materials and Cisco Wednesday and Thursday respectively.

- SPX leading/lagging sectors: Energy sector extends strong showing +3.57% w/O&G near highs; Health Care +1.14% followed by Consumer Staples (+0.75%)

- Laggers: Consumer Discretionary (-1.22%) with autos broadly weaker (Tesla -4.38% at 735.89); Financials (-0.23%).

- Dow Industrials Leaders/Laggers: United Health outperforming (UNH) +7.49 at 492.89, Chevron (CVX) +7.02 at 174.89, followed by Caterpillar (CAT) +3.14 at 207.47.

- Laggers: Goldman Sachs (GS) -2.54 at 304.45, American Express (AXP) -2.06 at 156.69, and Salesforce (CRM) -1.65 at 165.26.

- RES 4: 4509.00 High Apr 21

- RES 3: 4393.25 High Apr 22

- RES 2: 4303.50 High Apr 26/28 and a key short-term resistance

- RES 1: 4099.00/4287.01 High May 9 / 50-day EMA

- PRICE: 4041.25 @ 1445ET May 16

- SUP 1: 3855.00/3843.25 Low May 12 / Low Mar 25 2021 (cont)

- SUP 2: 3820.25 2.50 proj of the Mar 29 - Apr 18 - 21 price swing

- SUP 3: 3787.74 2.618 proj of the Mar 29 - Apr 18 - 21 price swing

- SUP 4: 3747.52 2.764 proj of the Mar 29 - Apr 18 - 21 price swing

S&P E-Minis remain vulnerable and short-term gains are considered corrective. Last week’s continuation lower and fresh cycle lows, reinforces the primary bearish trend condition and signals scope for a continuation lower. The next objective is 3843.25, the Mar 25 2021 low (cont). In terms of resistance, the key short-term level is at 4303.50, the Apr 26/28 high. Initial resistance is at 4099.00, the May 9 high.

COMMODITIES: Oil Firms With US Gasoline Surge

- Crude oil prices have firmed strongly with US gasoline futures rising to new highs and topping $4 a gallon for the first time in the process, plus earlier protests at four sites in Libya that likely halved production to 600kbpd.

- There’s still no concrete action on the EU package on Russian oil sanctions, with the EU earlier waiting for Hungary to agree but Hungary saying it hadn’t received an update in EU proposals. EU Borrell later said that ministers didn’t agree on the sanctions and the issue will now go back to EU envoys.

- WTI is +3.0% at $113.78 having cleared three resistance levels with a high of $114.90, the highest being $113.9 (76.4% of the Mar 7-15 downleg) which opens $118.13 (Mar 9 high).

- Brent is +2.1% at $113.83 having cleared key near-term resistance at $114.00 (May 5 high) and got close to testing a bull trigger at $115.76 (Mar 24 high) with a high of $114.79.

- Gold is +0.3% at $1817.3 after USD weakness and Treasuries rally give it some respite after last week’s pressure. It earlier spiked lower to $1787.0 (new support) after breaking $1800 before rallying through the US session.

OIL: Aramco Increased Q1 Output -- Saudi Aramco reported a 13% increase in total hydrocarbons output to 13 million boe/d in the first quarter of this year versus the same period a year prior.

- Aramaco did not report its average oil production for this years first quarter, after averaging 11.5 million boe/d in first quarter 2021.

- The companies Hawiyah and Haradh gas compression projects are due to come on-stream by the end of 2022, adding 1.3 billion cubic feet per day of raw gas. Aramco is aiming to increase its gas production by more than 50% by 2030, tapping into unconventional reserves such as the Jafurah gas field.

Tuesday Data Calendar

| Date | GMT/Local | Impact | Flag | Country | Event |

| 17/05/2022 | 0130/1130 |  | AU | RBA May Meeting Minutes | |

| 17/05/2022 | 0600/0700 | *** |  | UK | Labour Market Survey |

| 17/05/2022 | 0800/1000 | ** |  | IT | Italy Final HICP |

| 17/05/2022 | 0900/1000 | ** | | UK | Gilt Outright Auction Result |

| 17/05/2022 | 0900/1100 | * |  | EU | Employment |

| 17/05/2022 | 0900/1100 | *** | | EU | EMU Preliminary Flash GDP Y/Y |

| 17/05/2022 | 0900/1100 | *** | | EU | EMU Preliminary Flash GDP Q/Q |

| 17/05/2022 | 1200/0800 |  | US | St. Louis Fed's James Bullard | |

| 17/05/2022 | 1230/0830 | *** | | US | Retail Sales |

| 17/05/2022 | 1255/0855 | ** | | US | Redbook Retail Sales Index |

| 17/05/2022 | 1315/0915 | *** | | US | Industrial Production |

| 17/05/2022 | 1315/0915 | | US | Philadelphia Fed's Patrick Harker | |

| 17/05/2022 | 1400/1000 | * | | US | Business Inventories |

| 17/05/2022 | 1400/1000 | ** | | US | NAHB Home Builder Index |

| 17/05/2022 | 1505/1605 | | UK | BOE Cunliffe Fireside Chat | |

| 17/05/2022 | 1530/1130 | ** | | US | US Treasury Auction Result for 52 Week Bill |

| 17/05/2022 | 1630/1230 | | US | Minneapolis Fed's Neel Kashkari | |

| 17/05/2022 | 1700/1900 | | EU | ECB Lagarde Speech at Soroptimist International Club | |

| 17/05/2022 | 1800/1400 | | US | Fed Chair Jerome Powell | |

| 17/05/2022 | 1830/1430 | | US | Cleveland Fed's Loretta Mester | |

| 17/05/2022 | 2245/1845 | | US | Chicago Fed's Charles Evans |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.