Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

US TSYS: Fed Firmly Focused on Inflation

US FI markets hold weaker levels after the bell -- off mid-morning lows when 30YY climbed to 3.1711%, and holding narrow band through the second half.- Brief dip in Tsy futures after Fed Chairman Powell comment on WSJ interview that the Fed "won't hesitate to raise rates above neutral if needed" to bring inflation down. Levels recovered just as quickly as Chair Powell stuck to the dual mandate boiler plate comments for the most part.

- "What we need to see is inflation coming down in a clear and convincing way," Powell told the WSJ in a webcast. "We're going to keep pushing until we see that. We don't know with any confidence what neutral is, we don't know where tight is," he said.

- Rates traded weaker post-data, retail sales excl autos better than est at 0.6% (0.4% est), control group +1.0% vs. 0.8% est. Yield curves bear flattened: 2s10s -4.454 at 26.172, 5s30s -4.277 at 1.138%.

- StL Fed Bullard comments at EIC conf: 50bp hikes "at coming meetings"; market vol "reflects policy outlook repricing". While Bullard says the Fed has a good plan in place to address inflation -- has yet to mention recession risk for US (did say doesn't think Europe will go into recession). Last week, Bullard stated recession is "not that high for the US" while the "current strong jobs market is not consistent with recession risk.

- Rather large (certainly unexpected by the broader market) corporate issuance with $6B each between United Health Care and Citigroup multi-tranche jumbos later in the second half.

SHORT TERM RATES

US DOLLAR LIBOR: Latest settlements

- O/N -0.00215 to 0.82014% (-0.00557/wk)

- 1M -0.00714 to 0.92843% (+0.04172/wk)

- 3M -0.00743 to 1.44757% (+0.00386/wk) * / **

- 6M -0.01186 to 2.00514% (+0.01014/wk)

- 12M +0.02085 to 2.67771% (+0.02557wk)

- * Record Low 0.11413% on 9/12/21; ** New 2Y high: 1.45500% on 5/16/22

STIR: FRBNY EFFR for prior session:

- Daily Effective Fed Funds Rate: 0.83% volume: $84B

- Daily Overnight Bank Funding Rate: 0.82% volume: $271B

US TSYS: Repo Reference Rates

- Secured Overnight Financing Rate (SOFR): 0.80%, $1.013T

- Broad General Collateral Rate (BGCR): 0.80%, $376B

- Tri-Party General Collateral Rate (TGCR): 0.80%, $356B

- (rate, volume levels reflect prior session)

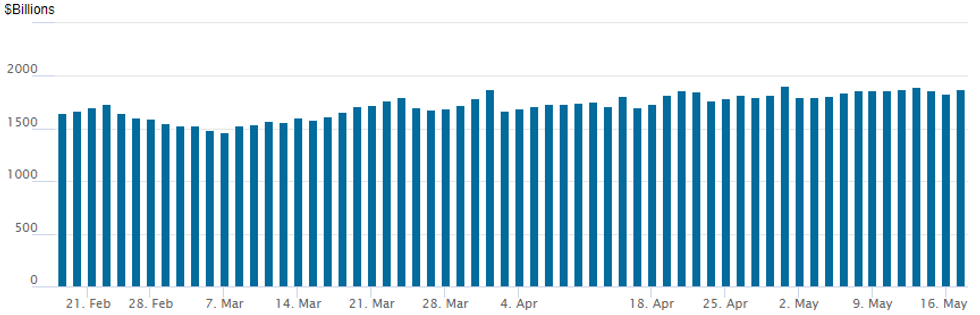

FED Reverse Repo Operation

NY Federal Reserve/MNI

NY Fed reverse repo usage currently 1,877.483B w/ 90 counterparties vs. prior session's 1,833.152B (all-time high of $1,906.802B on Friday, March 29, 2022).

EURODOLLAR/SOFR/TREASURY OPTIONS SUMMARY

Wing insurance buying more paired than the better put put buying last couple days:SOFR Options:

- +10,000 SFRQ2 97.93/98.06/98.12/98.25 call condors, 1.0

- +5,000 SFRU2 96.87/97.37 put spds, 5.5

- +5,000 short Jun 96.12/96.37 put spds, 4.25

- 6,800 Dec 99.00 calls, 1.5 ref 96.87-.875

- +3,500 Dec 97.50 calls, 40.0 vs. 96.78/0.30%

- +10,000 Sep 97.00/97.12 put spds, 2.75 ref 97.35

- Overnight trade

- +6,000 Dec 99.00 calls, 1.5

- 7,500 short Jun 96.37/96.50 put spds

- +5,000 Sep 96.68/96.93/97.81/98.06 call condors, 20.5

- 2,000 short Jul 96.25/96.44/96.62 put flys

- -3,000 TYQ 117/120 strangles, 144

- 7,000 FVM 112/114 strangles

- Overnight trade

- 6,000 USN 146/147 call spds

- +3,000 TYN 113/115.5/118 put flys, 25

EGBs-GILTS CASH CLOSE: 50bp On ECB's Agenda For July?

ECB's Knot sparked a bearish repricing at the front of European curves Tuesday with his comment that he would be open to a 50bp hike at the bank's July meeting.

- Although Knot's comments could be discounted on account of his pre-existing hawkish leanings, ECB rate hike pricing for 2022 hit a cycle high, with over 100bp in hikes priced for the year (though a 25bp raise in July remains the market's base case).

- UK yields also rose sharply, both following the EGB move and strong March wage data. 2Y Gilts sold off 20+bp.

- Periphery EGB spreads widened but not as much as might be expected given tighter ECB policy expectations.

Closing Yields / 10-Yr Periphery EGB Spreads To Germany:

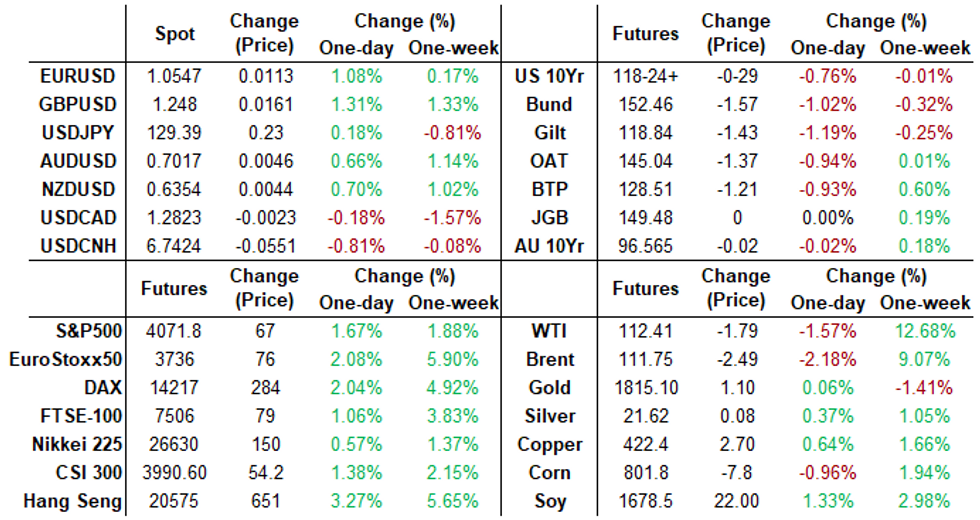

- Germany: The 2-Yr yield is up 12bps at 0.3551%, 5-Yr is up 12.8bps at 0.734%, 10-Yr is up 10.9bps at 1.046%, and 30-Yr is up 7.2bps at 1.176%.

- UK: The 2-Yr yield is up 20.8bps at 1.445%, 5-Yr is up 20.2bps at 1.565%, 10-Yr is up 15.1bps at 1.881%, and 30-Yr is up 11.5bps at 2.092%.

- Italian BTP spread up 1bps at 191.6bps / Spanish up 1bps at 107.2bps

EGB Options: Sonia Call Fly Buying And Bund Call Selling

Tuesday's Europe rates / bond options flow included:

- RXM2 155c, sold at 15 and 14.5 in 1.7k

- RXN2 150.5/149/148p fly sold vs RXN2 152/151/150.5p fly bought, net trade 2 in 2k

- OEM2 127.50/127.75cs vs 127/126.75ps, sold the cs at 4.5 in 3k

- 0RM2 98.37/98.87^^, sold down to 12.5 in 4k

- 0RM2 98.62/98.25/98.12 broken p fly, bought for 8 in 5k

- ERU2 100.00/99.87/99.75/99.50 broken put condor, bought for 2 in 10.5k

- ERH3 99.12/99.37/99.75 broken c ladder, bought for 3.25 in 2.5k

- SFIU2 98.30/98.45/98.60c fly, bought for 2 in 5k and for 2.25 in 15k (20k total)

FOREX: Greenback Slides As Risk Catches A Bid, Euro and GBP Bounce

- Renewed optimism for risk sentiment weighed on the US Dollar on Tuesday. The USD Index is down 0.82% approaching the APAC crossover, extending the week’s losses to over 1%. The majority of greenback pressure was felt during the early European session, with price largely in consolidation mode throughout US trade.

- Exacerbating the USD descent was a surging Euro, which was significantly bolstered by comments from ECB’s Knot that a bigger increase than 25bp cannot be excluded. EURUSD extended gains through 1.0450 and spent little time before breaching back above the 1.05 mark to print a 1.0556 high.

- GBP was among the best performers in G10 FX on Tuesday, closely matched by the Euro, SEK and NOK. This follows the stronger than expected UK labour market data, contributing to both sides of the GBPUSD trade amid the weaker dollar. Cable has gained around 1.3% and has consolidated just shy of 1.2500. Next resistance seen at 1.2512 High May 9.

- Equity gains have also lent support to the likes of AUD (+0.70%) and NZD (+0.75%), however, an underwhelming day for oil saw CAD relatively underperform ahead of Canadian inflation data due tomorrow.

- The USD picked up a small bid as Fed Chair Powell commented on not hesitating to raise rates above neutral, however, the greenback was only able to slightly trim losses.

- Aussie wage price index data overnight before inflation data from both the UK and Canada is scheduled for Wednesday’s session.

Late Equity Roundup, Extending Gains Late

Stocks making new late session highs after the FI close, follow through rsk on after Fed Chairman Powell's WSJ interview stuck to the dual mandate. SPX emini futures currently +79.25 (1.98%) at 4084.5, Dow Industrials +438.78 (1.36%) at 32663.54, Nasdaq +312.6 (2.7%) at 11975.88.

- Latest earnings cycle winding down: Home Depot and Walmart annc'd earlier. Home Depot was trading +6% earlier after better-than-expected earnings results for its fiscal first quarter ended May 1, pared gains/currently trades +2.28% at 302.75 (310.94 high). WMT didn't fare as well initially after cutting profit guidance on rising costs, continues to fall -11.2% at 131.64 (-16.61).

- Next to annc: Target early Wednesday, Applied Materials and Cisco Wednesday and Thursday respectively.

- SPX leading/lagging sectors: Information Technology (+2.96%) as semiconductors outperform, outpacing Materials (+2.89%) and Financials (+2.87%)

- Laggers: Consumer Staples (-1.26) food retail and super-center retailers lagging; Real Estate (+0.64%) followed by Utilities (+0.80%).

- Dow Industrials Leaders/Laggers: Goldman Sachs (GS) +9.19 at 312.63; Boeing (BA) +8.24 at 132.29. Laggers: as noted Walmart, McDonalds (-3.17 at 240.87).

E-MINI S&P (M2): Gains Appear Corrective In Nature

- RES 4: 4509.00 High Apr 21

- RES 3: 4393.25 High Apr 22

- RES 2: 4303.50 High Apr 26/28 and a key short-term resistance

- RES 1: 4099.00/4275.94 High May 9 / 50-day EMA

- PRICE: 4084.25 @ 1530ET May 17

- SUP 1: 3855.00/3843.25 Low May 12 / Low Mar 25 2021 (cont)

- SUP 2: 3820.25 2.50 proj of the Mar 29 - Apr 18 - 21 price swing

- SUP 3: 3787.74 2.618 proj of the Mar 29 - Apr 18 - 21 price swing

- SUP 4: 3747.52 2.764 proj of the Mar 29 - Apr 18 - 21 price swing

S&P E-Minis short-term gains are considered corrective and the primary trend direction remains down. Last week’s continuation lower and fresh cycle lows, reinforce the primary bearish trend condition and signals scope for a continuation lower. The next objective is 3843.25, the Mar 25 2021 low (cont). In terms of resistance, the key short-term level is 4303.50, the Apr 26/28 high. Initial resistance is at 4099.00, the May 9 high.

COMMODITIES: Crude Oil Ends Softer On Potential Venezuela Supply

- Crude oil prices ending the session lower as the US Treasury, with the decline coming as the US allows Chevron to negotiate its oil license with Venezuela’s PDVSA with a further decline into settlement.

- Prices had previously ground higher on a China re-opening/risk-on theme which also saw further increases in gasoline prices ahead of the summer driving season.

- Separately, US Treasury Officials plan to propose to European countries a tariff on Russian oil as a faster alternative to an outright ban.

- WTI is -1.6% at $112.4. Resistance is eyed at the earlier high of $115.56 after which it opens the Mar 9 high of $118.13, whilst support is the 20-day EMA of $105.52.

- Brent is -2.1% at $111.82. Resistance is the earlier high of $115.69 having stopped just shy of testing a bull trigger at $115.76 (Mar 24 high), whilst support sits at $107.87 (20-day EMA).

- Gold dips -0.45% to $1815.85 as Treasury yields rise with Fed hike expectations. It remains vulnerable despite yesterday’s recovery having traded through the $1800 handle, setting the scene for an extension lower towards the next key support at $1784.4 (Jan 28 low).

Wednesday Data Calendar

| Date | GMT/Local | Impact | Flag | Country | Event |

| 18/05/2022 | 0130/1130 | *** |  | AU | Quarterly wage price index |

| 18/05/2022 | 0600/0700 | *** |  | UK | Consumer inflation report |

| 18/05/2022 | 0600/0700 | *** | | UK | Producer Prices |

| 18/05/2022 | 0830/0930 | * | | UK | ONS House Price Index |

| 18/05/2022 | 0900/1100 | *** |  | EU | HICP (f) |

| 18/05/2022 | 1100/0700 | ** |  | US | MBA Weekly Applications Index |

| 18/05/2022 | - | | EU | ECB Lagarde & Panetta in G7 Meeting | |

| 18/05/2022 | 1230/0830 | *** |  | CA | CPI |

| 18/05/2022 | 1230/0830 | *** | | US | Housing Starts |

| 18/05/2022 | 1430/1030 | ** | | US | DOE weekly crude oil stocks |

| 18/05/2022 | 1700/1300 | ** | | US | US Treasury Auction Result for 20 Year Bond |

| 18/05/2022 | 2000/1600 | | US | Philadelphia Fed's Patrick Harker |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.