Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

US TSYS: Rates Reverse Post Jobs Move, 30YY Slips Below 3.15%

Rates trade strong after the bell, futures more than make up for Fri's sell-off on stronger than exp June employ report (+372k vs. +268k est).- Strong moves on light summer volumes, however, many accts near the sidelines to await Wed's CPI data: MoM (1.0% prior, 1.1% est); YoY (8.6%, 8.8%).

- Treasury futures held near highs, little react after $43B 3Y note auction's (91282CEY3) modest stop through: 3.093% high yield vs. 3.095% WI; 2.43x bid-to-cover vs. 2.45x last month.

- Yield curves extended bull flattening for the most part: 5s30s +1.091 at the moment at 12.770, while 2s10s extends inversion to -8.229 (-5.171), 2s5s at -2.431 (-3.680).

- Short end trades strong, however, after KC Fed George pushed back against need for "supersized" rate hikes, citing recession risks, unpredictable impacts from tightening financial conditions and market volatility. Markets had briefly started pricing in small chance of 100bps hike after Fri's data.

- Cross asset: Crude and Gold prices remain weaker: WTI at 103.74 -1.05, Gold -8.60 at 1733.82; Equities near lows: SPX emini futures ESU2 -45.25 at 3856.0.

- Reminder: Earnings season kicks off this week, with financials and banks the early focus. Just over 5% of the S&P 500 by market cap are due to report, with the releases in focus including JP Morgan, Morgan Stanley, BNY Mellon, BlackRock, Citigroup, State Street, UnitedHealth and Wells Fargo.

SHORT TERM RATES

US DOLLAR LIBOR: Latest settlements

- O/N +0.00329 to 1.56386% (-0.00672 total last wk)

- 1M +0.06472 to 1.96443% (+0.10214 total last wk)

- 3M +0.03214 to 2.45514% (+0.13014 total last wk) * / **

- 6M -0.02200 to 3.07043% (+.14914 total last wk)

- 12M +0.07714 to 3.72200% (+0.08057 total last wk)

- * Record Low 0.11413% on 9/12/21; ** New 3Y high: 2.45514% on 7/10/22

- Daily Effective Fed Funds Rate: 1.58% volume: $99B

- Daily Overnight Bank Funding Rate: 1.57% volume: $258B

- Secured Overnight Financing Rate (SOFR): 1.53%, $942B

- Broad General Collateral Rate (BGCR): 1.51%, $368B

- Tri-Party General Collateral Rate (TGCR): 1.51%, $345B

- (rate, volume levels reflect prior session)

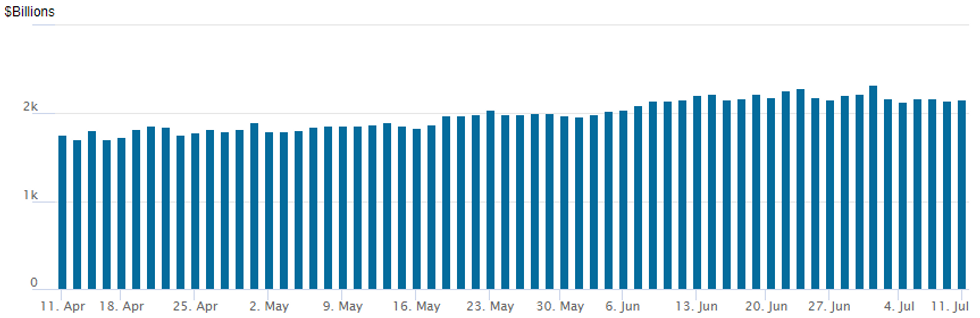

FED Reverse Repo Operation

NY Federal Reserve/MNI

NY Fed reverse repo usage climbs to $2,164.266B w/ 96 counterparties vs. $2,144.921B prior session. Record high stands at $2,329.743B from Thursday June 30.

EURODOLLAR/SOFR/TREASURY OPTIONS SUMMARY

Minimal option volume still centered on downside puts, hedge/insurance vs. more aggressive rate hikes despite underlying futures moderating forward expectations after last Fri's strong jobs gain for Jun (+372) saw 10YY climb back to 3.099%.- Highlight Eurodollar trade includes +25,000 (20k Blocked) ec 96.00/96.50 put spreads at 27.0 ref 96.23. Salient Treasury option trade had paper selling 22,000 TYU 115.5/121.5 call over risk reversals from 0.0-1.0 while 5Y options included a scale buyer of over 25,000 FVU 111.5 puts from 50-53. Lone upside call trade: 39,000 TYU 119/121 call spreads at 35 ref 117-27 to -27.5.

- 1,000Jul 97.18 calls, cab

- 5,000 Dec 96.00/96.50 put spds, 27.0 ref 96.23 adds to +20k Block

- Block, total +20,000 Dec 96.00/96.50 put spds, 27.0 vs. 96.21/0.20%

- -1,000 short Dec 96.87 straddles, 98.0

- seller Mar 96.25 straddles, 103

- 3,500 Dec 95.50 puts, 12.5-13.0

- over -22,000 TYU 115.5/121.5 call over risk reversals, 0.0-1.0, mostly the latter and still offered

- over 15,000 TYU 120 calls, 52

- 11,100 FVU 111.5 puts, 52-53

- 5,000 TYQ 114/115 put spds

- 39,000 TYU 119/121 call spds, 35 ref 117-27 to -27.5

- Blocks, 15,000 FVU 111.25 puts, 50-52.5 vs. 104-24 to -24.5

- 5,000 TYU 119 calls, 100

- 5,000 TYU 119.5 calls, 54-55

EGBs-GILTS CASH CLOSE: Recession Trade Resumes

Bund and Gilt yields fell to start the week, as the familiar themes of recession fears (and US dollar strength) were prevalent.

- Monday's strength was enough to largely reverse Friday's sell-off following the US jobs report, with concerns over global recession resuming (China Covid lockdowns and Russia-Eurozone gas dispute the proximate causes).

- Otherwise, it was a relatively quiet session for European fixed income despite the advance, with EUR/USD nearing parity taking the headlines, and little in the way of speakers or impactful data.

- Bobl outperformed on the German curve, with the UK belly also outperforming.

- Periphery EGB spreads tightened intraday but finished a little wider.

Closing Yields / 10-Yr Periphery EGB Spreads To Germany:

- Germany: The 2-Yr yield is down 8.5bps at 0.442%, 5-Yr is down 10.1bps at 0.865%, 10-Yr is down 9.9bps at 1.246%, and 30-Yr is down 7.2bps at 1.537%.

- UK: The 2-Yr yield is down 5bps at 1.88%, 5-Yr is down 5.6bps at 1.856%, 10-Yr is down 5.5bps at 2.178%, and 30-Yr is down 3.3bps at 2.602%.

- Italian BTP spread up 2.2bps at 196.6bps / Spanish up 1.7bps at 108.9bps

EGB Options: A Few Bund Puts In The Mix Monday

Monday's Europe rates / bond options flow included:

- RXQ2 149/148/147 put fly bought for 7 paid in 2.75k

- RXU2 149/156 RR, bought the put for 116 in 2.3k

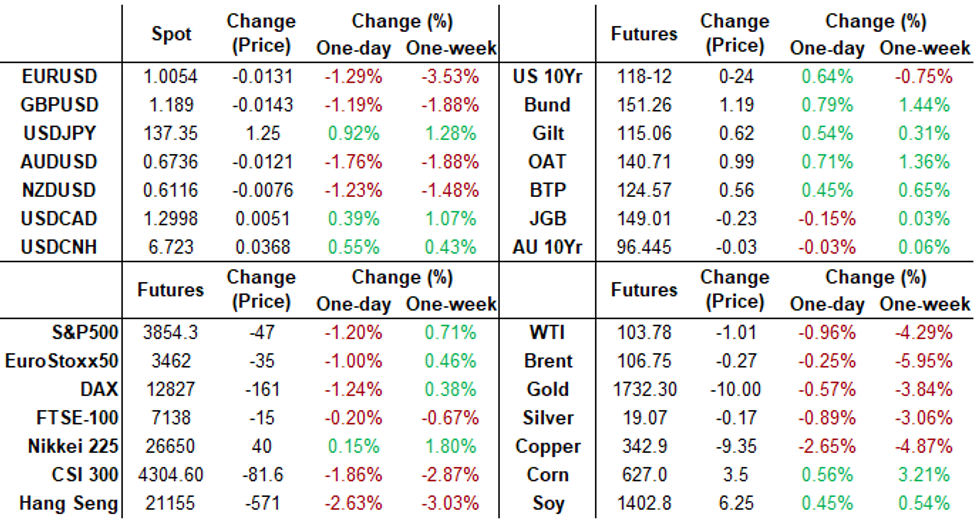

FOREX: Greenback Rally Extends, AUD Plummets To Fresh Two-Year Low

- A volatile start to the week for FX markets has been underpinned by continued US Dollar demand as a sense of risk-off permeates across global markets.

- The USD Index has advanced just shy of 1% from Friday’s close, rising to fresh multi-decade highs above the 108.00 mark.

- With risk under pressure once more, AUDUSD finds itself at the bottom of the G10 pile, having plummeted 1.6%. The notably strong sell-off today has resulted in a breach of support at 0.6762, the Jul 5 / 6 low and 0.6759, 50.0% of the Mar ‘20 - Feb ‘21 bull cycle. The break lower confirms a resumption of the technical downtrend and sets the scene for a move towards 0.6685, the Mar 9, 2020 high. On the upside, initial firm resistance is now seen at 0.6874, the 20-day EMA.

- Similarly, NZD and GBP are registering losses greater than 1%, along with the single currency, which now finds itself within striking distance of parity against the greenback as anxieties surrounding European gas supplies continue to mount.

- EURUSD printed a fresh cycle low of 1.0053 and overall trend conditions remain bearish. Weakness last week resulted in a break of 1.0350, May 13 low, to confirm a resumption of the primary downtrend. The move lower also highlights an acceleration of the bear cycle. The technical focus is on 1.0009, the base of a channel drawn from the Feb 10 high, just ahead of parity.

- Additionally, the Japanese Yen showed few signs of halting its steep downtrend as USDJPY surged above 137 to peak at 137.75, continuing to reach the highest levels seen since 1998.

- Another light day for economic data on Tuesday with German ZEW Economic Sentiment highlighting the European docket. Wednesday remains in focus with rate decisions from both the RBNZ and BOC but also US June inflation readings.

FX: Expiries for Jul12 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.0175-85(E521mln), $1.0260-70(E1.2bln)

- USD/JPY: Y135.55-60($1.0bln), Y137.60-65($1.2bln)

- NZD/USD: $0.6250(N$1.2bln)

- USD/CNY: Cny6.7000($1.3bln)

Late Equity Roundup: Weaker Mid-Range

Stocks trading modestly weaker, near the middle of the session range at the bell, directional with Tsy yields as rates more than make up for last Fri's post-jobs data sell-off. SPX eminis currently trading -45.75 (-1.17%) at 3855.5; DJIA -177.59 (-0.57%) at 31160.3; Nasdaq -254.5 (-2.2%) at 11381.97

- SPX leading/lagging sectors: Utilities moves to the fore (+0.42%) followed by Real Estate (+0.21%) and Health Care +0.01%. Laggers: Communication Services (-2.58%) weighed down by Twitter (TWTR) -9.95% after Elon Musk announced late Friday he wants to back out of purchase, lawsuits to follow.

Next up: Consumer Discretionary (-2.33%) weighed down by autos, particularly Tesla (TSLA) -5.91%. - Dow Industrials Leaders/Laggers: Visa Inc (V) takes the lead +2.37 at 205.94, Home Depot (HD) +1.95 at 288.42, Merck (MRK) +1.31 at 94.09. Laggers: Caterpillar (CAT) -3.83 at 175.27, Boeing (BA) -2.79 at 136.28 and Goldman Sachs (GS) -2.33 at 294.14.

- Reminder: Earnings season kicks off this week, with financials and banks the early focus. Just over 5% of the S&P 500 by market cap are due to report, with the releases in focus including JP Morgan, Morgan Stanley, BNY Mellon, BlackRock, Citigroup, State Street, UnitedHealth and Wells Fargo.

E-MINI S&P (U2): Remains Below Key Resistance

- RES 4: 4308.50 High Apr 28

- RES 3: 4204.75 High May 31 and a key resistance

- RES 2: 3985.11 50-day EMA

- RES 1: 3950.00 High Jun 27

- PRICE: 3876.25 @ 14:24 BST Jul 11

- SUP 1: 3735.00/3639.00 Low Jun 23 / 17 and the bear trigger

- SUP 2: 3578.27 0.618 proj of the Mar 29 - May 20 - 31 price swing

- SUP 3: 3500.00 Round number support

- SUP 4: 3384.75 0.764 proj of the Mar 29 - May 20 - 31 price swing

S&P E-Minis traded higher last week and price remains above recent lows. The outlook is bearish though following the reversal from 3950.00, the Jun 28 high. The next support lies at 3735.00, the Jun 23 low. A breach of this level would expose key support at 3639.00, the Jun 17 low. On the upside, clearance of resistance at 3950.00 is required to reinstate a bullish theme. This would open the 50-day EMA, currently at 3985.11.

COMMODITIES: China Demand Fears And Risk-Off Weigh On Oil, Gold

- Crude oil prices are flat to down as part of a session with broader risk-off sentiment. There was a particular impact from renewed concerns over Chinese demand as Shanghai began mass testing for Covid symptoms, whilst supply is bolstered by the CPC pipeline being allowed to continue carrying Kazakhstan exports. In products, Bolsonaro says Brazil is close to buying diesel from Russia.

- WTI is -0.65% at $104.11, off a low of $100.91 but with the bear cycle intact and with support next eyed at $95.10 (Jul 6 low).

- Brent is +0.05% at $107.07, off the intraday high of $107.7 and close to resistance at the 50-day EMA of $109.02 but with a bearish outlook and support at $98.5 (Jul 6 low).

- Gold meanwhile has fallen further as dollar strength continues to bite, -0.44% at $1734.74 having got close to last week’s low of $1732.3 (Jul 6 low). Having cleared a key short-term support and bear trigger of $1787, further momentum could see it open $1721.7 (Sep 29, 2021 low).

- Separately, the Texas power grid is facing its biggest test of the year amidst scorching temperatures, with the grid issuing a conservation alert and asking users to reduce consumption.

Tuesday Data Calendar

| Date | GMT/Local | Impact | Flag | Country | Event |

| 12/07/2022 | 2301/0001 | * |  | UK | BRC-KPMG Shop Sales Monitor |

| 12/07/2022 | 0800/0900 | | UK | BOE Cunliffe on Crypto Markets | |

| 12/07/2022 | 0900/1100 | *** |  | DE | ZEW Current Conditions Index |

| 12/07/2022 | 0900/1100 | *** | | DE | ZEW Current Expectations Index |

| 12/07/2022 | 0900/1000 | ** | | UK | Gilt Outright Auction Result |

| 12/07/2022 | 0900/1000 | | UK | BOE Bailey Speaks at OMFIF | |

| 12/07/2022 | 1000/0600 | ** |  | US | NFIB Small Business Optimism Index |

| 12/07/2022 | - |  | EU | ECB de Guindos at ECOFIN Meeting | |

| 12/07/2022 | 1255/0855 | ** | | US | Redbook Retail Sales Index |

| 12/07/2022 | 1400/1000 | ** | | US | IBD/TIPP Optimism Index |

| 12/07/2022 | 1530/1130 | ** | | US | US Treasury Auction Result for 52 Week Bill |

| 12/07/2022 | 1600/1200 | *** | | US | USDA Crop Estimates - WASDE |

| 12/07/2022 | 1630/1230 | | US | Richmond Fed's Tom Barkin | |

| 12/07/2022 | 1700/1300 | ** | | US | US Note 10 Year Treasury Auction Result |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.