Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

US TSYS: Rates Quietly Rebound, Yld Curves Hold 22 Year Inverted Lows

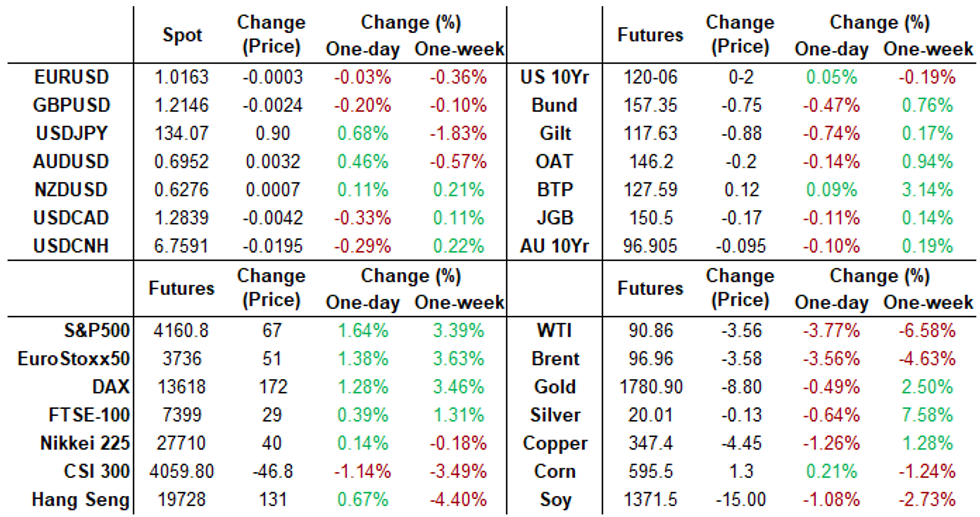

Tsy futures drifting near modest session highs after the bell - wide range on decent volume (TYU2>1.6M) after rebounding steadily off midmorning lows. Yield curves still near inverted lows not seen since late 2000: 2s10s currently -6.205 ast -36.662 vs. -37.202 low.

- Hawkish Fed messaging continues: StL Fed Bullard on CNBC earlier echoing Daly and Mester's messaging: Fed job "nowhere near" complete in reining in inflation while needing months of "convincing evidence" that infl has peaked.

- That said, SF Fed Daly clarified/softened her view slightly saying 50bp hike in Sep a "reasonable thing to do." Mkts appeared to ignore MN Fed Kashkari comments after the close: inflation fight a bigger priority than recession, while market bets on rate cuts are very unlikely.

- Meanwhile, US Tsy annc fourth consecutive reduction in its quarterly sales of longer-term debt as borrowing needs diminished and signaled a pause going forward. Reductions in short-end auction sizes was not widely expected (2s, 3s), the rest was more or less in line by the looks of it.

- Data on tap for Thursday: Challenger Job Cuts YoY, Initial Jobless Claims (260k est), Continuing Claims (1.383M est). Larger focus on Friday's July employment report (+250k est vs. +372K prior).

- Current cross assets: spot Gold rebounds +$5.39 (0.31%) at $1765.35, Crude weaker: WTI -$3.57 (-3.78%) at $90.81, stocks near recent session highs ESU2 +72.5 points (1.77%) at 4160.75.

- Currently, 2-Yr yield is up 4.3bps at 3.0937%, 5-Yr is up 0.7bps at 2.8599%, 10-Yr is down 1.6bps at 2.7319%, and 30-Yr is down 4.8bps at 2.9581%.

SHORT TERM RATES

US DOLLAR LIBOR: Latest settlements

- O/N +0.00315 to 2.31029% (-0.01128/wk)

- 1M +0.01900 to 2.37629% (+0.01400/wk)

- 3M +0.02529 to 2.83229% (+0.04400/wk) * / **

- 6M +0.07557 to 3.38900% (+0.05914/wk)

- 12M +0.13543 to 3.84314% (+0.13585/wk)

- * Record Low 0.11413% on 9/12/21; ** New 3.5Y high: 2.80586% on 7/27/22

- Daily Effective Fed Funds Rate: 2.33% volume: $95B

- Daily Overnight Bank Funding Rate: 2.32% volume: $278B

- Secured Overnight Financing Rate (SOFR): 2.30%, $1.015T

- Broad General Collateral Rate (BGCR): 2.27%, $399B

- Tri-Party General Collateral Rate (TGCR): 2.26%, $381B

- (rate, volume levels reflect prior session)

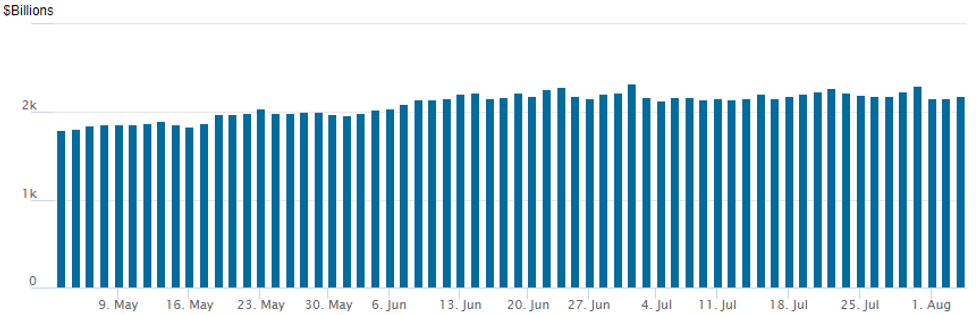

FED Reverse Repo Operation

NY Federal Reserve/MNI

NY Fed reverse repo usage climbs to $2,182.238B w/ 105 counterparties vs. $2,156.013B prior session. Record high still stands at $2,329.743B from Thursday June 30.

EURODOLLAR/SOFR/TREASURY OPTIONS SUMMARY

FI option trade focused on better downside put insurance buying interspersed by upside call unwinds Wednesday as underlying futures traded weaker as Fed speakers continued to remind markets inflation is too high and 75bp hike in Sep not off the table.

- Heavy short end selling continued as StL Fed Bullard on early CNBC interview echoed Daly and Mester's messaging: Fed job "nowhere near" complete in reining in inflation while needing months of "convincing evidence" that inflation has peaked. Meanwhile, SF Daly added Wednesday that markets are ahead of themselves expecting rate cuts in 2023.

- SOFR option volume outpaced Eurodollar options, salient trade included sale of 20,000 SFRZ2 96.12/97.12 call over risk reversals, 1.25 vs. 96.625/0.48%, buy of 15,000 short Aug SOFR 96.12/96.62 put spds, 10.25-10.75 and 15,000 short Aug 96.12/96.62 put spds, 10.25-10.75.

- +4,000 SFRV2 96.37/96.50 put spds .75 over 97.25 call spds vs. 96.59/0.20%

- Block, 2,500 SFRZ2 96.50/96.62/97.50 call trees, 0.25

- Block, 3,000 short Aug 95.12/95.75/96.00 put trees, 0.25

- +15,000 short Aug 96.12/96.62 put spds, 10.25-10.75

- Block, total 12,500 short Aug 96.75 puts, 6.0-6.5

- Block 10,000 SFRZ2 96.62/96.75/97.50 broken call trees, 1.0 credit (96.62 calls bought vs. 2 legs)

- 4,000 SFRZ2 96.12/97.12 call over risk reversals, 1.25 cr - adds to -20k Block

- +20,000 SFRZ2 97.50/97.75 call spds, 2.0 ref 96.615

- Block, 3,000 SFRH3 95.75/96.12 put spds, 10.0 vs. 96.60/0.08%

- Block, total -20,000 SFRZ2 96.12/97.12 call over risk reversals, 1.25 vs. 96.625/0.48%

- 5,000 Sep 96.25/96.37 put spds

- Block, +3,000 Dec 98.00/98.81 call spds 1.25 w/ SFRZ2 96.62/96.75/97.50 broken call trees (10k call trees blocked earlier) 0.25 net db/package

- total -20,000 TYV 122 calls, 40-42

- 2,000 FVU 111 puts, 9

- 3,000 FVU 112.25/112.5 put spds

- 3,600 TYU/wk1 TY 119.5 put spds 26

FOREX Greenback Supported By Firmer US Services PMI, USDJPY Extends Recovery

- A stronger-than-expected US Services PMI print further weighed on the front-end of the TSY curve, bolstering the US Dollar on Wednesday. The greenback index had largely been consolidating before the data after yesterday’s strong recovery, however, there was a notable uptick following the above consensus reading. Despite a 30 tik retreat off the intra-day highs, the USD Index (+0.25%) has marginally extended on yesterday’s rebound.

- A consolidation of hawkish Fed rhetoric over the past 24 hours continues to fuel the renewed optimism for the greenback keeping the USD underpinned as we approach Friday’s important jobs report.

- Bottom of the G10 pile on Wednesday is the Japanese Yen with USDJPY posting another huge daily range. The 134 handle initially capped the rally overnight in Asia and evidence of the significant volatility, the pair pulled back as much as 150 pips to 132.40 before consolidating above 133 for much of the European session. Price action continued to look perky into the US session and the ISM data prompted another spike in price to a daily high of 134.55, over 400 pips above yesterday’s low.

- Mixed price action across the rest of G10 with no clear theme driving the price action. A decent rally in global equity benchmarks has benefitted the likes of AUD and CAD, filtering through to a boost for crosses such as AUDJPY and CADJPY which have both risen over 1%.

- In similar vein in emerging markets, bolstered risk sentiment in equities helped the Mexican Peso rise 1.6%, however, the move largely reflects a reversal of the steep rally in USDMXN on Tuesday, with the pair just marginally above yesterday’s close.

- The Bank of England is the headline risk event on Thursday. The median surveyed estimate looks for a 50bp hike to bank rate, however, some analysts are predicting a smaller 25bp increase.

- A relatively light docket in the US (jobless claims and trade balance data) paves the way for Friday’s release of US Non-Farm payrolls.

FX: Expiries for Aug04 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.0100(E691mln), $1.0150-60(E1.9bln), $1.0200-10(E1.bln), $1.0215-30(E1.7bln), $1.0295-00(E1.3bln)

- USD/JPY: Y129.35-45($2.4bln), Y132.00($863mln), Y133.00($1.4bln), Y134.25-31($590mln), Y134.80-00($2.4bln), Y135.05-10($778mln)

- AUD/USD: $0.7000(A$582mln)

- USD/CAD: C$1.2750($745mln)

- USD/CNY: Cny6.75($1.6bln)

Late Equity Roundup, Running Near Highs, Retailing Outpacing Autos

Stock indexes trading higher, near late session highs into the FI close after ignoring more hawkish Fed speak earlier as short end rates back to pricing in >50% chance of 75bp hike at end of month. SF Fed Daly clarified/softened her view slightly saying 50bp hike in Sep a "reasonable thing to do."

- Currently, SPX eminis trade +69.75 (1.7%) at 4163.25; DJIA +462.73 (1.43%) at 32856.28; Nasdaq +331.4 (2.7%) at 12678.77.

- Earnings releases continues after the close: Marathon Oil (MRO) $1.267 est, MetLife (MET) $1.447 est, EBAY $0.896 est.

- SPX leading/lagging sectors: Consumer Discretionary gained late (+2.80%) as retailing outpaced autos, Information Technology (+2.79%) and Communication Services sector (+2.46%) as media and entertainment remained strong (Dish +6.54%, Meta +5.04%, Warner Bros +4.69%, Disney +4.00%). Laggers: Energy sector remained weak (-2.49%), followed by Materials (+0.33%) and Utilities (+0.39%).

- Dow Industrials Leaders/Laggers: Microsoft (MSFT) +8.13 at 282.95, Goldman Sachs (GS) +7.0 at 334.88, Salesforce.COM (CRM) +6.40 at 190.19. Laggers: Chevron (CVX) -3.94 at 155.2, Walmart (WMT) -2.18 at 130.50, Caterpillar (CAT) -0.41 at 183.10.

E-MINI S&P (U2): Bulls Still In The Driver's Seat

- RES 4: 4345.75 2.00 proj of the Jun 17 - 28 - Jul 14 price swing

- RES 3: 4306.50 High May 4

- RES 2: 4204.75 High May 31 and a key resistance

- RES 1: 4147.25 High Aug 01

- PRICE: 4112.50 @ 12:57 BST Aug 3

- SUP 1: 3978.47/13.25 50-day EMA / Low Jul 26 and key S/T support

- SUP 2: 3820.25 Low Jul 18

- SUP 3: 3723.75/3639.00 Low Jul 14 / Low Jun 17 and a bear trigger

- SUP 4: 3578.27 0.618 proj of the Mar 29 - May 20 - 31 price swing

S&P E-Minis remain below recent highs. The short-term outlook is bullish and short-term dips are considered corrective. For bulls, a break of Monday’s 4147.25 high would confirm a resumption of recent gains and open 4204.75 next, the May 31 high and the next key resistance. On the downside, initial trend support has been defined at 3913.25, the Jul 26 low. A break would highlight a possible reversal.

COMMODITIES: Oil Slides On Weak US Demand, Gas Volatility Continues

- Crude oil slides despite the initial rise following OPEC+ agreeing to a small production increase of just +100k in September, helped lower by a sharp drop in US gasoline demand to sit at the lowest since Feb and more than 1mbpd below the 2015-19 average.

- WTI is -3.2% at $91.39, through support at $94.91 (Aug 1 low) and closer to the bear trigger of $88.23 (Jul 14 low).

- Brent is -3.2% at $97.34, also moving closer to a key short-term support at $96.7 (Jul 25 low).

- Gold is +0.15% at $1763.3, little changed from a technical viewpoint whilst sitting above the 20-day EMA of $1748.9.

- Natural gas meanwhile remains in focus. EU prices sees continued volatility with continued turbine back and forth on whether it can be delivered or not (NBP +2.4%, TTF -2.9%) – most recently with Gazprom saying the Western sanctions make the return of the turbine impossible.

- Henry Hub prices in the US on the other hand surged +7% later in the session potentially coinciding with Freeport LNG’s Consent Agreement with the PHMSA plus Germany’s Uniper saying coal supplies may be limited by Rhine water levels, increasing demand for US gas in the process.

Thursday Data Calendar

| Date | GMT/Local | Impact | Flag | Country | Event |

| 04/08/2022 | 0130/1130 | ** |  | AU | Trade Balance |

| 04/08/2022 | 0600/0800 | ** |  | DE | Manufacturing Orders |

| 04/08/2022 | 0700/0300 | * |  | TR | Turkey CPI |

| 04/08/2022 | 0730/0930 | ** |  | EU | IHS Markit Final Eurozone Construction PMI |

| 04/08/2022 | 0800/1000 | | EU | ECB August Economic Bulletin | |

| 04/08/2022 | 0830/0930 | ** |  | UK | IHS Markit/CIPS Construction PMI |

| 04/08/2022 | 1100/1200 | *** | | UK | Bank Of England Interest Rate |

| 04/08/2022 | 1130/1230 | | UK | BOE Press Conference | |

| 04/08/2022 | 1230/0830 | * |  | CA | Building Permits |

| 04/08/2022 | 1230/0830 | ** |  | US | Jobless Claims |

| 04/08/2022 | 1230/0830 | ** | | US | Trade Balance |

| 04/08/2022 | 1400/1000 | ** | | US | WASDE Weekly Import/Export |

| 04/08/2022 | 1430/1030 | ** | | US | Natural Gas Stocks |

| 04/08/2022 | 1530/1130 | * | | US | US Bill 08 Week Treasury Auction Result |

| 04/08/2022 | 1530/1130 | ** | | US | US Bill 04 Week Treasury Auction Result |

| 04/08/2022 | 1600/1200 | | US | Cleveland Fed's Loretta Mester |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.