Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

US TSYS: Tsy Yield Curves Bear Steepen Post-FOMC Minutes

Tsys remain weaker after the bell but off session lows, yield curves bear steepening ( 2s10s gapped to session high of -38.963) following July FOMC minutes release, as market digests comments like:- Officials saw risk the Fed could tighten more than necessary; and as the stance of monetary policy tightened further, it likely would become appropriate at some point to slow the pace of policy rate increases while assessing the effects of cumulative policy adjustments on economic activity and inflation." Link to minutes:

- https://www.federalreserve.gov/monetarypolicy/files/fomcminutes20220727.pdf

- Lead quarterly Eurodollar futures EDU2 climbed to session high of 96.675 (+0.025) after the release as market expectations of more than 50bp hike at Sep 21 cool (despite there being ample time and data between now and then).

- US rates had sold off overnight after higher than expected UK CPI (+0.6% MoM; +10.1 YoY) underscored expectations of further tightening from the BoE.

- Fast two-way trade on decent volumes after steady July Retail sales read vs. +0.1% est (prior 1.0% revised to +0.8%), but higher in Ex-Auto +0.4% MoM vs. -0.1% est (prior 1.0% revised to +0.9%), ex-Auto/Gas +0.7% vs. 0.4% est and Control Group +0.8% (prior 0.8% revised +0.7%) vs. 0.6% est.

- Tsy futures gapped back to session lows briefly following weak $15B 20Y bond auction (912810TK4) tails: 3.380% high yield vs. 3.355% WI; 2.30x bid-to-cover vs. last month's 2.65x.

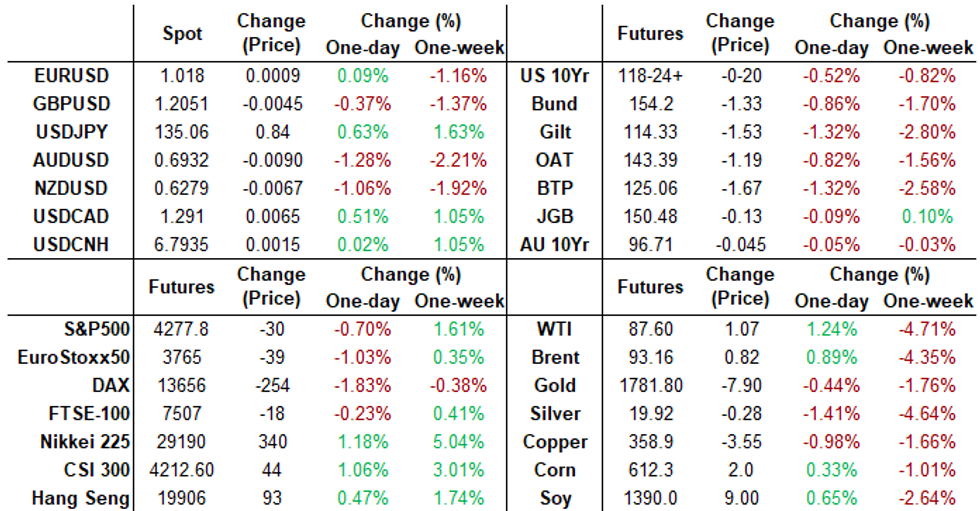

- The 2-Yr yield is up 2.5bps at 3.2828%, 5-Yr is up 9.5bps at 3.0477%, 10-Yr is up 8.9bps at 2.8931%, and 30-Yr is up 5.8bps at 3.1472%.

SHORT TERM RATES

US DOLLAR LIBOR: Latest settlements

- O/N -0.00872 to 2.31357% (-0.00129/wk)

- 1M -0.01143 to 2.36557% (-0.02129/wk)

- 3M +0.01600 to 2.97657% (+0.05500/wk) * / **

- 6M +0.00171 to 3.50771% (-0.00158/wk)

- 12M +0.04486 to 3.99557% (+0.03657/wk)

- * Record Low 0.11413% on 9/12/21; ** New 14Y high: 2.97657% on 8/17/22

- Daily Effective Fed Funds Rate: 2.33% volume: $94B

- Daily Overnight Bank Funding Rate: 2.32% volume: $289B

- Secured Overnight Financing Rate (SOFR): 2.29%, $974B

- Broad General Collateral Rate (BGCR): 2.26%, $393B

- Tri-Party General Collateral Rate (TGCR): 2.26%, $387B

- (rate, volume levels reflect prior session)

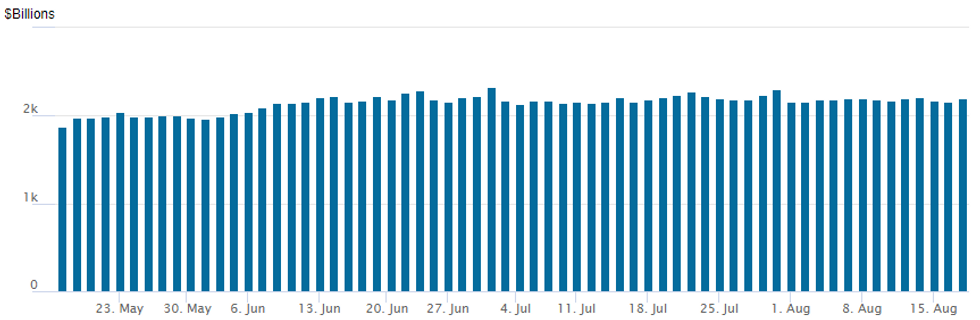

FED Reverse Repo Operation

NY Federal Reserve/MNI

NY Fed reverse repo usage climbs to $2,199.631B w/ 103 counterparties vs. $2,165.332B prior session. Record high still stands at $2,329.743B from Thursday June 30.

EURODOLLAR/SOFR/TREASURY OPTIONS SUMMARY

Mixed on net after slight pick-up in early call spd buying post-data. Continued put fly unwinds in Sep Eurodollar options:

SOFR Options:- +2,500 SFRZ3 93.00/94.00/95.00 put flys, 5.5

- Block +9,750 SFRF3 96.00/96.25 put strip, 51.0 vs. 96.275

- Block, 10,000 Sep 96.43/96.56 2x1 put spds, 0.0 ref 96.6225

- Block, -20,000 Sep 96.12/96.50/96.87 put flys, 19.0 vs. 96.615/0.37%, adds to appr -65k Block sales since Monday, unwinding

- +2,000 short Dec 96.50 straddles, 72.5

- +10,000 Sep 96.62/Mar 96.00 call spd

- 10,000 Sep 98.75/99.00 put spds

- 5,500 Sep 98.75/99.50 put spds

- 2,000 Sep 98.75/99.37 put spds

- 2,000 TYV 120/121.5 call spds, 24

- 2,000 TYU 119.25 calls, 25

- 1,500 TUU 105.25/105.37 call spds

- +5,000 FVU 112 calls, 22.5 vs. 111-28.25

- 2,000 TYU 118.75 calls, 37 ref 118-24.5

- -8,000 FVU 111.5/111.75 put spds, 6 vs. 111-27.25

- Block, total 10,000 FVV 111.25/112.25 put spds, 24-25.5

EGBs-GILTS CASH CLOSE: Short End Crashes On UK Double-Digit CPI

A higher-than-expected 10.1% UK July CPI reading (a 40-Yr high, vs 9.8% expected) set an extremely bearish tone for Wednesday trade, with short-end instruments badly underperforming as central bank hike expectations ratcheted up.

- European curves bear flattened, with the UK leading the way, as 200+bp of BoE hikes are now priced in this cycle (including a decent chance of 75bp in Sept), vs 170bp yesterday.

- The UK curve inverted further, 2s10s to lowest since 2008, 2s5s since 2007 as 2Y yields hit a post-2008 high.

- The German short end also sold off, with ECB hike pricing higher but not as much as BoE.

- The highest-beta EGB periphery sovereigns - Italy and Greece - underperformed, with 10Y spreads widening around 7bp.

Closing Yields / 10-Yr Periphery EGB Spreads To Germany:

- Germany: The 2-Yr yield is up 15.4bps at 0.731%, 5-Yr is up 15.4bps at 0.898%, 10-Yr is up 11.2bps at 1.083%, and 30-Yr is up 6.2bps at 1.292%.

- UK: The 2-Yr yield is up 24.8bps at 2.403%, 5-Yr is up 18.3bps at 2.148%, 10-Yr is up 16.3bps at 2.288%, and 30-Yr is up 10.8bps at 2.623%.

- Italian BTP spread up 7bps at 223.3bps / Greek up 6.7bps at 243.2bps

EGB Options: Euribor Midcurve Unwind And Large Bund Downside

Wednesday's Europe rates / bond options flow included:

- OEV2 148/146.50ps 1x1.25, bought for 9.75 in 3k

- OEV2/OEU2 put calendar, bought the Oct for 54 in 3k vs 126.28

- RXU2 155/156 call spread bought for 33 in 3.3k

- RXV2 146p, bought for 51 and 53 in 15k (ref 151.75 in Dec)

- 0RU2 98.50/98.25ps sold in 5k vs 2RU2 98.37/98.12ps bought in 5k receiving 3 (unwinding)

- 0RU2 97.875/98.625/98.375p fly, bought 2.25 in 6k

- ERZ2 99.00/98.875/98.75/98.625p condor vs 99.50c, bought the condor for flat in 30k

FOREX: USD Index Pares Gains Following Fed Minutes, Antipodean Weakness Prevails

- Mixed session for currencies across the G10 space on Wednesday with the dollar gaining ground against most other majors, however, notably underperforming against the Euro.

- Prior to the release of the FOMC minutes, AUD and NZD had significantly extended their overnight moves to the downside amid higher US yields and a decent pullback for major equity indices. The higher yields had also worked against the Japanese yen with USDJPY trading above pre-US CPI levels to within close proximity of resistance at 135.58. Overall, this propped up the dollar index, which was trading with 0.3% gains heading into the minutes.

- The minutes came as a dovish cue rather than being massaged in a hawkish direction, led by headlines that whilst some officials still see the Fed Funds rate below neutral, officials saw a slower pace of rate hikes at some point with many officials seeing risk that the Fed could tighten more than necessary. As such, the greenback saw a kneejerk reaction lower, and the USD Index now trades at closed to unchanged levels approaching the APAC crossover.

- An unchanged DXY fails to paint the full picture though as AUD (-1.10%) and NZD (-0.90%) remain notably lower following the earlier RBNZ meeting and Aussie wage price index data. Similarly the Japanese Yen holds onto 0.6% losses for Wednesday.

- While the Euro had been relatively outperforming all day with a notable recovery for the likes of EURAUD, EURNZD and EURJPY, the late USD selloff propelled EURUSD (+0.20%) to briefly trade at fresh highs above the 1.02 mark. Although showing relative strength, the pair still remains comfortably below the week’s opening levels with the ongoing energy crisis capping any bullish momentum up to this point.

- Aussie employment data highlights the docket overnight before the Norges bank decision at 0900BST where the most recent July CPI print tilts the balance of risks to another 50bps rate rise.

- Philly Fed Manufacturing, jobless claims and existing home sales are the US data points of note with potential comments from Fed’s George and Kashkari to watch out for.

FX: Expiries for Aug18 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.0147-57(E1.5bln), $1.0175($802mln), $1.0200-05(E1.0bln), $1.0215-30(E2.1bln), $1.0240-50(E1.0bln), $1.0290-00($786mln)

- USD/JPY: Y132.00($1.4bln), Y133.85-00($1.2bln), Y134.50-60($1.0bln), Y137.60-80($796mln)

- AUD/USD: $0.6975(A$822mln)

- USD/CNY: Cny6.80($611mln)

Late Equity Roundup: Off Lows, Energy Sector Leads

Stocks still weaker after the FI close, but near late session highs -- bouncing after July FOMC minutes release deemed less hawkish. Currently, SPX eminis trade -31 (-0.72%) at 4277.25; DJIA -172.43 (-0.5%) at 33980.63; Nasdaq -154.5 (-1.2%) at 12948.79.

- Stocks had followed Tsys lower since overnight after UK CPI surged (+0.6% MoM; +10.1 YoY) triggered extended rate hike expectations into 2023 (hopes of rate cut in 2023 evaporating).

- Equity earnings after the close: Synopsys (SNPS) $2.038 est; Cisco (CSCO) $0.816 est; Bath and Body Works (BBBI) $0.446 est. Earlier: Target (TGT) earnings miss (irony) -$0.39 vs. $0.725 est. Meanwhile, Lowe's Group (LOW) beat: $4.67 vs $4.611 est; Analog Devices (ADI) beat: $2.52 vs. $2.442 est.

- SPX leading/lagging sectors: Energy continued to outperform (+0.65%) lead by petroleum shares: Valero (VLO) +4.34%, Marathon (MPC) +2.35%, ConocoPhillips (COP) +1.45%; Utilities (-0.21%) and Consumer Staples (-0.19%) follow. Laggers: Communication Services (-1.63%) w/ media/entertainment underperforming, followed by Materials (-1.46%) and Consumer Discretionary (-1.04%).

- Dow Industrials Leaders/Laggers: Apple (AAPL) +2.31 at 175.36, McDonalds (MCD) +1.32at 137.88, IBM +1.30 at 137.86. Laggers: Boeing (BA) -4.33 at 167.75, Visa (V) -2.74 at 214.30, 3M (MMM) -2.84 at 147.42.

COMMODITIES: Crude Bounces With Unexpected US Draw

- Crude oil bounced after an unexpected draw in EIA crude stocks, driven by record exports and a dip in production. Furthermore, refinery utilization was down more the expected due to a fall in the Gulf, East and West Coasts whilst there was a big draw in gasoline with implied demand recovering back above 2020 levels and towards normal.

- WTI is +1.4% at $87.78, earlier only just holding off Aug 16 lows of $85.73, which still forms support, clearance of which would have exposed Mar 15 lows of $85.37. On the upside, key short-term resistance is defined at $95.05 (Aug 11 high), whilst today’s most active strikes in the CLU2 have been $90/bbl calls.

- Brent is +1.1% at $93.35, again having come close to the bear trigger at $91.22 (Jul 14 low). Should the increase continue, key short-term resistance is seen at $100.38 (Aug 12 high).

- Gold meanwhile suffers again, sliding -0.46% at $1767.56 with USD strength and higher Tsy yields, gaining only some respite from a more dovish than expected set of FOMC minutes. It clears support at the 20-day EMA of $1772.4, opening key short-term support at $1754.4 (Aug 3 low).

Thursday Data Calendar

| Date | GMT/Local | Impact | Flag | Country | Event |

| 18/08/2022 | 0130/1130 | *** |  | AU | Labor force survey |

| 18/08/2022 | 0600/0800 | ** |  | NO | Norway GDP |

| 18/08/2022 | 0800/1000 | *** | | NO | Norges Bank Rate Decision |

| 18/08/2022 | 0900/1100 | *** |  | EU | HICP (f) |

| 18/08/2022 | 0900/1100 | ** | | EU | Construction Production |

| 18/08/2022 | 1100/0700 | * |  | TR | Turkey Benchmark Rate |

| 18/08/2022 | 1230/0830 | * |  | CA | Industrial Product and Raw Material Price Index |

| 18/08/2022 | 1230/0830 | ** |  | US | Jobless Claims |

| 18/08/2022 | 1230/0830 | ** | | US | Philadelphia Fed Manufacturing Index |

| 18/08/2022 | 1230/0830 | ** | | US | WASDE Weekly Import/Export |

| 18/08/2022 | 1400/1000 | *** | | US | NAR existing home sales |

| 18/08/2022 | 1400/1000 | * | | US | Services Revenues |

| 18/08/2022 | 1400/1000 | ** | | US | leading indicators |

| 18/08/2022 | 1430/1030 | ** | | US | Natural Gas Stocks |

| 18/08/2022 | 1530/1130 | * | | US | US Bill 08 Week Treasury Auction Result |

| 18/08/2022 | 1530/1130 | ** | | US | US Bill 04 Week Treasury Auction Result |

| 18/08/2022 | 1700/1300 | ** | | US | US Treasury Auction Result for TIPS 30 Year Bond |

| 18/08/2022 | 1715/1915 | | EU | ECB Schnabel Presentation at IHK Reception | |

| 18/08/2022 | 1720/1320 | | US | Kansas City Fed's Esther George | |

| 18/08/2022 | 1745/1345 | | US | Minneapolis Fed's Neel Kashkari |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.