Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

HIGHLIGHTS

- EVANS BACKS RATES AROUND 4.5% IN `23 AND ON HOLD FOR SOME TIME, Bbg

- GERMANY BACKS JOINT EU DEBT FOR LOANS TO TACKLE ENERGY CRISIS, Bbg early session

- GERMAN GOVT SOURCE REJECTS REPORT SAYING BERLIN BACKS JOINT EU DEBT FOR LOANS TO EASE ENERGY CRISIS, Reuters later in session

Key links: MNI: Fed's Evans Sees Rates Holding Above 4.5% By Early 2023 / MNI US Employment Insight, Oct'22: Fourth 75bp Hike Almost A Done Deal / MNI INSIGHT: Fed Sees Fin. Stability As Separate From Rates / MNI: Fed’s Brainard Sees Restrictive Policy For Some Time

US Tsys: FI Off Lows, Germany Debt Scheme Denied

Tsys and stock indexes rebounded off session lows after headline hit that Germany denies backing "joint EU debt for loans to ease energy crisis" Rtrs -- FI and stocks sold off early on headline German WOULD back the debt scheme.

- Otherwise, quiet session on VERY light volumes (TYZ2<445k; USZ2<85k) due to Columbus Day US bank holiday - full session for Globex, however, while holiday's in Japan, Korea, and Canada contributing to thin markets.

- No data on the day (focus on Sep FOMC minutes Wednesday and CPI Thursday) while Chicago Fed Evans and Fed VC Brainard both made comments on policy at Chicago Fed NABE bank conf on the day. Little react to Evans, but Brainard came off slightly dovish: "the combined effect of concurrent global tightening is larger than the sum of its parts" while the "Federal Reserve takes into account the spillovers of higher interest rates, a stronger dollar, and weaker demand from foreign economies into the United States".

- The 2-Yr yield is unchanged at 4.3078%, 5-Yr is unchanged at 4.1423%, 10-Yr is unchanged at 3.8814%, and 30-Yr is unchanged at 3.8417%.

SHORT TERM RATES

US DOLLAR LIBOR: Latest settlements:

- 1M +0.00314 to 3.31671% (+0.17086 total last wk)

- 3M +0.01043 to 3.91914% (+0.15400 total last wk) * / **

- 6M +0.04272 to 4.42743% (+0.15271 total last wk)

- 12M +0.05371 to 5.0500% (+0.21572 total last wk)

- * Record Low 0.11413% on 9/12/21; ** New 14Y high: 3.91914% on 10/10/22

EURODOLLAR/SOFR/TREASURY OPTIONS SUMMARY

Monday's Columbus day bank holiday hampered liquidity w/ trade volume limited to Globex. Mixed flow as decent downside put insurance buying outpaced sporadic call trades as chances of 75bp rate hike in November continued to firm. Salient trades:- SOFR Options:

- 10,000 SFRV2 95.43/95.56 2x1 put spds

- 10,000 SFRV2 95.43 puts

- 2,000 SFRX2 95.81/95.93/96.06 call flys

- 1,050 SFRZ2 96.00/96.12/96.25/96.37 call condors

- Block, 4,000 SFRZ2 96.00/96.25 call spds, 1.75 ref 95.535

- 4,000 SFRZ2 97.75 calls

- Eurodollar Options:

- 7,500 EDH3 94.37/95.12/95.62 put flys

- 4,000 Dec 95.18/95.37 3x2 put spds

- 6,300 EDZ2 95.50/95.75 call spds

- 8,000 EDZ2 95.12/95.37 put spds

- Treasury Options:

- 4,000 TYX2 115 calls, 2

- 2,000 TYZ2 106 puts, 18

- 3,000 TYZ 110/111 put spds, 27

- 3,100 FVZ 111.5/112.5 call spds

- 3,000 TYZ2 107.5/110/112.5 put flys

Late Equity Roundup: Off Lows, Nothing Fundamental

Stock indexes still weaker in late trade, but off session lows, bouncing w/ Tsys after headline Germany denies backing "joint EU debt for loans to ease energy crisis" Rtrs (FI and stocks sold off early on headline German WOULD back the debt scheme).

That said, Information Technology and Energy sectors continue to underperform. Currently, SPX eminis trade -13.5 (-0.37%) at 3640; DJIA -25.66 (0.09%) at 29320.12; Nasdaq -57.3 (-0.5%) at 10594.1.

- SPX leading/lagging sectors: Carry-over weakness in Information Technology (-1.19%) as semiconductor makers feel pressure from Pres Biden's new export measures to China. Energy (-2.07%) as crude traded lower (WTI -1.40 at 91.24). Leaders: Utilities (+0.64%) w/gas, electric and independent power names evenly paired, Consumer Staples (+0.57%) and Industrials (+0.50%).

- Dow Industrials Leaders/Laggers: Amgen (AMGN) +3.69 at 232.72, Merck (MRK) +2.76 at 90.36, Boeing (BA) +1.49 at 131.28. Laggers: United Health (UNH) -6.39 at 498.46, Microsoft (MSFT) -4.95 at 229.29, Salesforce Inc (CRM) -5.06 at 145.23

E-MINI S&P (Z2): Broader Trend Direction Remains Down

- RES 4: 4234.25 High Aug 26

- RES 3: 4175.00 High Sep 13 and a key resistance

- RES 2: 3908.86 50-day EMA

- RES 1: 3820.00 High Oct 5

- PRICE: 3625.00 @ 1430ET Oct 10

- SUP 1: 3571.75 Low Oct 3 and the bear trigger

- SUP 2: 3558.97 1.382 proj of the Aug 16 - Sep 7 - 13 price swing

- SUP 3: 3506.38 1.50 proj of the Aug 16 - Sep 7 - 13 price swing

- SUP 4: 3453.78 1.618 proj of the Aug 16 - Sep 7 - 13 price swing

S&P E-Minis remains below last week’s high of 3820.00 on Oct 5. This level marks a key resistance, where a break is required to reinstate a short-term bullish theme. The broader trend remains down and attention is on the bear trigger at 3571.75, the Oct 3 low. A break of this level would confirm a resumption of the broader downtrend and open 3558.97, a Fibonacci projection.

COMMODITIES: Crude Oil Pulls Back After Last Week's Stellar Gains

- Crude oil retraces some of last week’s stellar gains, falling -2% in what are seen as overbought markets after its 17% gain.

- Earlier in the session, Exxon is said to weigh the takeover Denbury, the US’s largest carbon-dioxide pipeline network, which Bloomberg reports as being potentially the biggest carbon-management investment since the Inflation Reduction Act passed in August and its large tax incentives for burying carbon dioxide.

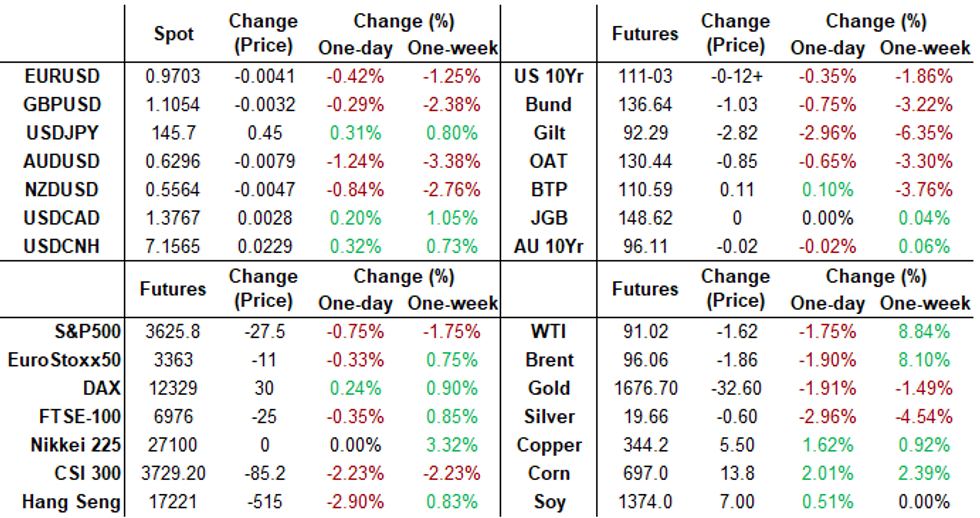

- WTI is -1.9% at $90.93, pulling back from an intraday high of $93.64 that now forms initial resistance but remaining above initial support at $79.14 (Sep 30 low).

- Most active strikes in CLX2 have been $85/bbl puts today.

- Brent is -2.0% at $95.98, down from an overnight high of $98.75 that also forms resistance but again not troubling support.

- Gold is -1.5% at $1669.5 on a largely one way decline today as USD strength extended. It easily cleared support at 1695.2 (former trendline resistance) to open 1659.7 (Oct 3 low).

Tuesday Data Calendar

| Date | GMT/Local | Impact | Flag | Country | Event |

| 11/10/2022 | 2301/0001 | * |  | UK | BRC-KPMG Shop Sales Monitor |

| 11/10/2022 | 2330/1030 |  | AU | Westpac-MI Consumer Sentiment | |

| 11/10/2022 | 0030/1130 | | AU | NAB Business Survey | |

| 11/10/2022 | 0600/0700 | *** | | UK | Labour Market Survey |

| 11/10/2022 | 0800/1000 | * |  | IT | Industrial Production |

| 11/10/2022 | 0900/1000 | * | | UK | Index Linked Gilt Outright Auction Result |

| 11/10/2022 | 1000/0600 | ** |  | US | NFIB Small Business Optimism Index |

| 11/10/2022 | - |  | EU | ECB Panetta IMF/World Bank Annual Meetings | |

| 11/10/2022 | 1245/1445 | | EU | ECB Lane Keynote Speech | |

| 11/10/2022 | 1400/1000 | ** | | US | IBD/TIPP Optimism Index |

| 11/10/2022 | 1530/1130 | | US | Philadelphia Fed's Patrick Harker | |

| 11/10/2022 | 1530/1130 | * | | US | US Treasury Auction Result for 13 Week Bill |

| 11/10/2022 | 1530/1130 | * | | US | US Treasury Auction Result for 26 Week Bill |

| 11/10/2022 | 1600/1200 | | US | Cleveland Fed's Loretta Mester | |

| 11/10/2022 | 1700/1300 | *** | | US | US Note 03 Year Treasury Auction Result |

| 11/10/2022 | 1800/1900 | | UK | BOE Cunliffe Panels IIF Annual Meeting | |

| 11/10/2022 | 1800/2000 | | EU | ECB Lane NY Fed Fireside Chat | |

| 11/10/2022 | 1835/1935 | | UK | BOE Bailey in Conversation w. Tim Adams at IIF Meeting |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.