Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

- Treasury yields marked the highest levels since mid-November this morning: 10Y at 4.4621%, finished day at 4.4178%.

- Generally subdued session no significant data to speak of for the next two sessions.

- Focus firmly on Wednesday's CPI and March FOMC minutes, PPI on Thursday.

US TSYS 10Y Yield Taps Mid-Nov High, Focus on Wed's CPI, Fed Minutes

- Treasury futures finished weaker but off lows Monday, 10Y yield marking the highest level since mid-November at 4.4621%.

- The NY Fed’s consumer inflation expectations were mixed in March. Full report here. Otherwise, limited data to speak of for the next two sessions, focus on Wednesday's CPI and March FOMC minutes, PPI on Thursday.

- Projected rate cut pricing continued to ebb: May 2024 at -4.7bp w/ cumulative -1.2bp at 5.317%; June 2024 at -48.8% w/ cumulative rate cut -13.4bp at 5.195%. July'24 cumulative at -22.1bp, Sep'24 cumulative -38.2bp.

- A downtrend in Treasuries remains intact and today’s move lower marks a bearish start to the week. The contract has breached support at 109-09+, the Apr 3 low to confirm a resumption of this year's downtrend. The break lower opens the 109-00 handle and 108-25+, a Fibonacci projection level. Key short-term resistance has been defined at 110-31+, the Mar 27 high. First resistance to watch is 110-06, the Apr 4 high.

SOFR FIXES AND PRIOR SESSION REFERENCE RATES

SOFR Benchmark Settlements:

- 1M -0.00104 to 5.31742 (-0.01028 total last wk)

- 3M +0.00384 to 5.29723 (-0.00484 total last wk)

- 6M +0.01052 to 5.23086 (+0.00253 total last wk)

- 12M +0.02147 to 5.05254 (+0.03125 total last wk)

- Secured Overnight Financing Rate (SOFR): 5.32% (+0.00), volume: $1.898T

- Broad General Collateral Rate (BGCR): 5.31% (+0.00), volume: $705B

- Tri-Party General Collateral Rate (TGCR): 5.31% (+0.00), volume: $695B

- (rate, volume levels reflect prior session)

- Daily Effective Fed Funds Rate: 5.33% (+0.00), volume: $88B

- Daily Overnight Bank Funding Rate: 5.32% (+0.00), volume: $247B

FED Reverse Repo Operation

NY Federal Reserve/MNI

- RRP usage inches bounces to $448.597B vs $438.319B on Friday. Compares to mid-March low of $413.877B - the lowest level since May 2021.

- Meanwhile, the latest number of counterparties at 74 vs. 67 Friday (near the lowest number of counterparties since July 7, 2021).

SOFR/TEASURY OPTION SUMMARY

SOFR and Treasury options leaned toward better downside put flow on net Monday -- carry over hedging higher (steady) for longer rates after last Friday's jobs surge for March (+303k). Underlying futures extending lows while projected rate cut pricing continues to ebb: May 2024 at -4.7bp w/ cumulative -1.2bp at 5.317%; June 2024 at -48.8% w/ cumulative rate cut -13.4bp at 5.195%. July'24 cumulative at -22.1bp, Sep'24 cumulative -38.2bp.

- SOFR Options:

- +10,000 SRK4 94.75/94.81 put spds 2.75 ref 94.82

- +6,000 SRN4 94.62/94.75/94.87 put flys 2 ref 95.05

- 5,000 SFRJ4 94.87/94.93/95.00 call flys

- 5,000 0QJ4 95.50 puts, 1.5 vs. 95.675/0.10%

- Block, +10,000 SFRJ4 94.87/94.93 call spds, 0.75

- -5,000 SFRM4 94.75/94.87 call strip, 16.25 ref 94.82

- Block, 15,000 SFRZ4 96.62 calls, 7.5 vs. 95.33/0.09%

- +8,000 SRQ4 94.93/95.06/95.18 put fly 1.75 ref 9505.5

- +4,000 SRU4 95.00/95.25 put spd vs 95.75/96.00 call spds 15.5 ref 9505

- -8,000 SRM4 94.62/94.68/94.87 1x1x1 put fly 10.0-9.75 ref 9482

- +4,000 SRM4 95.25/95.50 call spds cab, ref 9482

- +4,000 SFRU4 94.43/94.68 put spds, 1.75 ref 95.06

- -5,000 SFRZ4 95.25/95.50 call spds, 8.5 ref 95.315

- +4,000 SFRN4 95.00/95.18/95.37 call flys, 3.75

- Block, +4,000 2QM4 95.37/95.62 put spds, 3.0

- 5,000 SFRJ4 94.62/94.75 put spds ref 94.82

- 2,500 2QM4 94.93/95.06/95.18 put flys

- +5,000 0QM4 96.25/96.75 call spds, 4.0 vs. 94.69/0.14%

- +5,000 SFRQ4 94.93/95.06/95.18 put flys, 1.75

- +7,000 SFRM4 94.87/95.00 call spds 3.0

- +6,000 SFRN4 95.00/95.18/95.37 call flys, 3.75

- 2,500 SFRJ4 94.87/94.93 call spds ref 94.815

- 2,300 SFRU4 95.06/95.18/95.50/95.62 call condors ref 95.04

- Treasury Options:

- Update, +40,000 FVM4 106 puts 42-42.5

- 6,000 TYM4 106/107.5/109 put flys, 15 ref 109-04 to -05

- 3,000 USM4 118 calls, 124 ref 116-20

- 3,350 wk3 10Y 107.5/108/109 broken put flys rtef 109-02.5

- 3,900 USK4 115 puts, 44 last ref 116-14

- 1,500 FVM4 104/104.5/105/105.5 put condors ref 105-31

- +6,500 wk2 FV 105.25/105.5 put spds 3

- +3,000 Wed wk2 108/108.5 2x1 put spds 2

- Block/screen -15,000 TYK4 111.25/111.5 call spds, 2 vs. 109-10/0.08

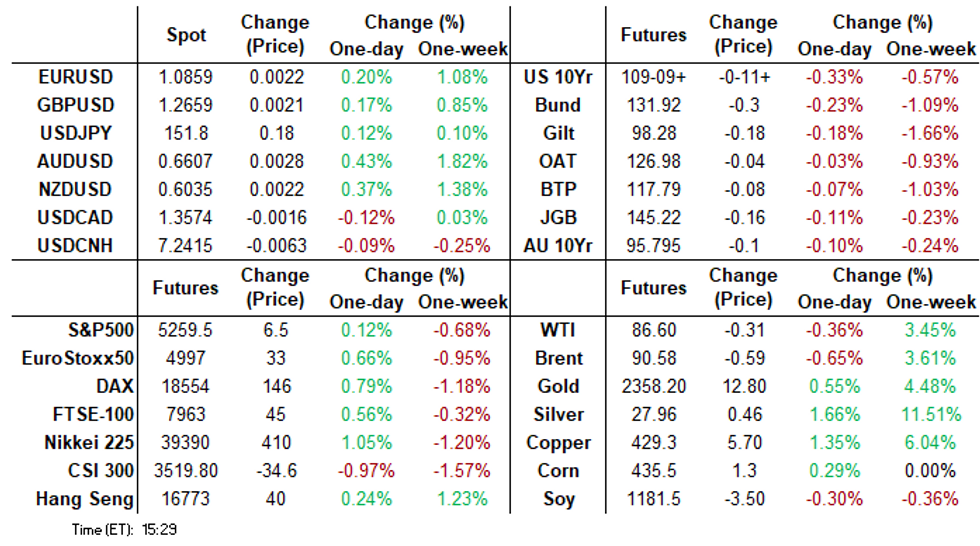

EGBs-GILTS CASH CLOSE: Caught Between US Data Points, Bunds Underperform

The German curve bear flattened Monday, with the belly underperforming on the UK curve.

- Stronger-than-expected German industrial production data continued the negative tone for European core FI set after Friday's robust US jobs data. While there was little otherwise in the way of newsflow or macro developments Monday, focus was firmly on hawkish risks from the upcoming US CPI reading on Wednesday.

- Bunds underperformed Gilts, with notable underperformance of the German short end (though ECB cut pricing was little changed on the day).

- Periphery EGB spreads closed tighter, as equities clawed back some of Friday's losses.

- Our latest Europe Pi showed broad short-setting across the futures space last week, with BTP structural positioning moving into short territory.

- MNI's preview of Thursday's ECB meeting was published today (PDF). With limited expectations of the ECB changing tack ahead of a presumptive June cut, any adjustment to the official communication this week would represent a minor surprise.

- Overnight we get UK BRC retail sales, while Tuesday brings the ECB Bank Lending Survey, and supply from Austria, Belgium, and Germany.

Closing Yields / 10-Yr Periphery EGB Spreads To Germany

- Germany: The 2-Yr yield is up 5.2bps at 2.927%, 5-Yr is up 5.1bps at 2.441%, 10-Yr is up 3.6bps at 2.435%, and 30-Yr is up 1.6bps at 2.586%.

- UK: The 2-Yr yield is up 1bps at 4.234%, 5-Yr is up 2.3bps at 3.946%, 10-Yr is up 1.6bps at 4.085%, and 30-Yr is up 1.4bps at 4.591%.

- Italian BTP spread down 2.4bps at 139.4bps / Spanish bond spread down 1.8bps at 81.7bps

EGB Options: Mixed Structures In Light Trade Monday

Monday's Europe rates/bond options flow included:

- OEK4 119/120cs 1x2, bought for 1 in 4.25k

- RXM4 130/128ps, bought for 32 and 33 in 5k

- SFIZ4 95.70/96.10/96.50/96.90c condor, sold at 7.75 in 2k

- SFIZ4 95.75/96.75cs vs 95.25p, bought the cs for 1.75 in 5k

FOREX Renewed CHF Weakness, Antipodeans & Scandies Outperform

- The greenback was little phased by rising US yields on Monday, with the USD index marginally in the red, down 0.11% at typing. This coincides with latest indicative positioning data which shows the USD Index net position has consolidated at lows, with outright position now short of 1,896 contracts, the lowest since 2021.

- CHF remains the poorest performer on the session, a move that's keeping the uptrend in EUR/CHF underpinned. Cycle highs at 0.9849 remain the bull trigger, a break above which puts the cross at the best levels since April last year.

- Interestingly, UBS noted that while the CHF may continue to depreciate a little in the short-term, the expected tightening of the ECB/SNB and Fed/SNB policy rate spread will likely raise the risk of CHF appreciation in the longer-term.

- With equity markets consolidating the post-payrolls bounce, AUD and NZD are rising around 0.4%. The recent bounce in AUDUSD has resulted in a break of resistance around the 50-day EMA. This marks a bullish development and suggests the recent bout of weakness between Mar 8 - Apr 1 has been a correction

- In similar vein, Scandi currencies are among the session's best performers, with NOK shrugging off the pullback in oil prices. EUR/NOK trades close to last week's lows, with the striking of a sizeable wage deal with labour unions adding to domestic inflationary pressure and possibly restricting the Norges Bank's space with which to ease policy this year.

- USDJPY has traded in a narrow 151.70-90 range, with 152.00 continuing to cap the topside, a level that continues to dominate the focus ahead of this week’s US CPI release and the ongoing threat of possible MOF intervention.

FX Expiries for Apr09 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.0800(E685mln), $1.0860-75(E604mln)

- USD/JPY: Y151.50($1.1bln), Y153.00-15($987mln)

- AUD/USD: $0.6615-30(A$1.5bln)

- USD/CNY: Cny7.2200($980mln)

Late Equities Roundup: Holding Modest Gains

- Stocks hold modestly higher territory late Monday, off midday highs amid light position squaring. Stock held to a narrow range as markets await Wednesday's CPI and FOMC minutes. Currently, DJIA is up 32.49 points (0.08%) at 38936.26, S&P E-Minis up 5.75 points (0.11%) at 5258.75, Nasdaq up 23.3 points (0.1%) at 16271.68.

- Leading Gainers: Consumer Discretionary and Real Estate sectors continued to outperform late in the session. A combination of autos, cruise-lines and personal product distributors supported the Consumer Discretionary sector: Tesla +5.38% amid talk of autonomous EV taxi venture, Bath & Body Works +3.12%, Carnival +3.01% and Norwegian Cruise Line +2.81%

- Meanwhile, Real estate investment trusts, particularly residential and office REITs buoyed the latter: Camden Property +5.46%, Mid-America Apartment +4.11%, Boston Properties +3.34%.

- Laggers: Health Care and Information Technology sectors underperformed, biotech extending lows late: Merck -1.31%, Eli Lilly -0.95%, Vertex Pharmaceuticals -0.75%. Meanwhile, hardware makers weighed on IT: Super Micro -1.37%. Seagate -0.90%, Apple -0.52%.

- Reminder, the next quarterly earnings starts in earnest late this week with JP Morgan, BlackRock, Wells Fargo, State Street and Citigroup reporting Friday, April 12.

E-MINI S&P TECHS: (M4) Corrective Bear Cycle Remains In Play

- RES 4: 5434.54 Bull channel top drawn from the Jan 17 low

- RES 3: 5428.25 1.00 proj of the Oct 27 - Dec 28 - May 1 price swing

- RES 2: 5400.00 Round number resistance

- RES 1: 5308.50/33.50 High Apr 4 / 1 and the bull trigger

- PRICE: 5257.50 @ 1455 ET Apr 8

- SUP 1: 5191.50 Low Apr 5

- SUP 2: 5144.64 50-day EMA

- SUP 3: 5100.00 Round number support

- SUP 4: 5018.00 Low Feb 21

The trend condition in S&P E-Minis remains bullish, however, the recent move lower highlights a corrective cycle and last week's sell-off reinforces this condition. The contract has breached bull channel support drawn from the Jan 17 low, and cleared the 20-day EMA. This has exposed the 50-day EMA, at 5144.64 and the next important support. Key resistance and the bull trigger is 5333.50, the Apr 1 high.

COMMODITIES Spot Gold Pares Gains From Fresh Record High, Crude Slips Back

- Spot gold rose to yet another record high early in Monday’s session, reaching $2,353.95/oz, before paring gains over the course of the day.

- The yellow metal is currently up 0.5% at $2,341/oz. While some analysts have continued to raise their year-end price forecasts, TD Securities note the risk of a reversal given the excess of safe haven demand in the absence of a further escalation in the middle east.

- From a technical perspective, the trend condition in gold remains bullish, with sights on $2376.5 next, a Fibonacci projection. Initial firm support is at $2210.1, the 20-day EMA.

- Meanwhile, crude had has slipped back today following cautious optimism of progress on a Gaza ceasefire deal. However, recent news of the proposal’s rejection by Hamas is likely to put a dent in such hope.

- WTI May 24 is down 0.5% at $86.5/bbl.

- Following the recent rally in WTI futures, the next objective is $89.08, a Fibonacci projection, a break of which would pave the way for a climb towards the $90.00 handle. On the downside, initial firm support to watch lies at $82.42, the 20-day EMA.

- Front month Henry Hub has risen today amid upside support from above-normal demand.

- US Natgas May 24 is up 2.9% at $1.84/mmbtu.

TUESDAY DATA CALENDAR

| Date | GMT/Local | Impact | Flag | Country | Event |

| 09/04/2024 | 2301/0001 | * |  | UK | BRC-KPMG Shop Sales Monitor |

| 09/04/2024 | 0645/0845 | * |  | FR | Foreign Trade |

| 09/04/2024 | 0900/1000 | ** | | UK | Gilt Outright Auction Result |

| 09/04/2024 | 1000/0600 | ** |  | US | NFIB Small Business Optimism Index |

| 09/04/2024 | 1255/0855 | ** | | US | Redbook Retail Sales Index |

| 09/04/2024 | 1530/1130 | * | | US | US Treasury Auction Result for Cash Management Bill |

| 09/04/2024 | 1700/1300 | *** | | US | US Note 03 Year Treasury Auction Result |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.