Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

HIGHLIGHTS:

- Sterling slips as markets await yet another Brexit deadline

- US government averts government shutdown with last minute deal

- Focus shifts to next week's rate decisions, with US, UK, Norway, Switzerland, Mexico and more

US TSYS SUMMARY: Waiting-And-Seeing On Stimulus, Fed

A solid if unexciting session for Treasuries, with most gains made overnight on no-deal Brexit concerns.

- We had modest follow through in U.S. hours as markets considered potential for a government shutdown at midnight, and a continued COVID fiscal impasse.

- Slightly sub-par volume too, with a real wait-and-see feel on political developments and next week's FOMC.

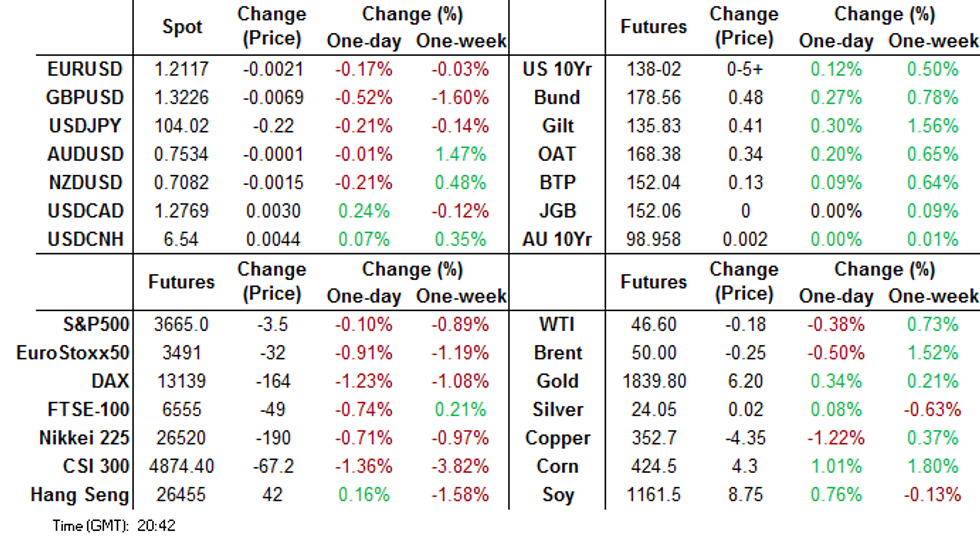

- Curve mixed, with the belly outperforming. The 2-Yr yield is down 2bps at 0.117%, 5-Yr is down 3.5bps at 0.3512%, 10-Yr is down 2.5bps at 0.8816%, and 30-Yr is down 1.2bps at 1.6151%.

- Mar 10-Yr futures (TY) up 8.5/32 at 138-05 (L: 137-26.5 / H: 138-07)

- Attention has also been on equities which continue to stumble after recent all-time highs; in contrast data (mildly weaker-than-expected PPI, strong beat in UMichigan sentiment) didn't really move the needle significantly.

- That said, plenty of data next week, which will provide greater insight into the economic impact of the 2nd wave of the pandemic: retail sales, flash PMI, housing starts, and industrial production all on the docket.

EGBs-GILTS CASH CLOSE: Rally Ahead Of Sunday 'Deadline' For Deal

Gilts have faded early gains made on no-deal Brexit concerns, but yields still remain firmly lower, with bull flattening intact. That said, Bunds actually outperformed on the day, with periphery spreads widening, as Eurozone equities fell sharply.

- FI opened strong on headlines that EU's von der Leyen told European leaders that a no-deal outcome was more likely than not, and later PM Johnson described no-deal as " very, very likely".

- The next deadline to reach a deal in the Brexit saga is said to be Sunday, though already various officials have suggested that this is not necessarily the end of the road.

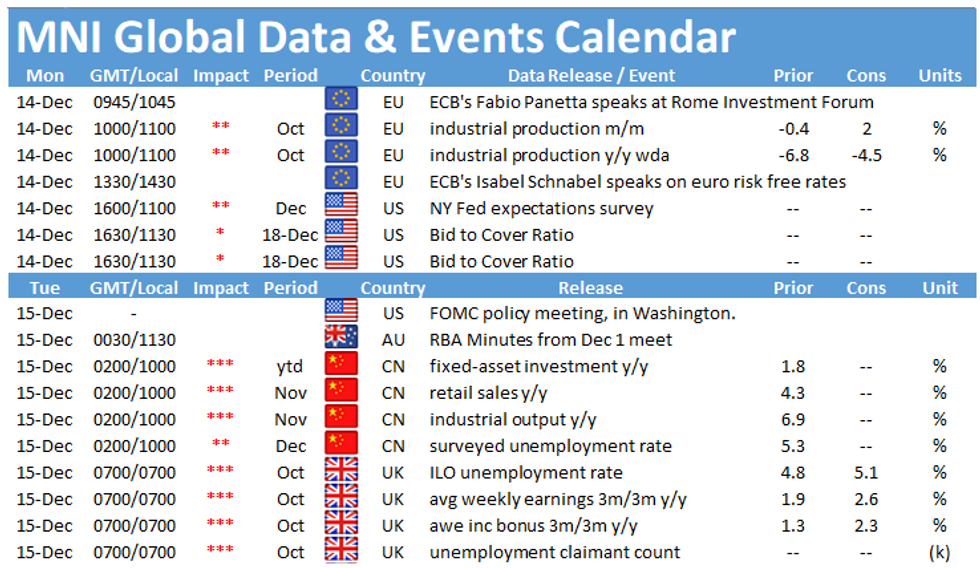

- Thin calendar otherwise early next week, little in the way of data/speakers, and no bond supply the entire week. BoE Thursday is the main event.

Closing Levels / 10-Yr Periphery EGB Spreads:

- Germany: The 2-Yr yield is down 1.7bps at -0.783%, 5-Yr is down 2.5bps at -0.812%, 10-Yr is down 3.3bps at -0.636%, and 30-Yr is down 5.3bps at -0.239%.

- UK: The 2-Yr yield is up 0.3bps at -0.112%, 5-Yr is down 1.2bps at -0.095%, 10-Yr is down 2.9bps at 0.172%, and 30-Yr is down 3.1bps at 0.713%.

- Italian BTP spread up 2.9bps at 119.4bps

- Spanish bond spread up 1.3bps at 63.8bps/ Portuguese spread up 1.5bps at 59.8bps

EUROPE SUMMARY: Mixed Sterling Trades Ahead Of Sunday Deal 'Deadline'

Friday's options flow included:

- RXF1 177.50/176.50ps, bought for 9 in 1kRXG1 175.50 put, bought for 13 in 2k

- DUF1/DUG1 112.30/20ps spread, bought the Feb for 1.25 in 10k

- ERZ1 100.37p, bough for 1.5 in 2k

- 0RZ0 100.50/100.62/100.75c fly, sold at 8.75 and 8.5 in 6k

- 0LM1 99.875/99.75ps, sold at 2 in 8k

- LH1 100.12/100.25/100.37 call fly, bought for 1 in 2k

- LH1 100.00/100.125/100.25 call fly bought for 2 in 1.5k

- LM1 99.87/100.00/100.125 1x3x2 call fly sold at 0.25 in 11k (v 100.03)

- LZ1 100.99.99.875ps vs 100.375c, bought the ps for 0.75 in 3k

- LZ1 99.875/99.625ps, bought for 2 in 5k

- 2LF1 99.875p vs 0LF1 99.875p, bough the 2yr for 1.25 in 7.5k

- 2LH1 100c vs 0LH1 100c, sold 2yr at 0.5 in 4k

- 2LH1 99.75/99.50 put spread bought for up to 1.75 in 4k

FOREX: Crunch Time

Sterling had a poor finish to the week, falling against all others in G10 as markets gear for yet another self-imposed deadline for make-or-break trade deal negotiations on Sunday evening. Options markets have taken note and are pricing in a sizeable swing for GBP on Monday, indicating decent two way risk in GBP crosses. Nonetheless, it may come as no surprise that some see the negotiations going beyond this weekend, with the German foreign minister suggesting talks could extend through to next week.

Equities retreated into the Friday close, capping a negative week for stocks globally. Losses were muted, however, with the S&P 500 still well within range of the alltime highs posted midweek. This supported JPY throughout the Friday session, which rose against all others in G10.

Focus in the coming week turns to global central banks. Rate decisions are due from the US, UK, Norwegian, Swiss, Hungarian, Mexican central banks (among others), which should keep markets busy regardless.

Options Pricing a Sizeable Swing in GBP Monday

No surprise to see GBP implied vols surging further this morning, with the sharpest rise seen in the short-end. One week vols, naturally capturing the Sunday night deal deadline have risen north of 20 points, to the highest level since March's COVID crisis (although this pales in comparison to rates north of 50 points as the 2016 referendum results rolled in...).

- For options pricing for a Monday expiry after the deal deadline has passed, GBP/USD implied breakevens sit at just over 210 pips (sizeable, relative to a 60 pip breakeven for the same contract in EURUSD).

- Markets see a 24% implied probability of GBP/USD trading below 1.30 by the Monday close and a 19% probability of trading above 1.35.

FX OPTIONS: Expiries for Dec14 NY cut 1000ET (Source DTCC)

EUR/USD: $1.1900(E521mln), $1.2000(E1.1bln), $1.2050-60(E664mln), $1.2175(E860mln), $1.2240-50(E614mln)

USD/JPY: Y103.00-10($800mln), Y103.50-55($878mln), Y104.00($557mln), Y104.94-00($519mln), Y106.00($2.1bln)

GBP/USD: $1.3500(Gbp545mln), $1.3600(Gbp657mln)

EUR/GBP: Gbp0.8800-20(E540mln), Gbp0.9015-25(E564mln)

EUR/JPY: Y126.00(E606mln)

AUD/JPY: Y78.30-35(A$574mln)

USD/CAD: C$1.3300($692mln)

EQUITIES: Stocks Sag into Friday Close, Second Weekly Loss in Six

Equities sank into the Friday close, with the S&P500 coming off around 0.25% to record a negative week on Wall Street. Losses were muted, however, with alltime highs printed mid-week signalling consolidation rather than any turn in risk sentiment.

Energy and financials lagged, with the moderating crude price and firm outperformance earlier in the week largely responsible. Losses were stemmed in communication services and consumer staples, which managed to finish in the green.

The VIX picked up moderately from the mid-week lows, with Brexit and Washington dealmaking (or lack thereof) providing a boost, but this effect could fade fast headed into the holidays.

COMMODITIES: Oil, Metals Moderate Into Friday Close

After the week's sharp rally, WTI and Brent crude futures have moderated slightly but continue to hold close to the top-end of the recent range. Soft equity markets Friday are largely responsible for the pullback in commodity prices, with Brent futures dipping back below the $50/bbl mark.

Precious metals are seeing little support from soft risk sentiment early Friday, with spot gold still pinned between the 50- and 200-dma directional triggers. These levels lie at $1875.29 and $1809.67 respectively.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.