Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

HIGHLIGHTS

- MNI CHINA-RUSSIA: Foreign Ministers Meet As Germany Approves Export Of MiG-29s

- MNI US: Senate Labor Committee Hearing On Biden Labor Sec Nominee Julie Su April 20

- MNI WHEAT: Russia Warns That Black Sea Grain Deal May Not Be Extended

- ECB'S WUNSCH: MAY RATE DECISION BETWEEN 25 AND 50 BPS HIKE, Bbg

- GERMANY TO ALLOW POLAND EXPORT OF MIG-29 JETS TO UKRAINE, Bbg

US TSYS: Near Late Lows After Posting Strong Gains Post-PPI

- Treasury futures trading weaker but off lows after the bell, no obvious headline or block driver for the reversal. Treasury futures had rallied after PPI came out weaker than estimate: -0.5% vs. 0.0%, weekly claims higher than expected at 239K.

- The main takeaway is that PPI inflation has slowed more notably in the past two months, better reflecting the improvement in supply chain pressures although it hasn’t yet fully fed through to core CPI underlying goods.

- June 10Y futures marked session high of 116-03 by midmorning, 10Y yield low of 3.3681%, before retracing through the second half to 115-12.5 low and 3.4562% high yield. Curves maintained steeper profiles, however, as short end rates kept pace with the intermediates, 2s10s currently +4.905 at -52.444.

- Fed funds implied hike for May'23 held steady around 18.4bp, as well as Jun'23, while projected rate cuts later in the year have receded slightly from this morning's levels: Nov'23 cumulative -31.5bp to 4.511%, Dec'23 cumulative -49.5bp at 4.331. Fed Terminal currently at 5.01% in Jun'23.

- Friday focus: Fed Speak, Import/Export prices, Retail Sales, Industrial Production, Capacity Utilization and UofM sentiment.

SHORT TERM RATES

SOFR Benchmark Settlements:- 1M+0.00835 to4.88952

- 3M -0.00355 to 4.98632

- 6M -0.02473 to 4.96063

- 12M -0.04950 to 4.71602

US DOLLAR LIBOR: Latest settlements:

- O/N -0.00272 to 4.81214% (+0.00243 total last wk)

- 1M +0.00200 to 4.94771% (+0.04742 total last wk)

- 3M +0.00900 to 5.26029% (+0.06243/wk)*/**

- 6M -0.03586 to 5.30614% (-0.10186 total last wk)

- 12M -0.08072 to 5.28571% (-0.21701 total last wk)

- * Record Low 0.11413% on 9/12/21; ** New 16Y high: 5.25129% on 4/12/23

- Daily Effective Fed Funds Rate: 4.83% volume: $114B

- Daily Overnight Bank Funding Rate: 4.82% volume: $283B

- Secured Overnight Financing Rate (SOFR): 4.80%, $1.358T

- Broad General Collateral Rate (BGCR): 4.77%, $527B

- Tri-Party General Collateral Rate (TGCR): 4.77%, $523B

- (rate, volume levels reflect prior session)

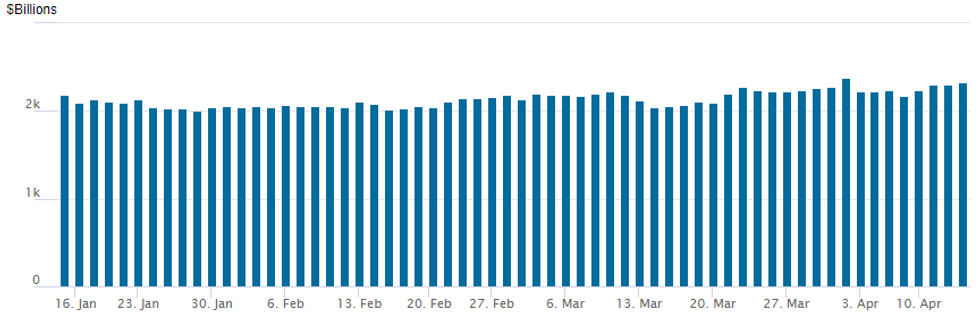

FED Reverse Repo Operation

NY Federal Reserve/MNI

NY Fed reverse repo usage climbs to $2,321.699B w/ 101 counterparties, compares to prior $2,303.862B. All-time record high of $2,553.716B reached December 30, 2022; high usage for 2023: $2,375.171B on Friday March 31, 2023

EURODOLLAR/SOFR/TREASURY OPTIONS SUMMARY

Mixed trade continued Thursday, better put focus in general on modest volumes, speculative focus on the next FOMC rate announcement on May 3 leaning toward another 25bp hike, particularly after underlying futures pared post-data gains. Salient trade includes:- SOFR Options:

- Block, 5,000 SFRZ3 94.87/95.12/95.87/96.12 iron condors, 15.0 ref 95.775

- over 3,000 SFRM3 94.81/94.93/95.06 put flys, 3.5 ref 95.08

- +10,000 SFRM3 95.06/95.18 call spds, 3.5

- Block, 5,000 SFRU3 94.37/94.50 put spds, 1.0 ref 95.415

- over 15,000 SFRJ3 95.00 straddles

- -10,000 SFRJ3 94.87/94.93/95.06/95.12 put condors, 4.25

- +5,000 SFRM3 95.06/95.18 call spds, 3.25

- 1,500 SFRK3 94.87/94.93/95.00 put flys, ref 95.045

- 5,000 SFRU3 94.68/94.93/95.37/95.62 iron condors

- 6,000 SFRN3 95.50 calls, ref 95.355

- 2,400 OQM3 95.62/96.25/96.75 broken put flys ref 96.575

- 2,000 SFRM3 95.12/95.25/95.37/95.50 put condors ref 95.06

- 2,000 OQK3 95.00/95.50/96.00 put flys, ref 96.585

- Treasury Options:

- over 6,900 FVK3 111 calls, 8

- 3,000 TYK3 112/119 combo

- over 3,300 TYK3 115 puts, 14 last

- 1,700 TYM 114/114.5 put spds

- 2,500 TUM3 102.75 puts, 12 ref 103-13.88

- 2,500 wk2 TY 115 puts, 3 ref 115-25.5

EGBs-GILTS CASH CLOSE: Twist Steepening As Hike Expectations Retrace

The German and UK curves modestly twist steepened Thursday, with the short end benefiting from a retracement in central bank tightening expectations.

- Yields hit a session low in mid-afternoon as markets digested a softer-than-expected US producer price report, but edged back toward opening levels as equities picked up some steam toward the close.

- ECB implied rate pricing hit a session low early on after a Reuters sources story pointing to the Governing Council hiking 25bp at the May meeting vs the 50bp floated by Holzmann on Weds, remaining steady thereafter (peak depo down 6bp on the day, BoE's -4bp).

- BoE Chief Econ Pill told an MNI event that the UK could see a positive demand shock amid a strong labor market, but remained ambiguous on the outlook for rate hikes, saying there is scope to do too much as well as too little.

- Periphery EGB spreads widened slightly, with Greece underperforming.

- Friday's docket includes final French and Spanish CPI, with BOE's Tenreyro and ECB's Nagel scheduled to speak.

Closing Yields / 10-Yr Periphery EGB Spreads To Germany

- Germany: The 2-Yr yield is down 1.7bps at 2.779%, 5-Yr is down 0.5bps at 2.392%, 10-Yr is up 0.2bps at 2.372%, and 30-Yr is up 1.7bps at 2.462%.

- UK: The 2-Yr yield is down 0.2bps at 3.517%, 5-Yr is up 0.1bps at 3.406%, 10-Yr is up 0.5bps at 3.575%, and 30-Yr is up 4.7bps at 3.942%.

- Italian BTP spread up 0.5bps at 185bps / Greek up 1.6bps at 189.4bps

EGB Options: Still Buying Euribor Put Flies

Thursday's Europe rates / bond options flow included:

- ERU3 96.50/96.00/95.25 broken put fly bought for 13.5 in 6k (also bought Wednesday for up to 12.75 in 12k)

- SFIU3 95.4/95.6/95.8c fly, bought for 2.75 in 2k

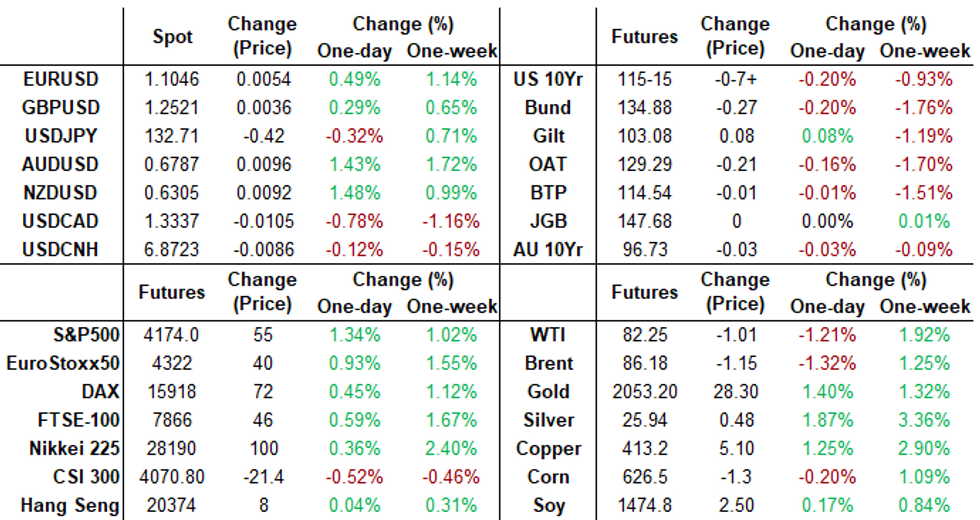

FX: Firmer Risk Sentiment Weighs Further On Greenback, AUD & NZD Rise Over 1.5%

- Below-expectation US data and a strong recovery for major equity indices on Thursday further weighed on the US dollar, prompting the DXY (-0.52%) to narrow the gap significantly with the year’s lows at 100.82. The firmer risk backdrop underpinned an impressive rally for the likes of AUD & NZD, while the Swiss Franc extended its most recent upward trend.

- For AUDUSD, an additional tailwind was firmer jobs data overnight, with both the employment change and the unemployment rate coming in better than expectations. The continued strength has seen the pair rise to a new seven-week high of 0.6797.

- On the tech side, AUDUSD has topped the 50-day EMA convincingly on Thursday amid the widespread greenback weakness. This works against the broader downtrend and key short-term resistance at the April 04 high has been pierced. Attention now turns to 0.6824, the Feb 24 high.

- CHF again trades well, with USD/CHF through to new YTD lows as well as breaching the February 2021 low at 0.8871. The pair was yet to hit technically oversold levels, however, today’s price action could tip the 30-day RSI below 30 for the first time since November.

- Elsewhere in G10, EUR/USD now sits north of the noted 1.1033 resistance, while GBP/USD has made a new trend high above the bull trigger at 1.2525.

- USDJPY traded poorly following the US data, falling over a big figure from 133.17 to 132.02 lows. Despite the renewed weakness, the slightly higher US yields and the grind higher for stocks has seen the pair recover around 70 pips of the moves as we approach the APAC crossover.

- US retail sales and UMich sentiment and inflation expectations data headline Friday’s docket to finish the week.

FX: Expiries for Apr14 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.0890-00(E2.2bln), $1.0950(E1.1bln), $1.1000(E1.8bln), $1.1050(E630mln)

- USD/JPY: Y130.00($1.2bln), Y132.00($910mln), Y133.00($661mln), Y134.00($602mln)

- NZD/USD: $0.6400(N$1.1bln)

- USD/CAD: C$1.3440-45($1.7bln)

- USD/CNY: Cny6.8000($503mln), Cny6.9000($914mln), Cny6.9050($514mln)

Late Equities Roundup: Nearing Resistance

- US stocks are quietly extending session in early afternoon trade: Dow Industrials (33,965.0 +316.1), SPX Eminis (4165.75 +46.75) and Nasdaq (12,150.4 +221.2) at the moment.

- No particular headline driver for the ongoing support other than carry-over positive tone regarding inflation following this mornings lower than expected PPI.

- After trading weaker in the first half of the week, Communication Services, Information Technology and Consumer Discretionary sectors are outperforming. Laggers: Utilities, Real Estate and Industrials.

- Nearing resistance again after S&P E-minis briefly traded above 4171.75 yesterday, the Apr 4 high. Current trend conditions are bullish - price has recently breached 4119.50, Mar 6 high, reinforcing a positive theme.

- The move higher has also resulted in a break of 4148.48, 76.4% of the Feb 2 - Mar 13 downleg. This signals scope for an extension to 4205.50, the Feb 16 high ahead of 4244.00, the Feb 2 high and a key M/T resistance.

E-MINI S&P (M3): Trend Needle Points North

- RES 4: 4244.00 High Feb 2 and a bull trigger

- RES 3: 4223.00 High Feb 14

- RES 2: 4205.50 High Feb 16

- RES 1: 4177.75 High Apr 12

- PRICE: 4151.50 @ 1220ET Apr 13

- SUP 1: 4083.19 20-day EMA

- SUP 2: 4056.44 50-day EMA

- SUP 3: 3980.75 Low Mar 28

- SUP 4: 3937.00 Low Mar 24

S&P E-minis briefly traded above 4171.75 yesterday, the Apr 4 high. Current trend conditions are bullish - price has recently breached 4119.50, Mar 6 high, reinforcing a positive theme. The move higher has also resulted in a break of 4148.48, 76.4% of the Feb 2 - Mar 13 downleg. This signals scope for an extension to 4205.50, the Feb 16 high ahead of 4244.00, the Feb 2 high and a key M/T resistance. Firm support lies at 4056.44, the 50-day EMA.

COMMODITIES: Gold Begins To Eye All-Time Highs Whilst Oil Retraces CPI Gains

- Crude oil has increasingly retraced a share of yesterday’s post-CPI gains, despite equities pushing higher and the dollar stepping lower again with the latter a repeat of yesterday’s favorable conditions for crude.

- Earlier, OPEC leaving its 2023 global oil demand growth forecasts unchanged at 2.3mln bpd and that OPEC cuts will cause a widening supply shortfall had little immediate impact on prices.

- WTI is -1.0% at $82.41, pulling back after coming close to key resistance at $83.53. Support remains at $79.00 (Apr 3 low).

- Brent is -1.2% at $86.31, having earlier nudged resistance at $87.49 (Apr 12 high) and stopped short of the key $88.35 (Jan 23 high). Support is seen at $83.50 (Apr 3 low).

- Gold is +1.3% at $2041.64 off a high of $2048.71 as the aforementioned weaker USD provided a strong support for the yellow metal. It cleared resistance at $2032.1 (Apr 5 high) and confirmed a resumption of the current uptrend, ultimately setting attention on the next key resistance at $2070.4 (Mar 8, 2022 high), just ahead of the all-time high of $2075.5 (Aug 7, 2020).

Friday Data Calendar

| Date | GMT/Local | Impact | Flag | Country | Event |

| 14/04/2023 | 0600/0800 | *** |  | SE | Inflation report |

| 14/04/2023 | 0645/0845 | *** |  | FR | HICP (f) |

| 14/04/2023 | 0700/0900 | *** |  | ES | HICP (f) |

| 14/04/2023 | - |  | EU | ECB Lagarde and Panetta in IMF/World Bank Spring Meetings | |

| 14/04/2023 | 1230/0830 | ** |  | CA | Monthly Survey of Manufacturing |

| 14/04/2023 | 1230/0830 | *** |  | US | Retail Sales |

| 14/04/2023 | 1230/0830 | ** | | US | Import/Export Price Index |

| 14/04/2023 | 1245/0845 | | US | Fed Governor Christopher Waller | |

| 14/04/2023 | 1300/0900 | * | | CA | CREA Existing Home Sales |

| 14/04/2023 | 1315/0915 | *** | | US | Industrial Production |

| 14/04/2023 | 1400/1000 | *** | | US | University of Michigan Sentiment Index (p) |

| 14/04/2023 | 1400/1000 | * | | US | Business Inventories |

| 14/04/2023 | 1600/1700 |  | UK | BOE Tenreyro Panellist at the IMF Meeting |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.