HIGHLIGHTS

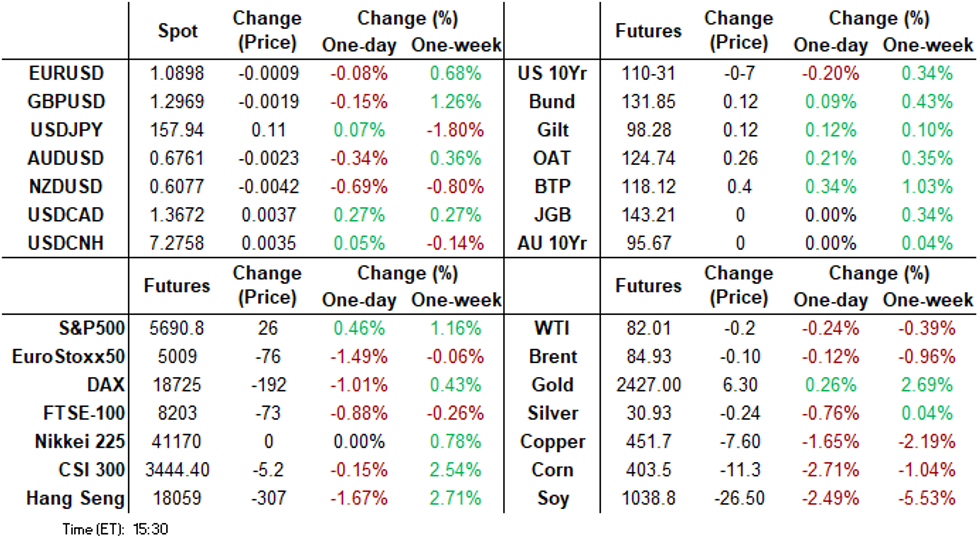

Treasuries look to finish mostly weaker Monday, curves twisting steeper as short end rates outperformed.

As a result, projected rate cut pricing through year end remains firm near 2.5x .25bp cuts by December.

Fed Chairman Powell interview: June inflation data lends Fed confidence on future rate cuts.

US TSYS: Curves Twist Steeper, Near Highs After Dovish Leaning Powell Interview

- Treasuries look to finish near session lows after gapping mildly higher at the start of Fed Chairman Powell's cordial interview with David Rubenstein at the Economic Club of DC earlier.

- While expressly stating he would not comment on markets, Treasury futures pare losses as Chairman Powell discusses the labor market where the Fed could react to an unexpected labor market weakening.

- Fed Chair Powell at a Q&A with the Economic Club of Washington, D.C. strikes a predictably dovish-leaning message in light of recent data, repeating previous comments that the labor market is back to roughly where it was pre-pandemic; for inflation, in Q2 we had "3 better readings" following June's reports.

- Sep'24 10Y futures extending top end of the session range to 111-06.5 (+0.5) but have scaled back to pre-interview levels at 110-30.5 (-7.5). Curves folding broadly steeper: 2s10s +4.052 at -23.017, 5s30s +3.158 at 32.372.

- Projected rate cut pricing into year end have gained vs. this morning's levels (*): July'24 at -6.5% w/ cumulative at -1.6bp at 5.313%, Sep'24 cumulative -27.5bp (-24.8bp), Nov'24 cumulative -44.1bp (-41.6bp), Dec'24 -65.8bp (-63.3bp).

- Focus turns to Tuesday's Retail Sales, Import/Export Prices, upcoming earnings from Bank of America, Charles Schwab, State Street and Morgan Stanley.

SOFR FIXES AND PRIOR SESSION REFERENCE RATES

SOFR Benchmark Settlements:

- 1M +0.00679 to 5.33459 (+0.00037 total last wk)

- 3M -0.00034 to 5.28577 (-0.02078 total last wk)

- 6M -0.01422 to 5.15058 (-0.06167 total last wk)

- 12M -0.02977 to 4.83577 (-0.13995 total last wk)

- Secured Overnight Financing Rate (SOFR): 5.34% (+0.00), volume: $1.900T

- Broad General Collateral Rate (BGCR): 5.32% (+0.00), volume: $774B

- Tri-Party General Collateral Rate (TGCR): 5.32% (+0.00), volume: $756B

- (rate, volume levels reflect prior session)

- Daily Effective Fed Funds Rate: 5.33% (+0.00), volume: $90B

- Daily Overnight Bank Funding Rate: 5.32% (+0.00), volume: $263B

FED Reverse Repo Operation

NY Federal Reserve/MNI

RRP usage inches up to $413.280B from $406.590B on Friday. Number of counterparties drops to 65 from 73 prior. Today's usage compares to $327.066B on Monday, April 15 -- the lowest level since mid-May 2021.

SOFR/TEASURY OPTION SUMMARY

Larger SOFR and Treasury option volume appeared mixed with several unwinds in call and put skew plays Monday as underlying futures bear steepened, short end outperforming. As a result, projected rate cut pricing into year end have gained vs. this morning's levels (*): July'24 at -6.5% w/ cumulative at -1.6bp at 5.313%, Sep'24 cumulative -27.5bp (-24.8bp), Nov'24 cumulative -44.1bp (-41.6bp), Dec'24 -65.8bp (-63.3bp). Salient flow includes:

SOFR Options:- +8,000 SFRZ4 94.87/95.00 put spds, 1..5 ref 95.38

- Block, 7,000 SFRQ4 95.12/95.31 call spds, 1.25 ref 94.975

- -10,000 SFRV4 95.37/95.50 call spds, 4.0 ref 95.38

- Block, 5,000 SFRZ4 94.87/95.37 call over risk reversals, 17.0 ref 95.37

- Block, +5,000 0QU4 96.25/96.50/96.75/97.00 call condors, 7.0 vs. 96.285/0.05%

- Block, 5,000 2QV4 96.37/96.87/97.37 call flys, 13.0 net ref 96.51

- Block, 5,000 SFRH5 95.50/95.75/96.00/96.25 call condors, 6.5 ref 95.725

- Block, -7,000 SFRU4 95.00 1.0 over SFRV4 95.43/95.56 call spds

- -25,000 SFRH5 95.50/95.75/95.81/96.00 broken call condors, 5.5

- -15,000 SFRH5 94.75/95.00/95.12/95.43 call condors, 6.0-6.25

- +5,000 SFRZ4 95.43/95.62 call spds, 4.5 vs. 95.35/0.13%

- -2,000 SFRZ4 94.87/95.37 strangle, 17.0 ref 95.355

- -10,000 SFRZ4 94.75/95.12 put spds , 4.75 ref 95.35

- +6,000 SFRZ4 95.25/0QZ4 96.75 call spds 2.75

- -20,000 SFRZ4 94.75 puts, 1.0 ref 95.34/0.07%

- Block/screen, 8,000 SFRU4 95.12/95.25 call spds 1.0

- +5,000 SFRH5 96.00/96.75 1x2 call spds, 4.25

- 2,000 SFRV4 95.12/95.31/95.37 broken put trees

- +3,500 SFRU4 94.87/94.93/95.00 call flys, 2.25 ref 94.945

- 4,000 0QU4 96.00/96.50 call spds vs. 3QU4 96.50/96.87 call spds

- 3,600 SFRH5 94.75 puts, 1.5 ref 95.735

- +5,000 SFRH5 96.00/96.75 1x2 call spds 4.25

- +18,500 SFRV4 95.12/95.25/95.31/95.43 call condors, 3.75 ref 95.345

- +30,000 wk1 TY 111.25 puts, 46 (expire Aug 2)

- +54,000 wk3 Wednesday FV 107 puts, 1 (expires this Wednesday)

- 2,600 TUU4 102.12/102.62 put spds, 15

- 6,600 TYU4 112 calls, 25 ref 111-02

- 7,500 TYV4 114 calls, 21 ref 111-14.5

- 2,500 USU4 116 puts, 37 ref 119-09

- +10,000 TYQ4 110 puts, 5 ref 111-03.5 to -04

- 2,000 TYU4 110.5/111.5 strangles ref 111-03

- 3,600 TYQ4 110.25 puts vs. 111/111.5 call spds 0.0 ref 110-29

- 1,900 TYV4 109 puts ref 111-10

EGBs-GILTS CASH CLOSE: Constructive Start To ECB Week

European government bonds strengthened across the board Monday.

- Core FI started on the front foot, faltering in late morning led by Bunds amid some confusion over news reports over increased funding in the 2024 German budget (which turned out not to be a new development).

- Overall though there was little in the way of European macro news flow/headlines to drive, with the general tone remaining positive following last Thursday's soft US inflation report.

- The UK curve bull steepened, with Germany's shifting in a similar direction but with outperformance in the 5Y segment.

- Periphery / semi-core EGB spreads tightened on the day despite weakness in equities, led by BTPs and OATS (-2bp on the day vs 10Y Bund).

- With a limited calendar of scheduled events Tuesday (including German ZEW), focus this week is on Wednesday's UK CPI release and Thursday's ECB decision.

Closing Yields / 10-Yr Periphery EGB Spreads To Germany

- Germany: The 2-Yr yield is down 2.4bps at 2.799%, 5-Yr is down 3bps at 2.445%, 10-Yr is down 2.4bps at 2.472%, and 30-Yr is down 2.3bps at 2.66%.

- UK: The 2-Yr yield is down 2.1bps at 4.065%, 5-Yr is down 0.9bps at 3.939%, 10-Yr is down 0.8bps at 4.101%, and 30-Yr is down 0.9bps at 4.606%.

- Italian BTP spread down 2.2bps at 127.5bps / Spanish down 0.3bps at 76.1bps

Euro Rate Upside Via Midcurve Monday

Monday's Europe rates/bond options flow included:

- ERZ4 97.12 calls 40K sold vs. 0RZ4 98.00/98.25 call spread, package trades at 1

- 0RZ4 98.00/98.50 cs bought for 4.25 in 5k

FOREX USDJPY Completes Round Trip Post-Powell, NZD Weakness Persists

- USDJPY has unsurprisingly posted the largest range across the majors on Monday, as volatility remains high in the aftermath of last week’s US data and supposed BOJ intervention. Chair Powell described the latest data as adding to the FOMC’s confidence, which prompted a momentary blip lower for the greenback.

- USDJPY trades close to unchanged around 157.90. The pair reached as low as 157.19 following Powell’s remarks, having printed an overnight high of 158.42 during the APAC session. Most notable support remains at 156.83, a Fibonacci retracement.

- NZD underperforms across G10, falling 0.57% against the dollar as weaker-than-expected China GDP weighs at the margin. The AU-NZ 2yr swap continues to tick higher, now back at November 2020 levels which continues to bolster the AUD/NZD rally, rising to a fresh cycle high of 1.1136.

- EURUSD tracks close to 1.0900 and 1.30 continues to cap the topside in GBPUSD, a level that would place cable at the highest level since July last year.

- Scandinavian FX underperforms, with USDNOK trading 0.95% higher on Monday. In similar vein, there were some notable laggards in the EM space such as MXN, dropping over 1% given its beta to Trump election odds and ZAR falling 1.5%.

- Eurozone Trade and German ZEW data crosses on Tuesday, before US retail sales and Canadian CPI highlight the economic calendar.

Late Equity Roundup: Energy, Financials Continue to Lead Gainers

- Stocks are firmer in late trade, well off first half highs amid steady profit taking over the last three hours after the Dow climb to a new record high of 40,342.22 earlier. S&P eminis and Nasdaq indexes still off Friday's highs. Currently, the DJIA up 257.15 points (0.64%) at 40256.48, S&P E-Minis up 24.75 points (0.44%) at 5690.25, Nasdaq up 78.3 points (0.4%) at 18477.32.

- Energy and Financial sector shares continue to lead gainers in late trade, equipment and services shares buoyed the former: Haliburton +5.19%, Schlumberger +4.63%, Baker Hughes +4.46%. Banks continue to buoy the Financial sector: Regions Financial +2.91%, JP Morgan +2.54%, M&T Bank +2.36%.

- Note, Wells and JPM rebounded after consolidating following last Friday's earnings. Blackrock and Goldman Sachs both announced early Monday, GS +1.85%, Blackrock +0.41%.

- Conversely, Utilities and Health Care sectors underperformed in late trade, electricity and independent power providers underperforming: AES Corp -9.26%, Centerpoint energy -6.83%, NextEra Energy -5.43%. Meanwhile, equipment and service providers weighed on the Health Care sector: Baxter -3.47%, DaVita -3.10%, Stryker -2.79%.

- Upcoming earnings: Bank of America, Charles Schwab, State Street and Morgan Stanley on Tuesday; Citizens Financial, US Bancorp, Discover Financial and Ally Financial on Wednesday; KeyCorp, M&T Bank and Blackstone on Thursday; Fifth Third, Regions Financial, Comerica, American Express and Huntington next Friday.

E-MINI S&P TECHS: (U4) Trend Needle Points North

- RES 4: 5764.00 3.50 proj of the Apr 19 - 29 - May 2 price swing

- RES 3: 5741.34 3.236 proj of the Apr 19 - 29 - May 2 price swing

- RES 2: 5713.31 3.236 proj of the Apr 19 - 29 - May 2 price swing

- RES 1: 5717.75 Intraday High Jul 15

- PRICE: 5689.50 @ 14:50 BST Jul 15

- SUP 1: 5569.65 20-day EMA

- SUP 2: 5502.75/5461.50 Low Jul 2 / 50-day EMA

- SUP 3: 5398.75 Low Jun 11

- SUP 4: 5267.75 Low May 31 and key support

The trend condition in S&P E-Minis is bullish and the contract is holding on to its recent gains. The continuation higher last week confirms a resumption of the uptrend and maintains the bullish sequence of higher highs and higher lows. Moving average studies are in a clear bull-mode set-up too and this continues to highlight positive market sentiment. Sights are on the 5713.31, a Fibonacci projection. Firm support is at 5569.65, the 20-day EMA.

COMMODITIES Crude Falls, Copper Drops After Soft Q2 Chinese GDP Data

- WTI is falling today as geopolitical risks are weighed against a stronger US dollar and concerns of weaker demand in China.

- WTI Aug 24 is down 0.3% at $81.9/bbl.

- For WTI futures, sights remain on $85.27, the Apr 12 high and a bull trigger. Initial firm support to watch is $80.07, the 50-day EMA.

- Meanwhile, Henry Hub has extended its losses during US hours and is on track for its lowest since May 3. The delayed return of Freeport LNG following the halt due to hurricane Beryl has added pressure.

- US Natgas Aug 24 is down 7.0% at $2.17/mmbtu.

- Spot gold is up 0.5% on the day at $2,424/oz, albeit off the $2,439.8 intra-day high, which was just $10 shy of the May 20 record high.

- Key resistance is at $2,450.1, the May 20 high, while initial support to watch lies at the 50-day EMA, at $2,339.3.

- Copper has fallen by 1.7% to $451/lb on Monday, unwinding Friday’s rebound, following the softer-than-expected Chinese GDP data.

- A bearish corrective cycle that started May 20, remains in play for now. A resumption of the bear leg would open $426.12, a Fibonacci retracement. Initial resistance to watch is $489.25, the May 29 high.

TUESDAY DATA CALENDAR

| Date | GMT/Local | Impact | Flag | Country | Event |

| 16/07/2024 | 0700/0900 |  | EU | ECB's De Guindos in ECONFIN meeting | |

| 16/07/2024 | 0800/1000 | ** | | EU | ECB Bank Lending Survey |

| 16/07/2024 | 0800/1000 | ** |  | IT | Italy Final HICP |

| 16/07/2024 | 0900/1100 | *** |  | DE | ZEW Current Conditions Index |

| 16/07/2024 | 0900/1100 | *** | | DE | ZEW Current Expectations Index |

| 16/07/2024 | 0900/1100 | * | | EU | Trade Balance |

| 16/07/2024 | 0900/1000 | ** |  | UK | Gilt Outright Auction Result |

| 16/07/2024 | 1215/0815 | ** |  | CA | CMHC Housing Starts |

| 16/07/2024 | 1230/0830 | ** |  | US | Import/Export Price Index |

| 16/07/2024 | 1230/0830 | *** | | CA | CPI |

| 16/07/2024 | 1230/0830 | *** | | US | Retail Sales |

| 16/07/2024 | 1255/0855 | ** | | US | Redbook Retail Sales Index |

| 16/07/2024 | 1400/1000 | * | | US | Business Inventories |

| 16/07/2024 | 1400/1000 | ** | | US | NAHB Home Builder Index |

| 16/07/2024 | 1530/1130 | * | | US | US Treasury Auction Result for Cash Management Bill |

| 16/07/2024 | 1845/1445 | | US | Fed Governor Adriana Kugler | |

| 17/07/2024 | 2245/1045 | *** |  | NZ | CPI inflation quarterly |