Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

- MNI ECB: Pres Lagarde: Labour Market Robust But Slowing, Growth Risks To Downside

- TSY SEC YELLEN SAYS INFLATION IS COMING `WELL UNDER CONTROL', Bbg

- CIA CHIEF TO NEGOTIATE FOR RELEASE OF HOSTAGES IN GAZA: WAPO

- MICROSOFT TO CUT 1,900 ACTIVISION BLIZZARD, XBOX STAFF bbg

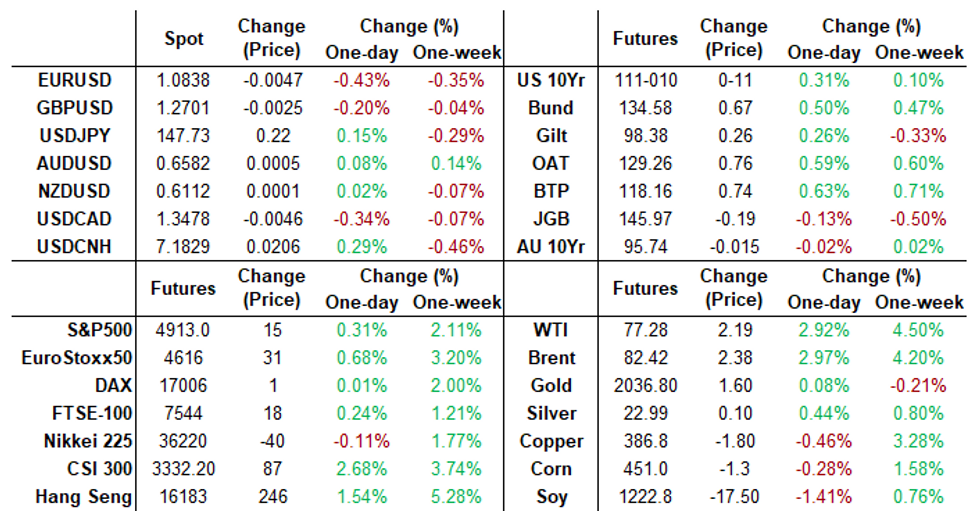

US TSYS 10Y Yield Back Near 4%

- After the knee-jerk sell-off reaction to 3.3% GDP, Treasury futures recovered, extended session highs in the last couple minutes, Mar'24 10Y taps 111-11.5 (+12.5), 10Y yield nears 4% to 4.0077% low.

- Reuters headlines providing lift for Treasury futures in late trade:

- ECB POLICYMAKERS OPEN TO START DISCUSSING FUTURE RATE CUTS IN MARCH IF DATA POINTS TO INFLATION HITTING 2% THIS YEAR: SOURCES

- ECB POLICYMAKERS SAY MARCH PIVOT WOULD PAVE WAY FOR RATE CUT MOST LIKELY IN JUNE: SOURCES - Reuters News

- Initial technical resistance at 111-21/112-26+ (20-day EMA / High Jan 12). Curves mildly flatter w/ 2s10s -0.706 at -21.281.

- Cross asset summary: Crude higher (WTI +2.17 at 77.26), Gold firmer (+4.83 at 2018.72), stocks firmer: SPX eminis +19.5 at 4919.5 - still off yesterday's contract high of 4933.25.

- Fast two reported earlier as Treasury futures broke upside AND downside range after Q4 advance GDP/core PCE, weekly claims data:

- GDP Price Index (1.5% vs. 2.2% est, 3.3% prior)

- GDP Annualized QoQ (3.3% vs. 2.0% est, 4.9% prior)

- Personal Consumption (2.8% vs. 2.5% est, 3.1% prior)

- Core PCE Price Index QoQ (2.0% vs. 2.0% est, 2.0% prior)

- Initial Jobless Claims (214k vs. 200k est, 189k prior rev)

- Continuing Claims (1.833M vs. 1.823M est, 1.806M prior)

FIXES AND PRIOR SESSION REFERENCE RATES

SOFR Benchmark Settlements:

- 1M -0.00005 to 5.33659 (+0.00065/wk)

- 3M -0.00446 to 5.31959 (+0.00441/wk)

- 6M -0.01571 to 5.17225 (+0.01292/wk)

- 12M -0.02724 to 4.81968 (+0.02119/wk)

- Secured Overnight Financing Rate (SOFR): 5.31% (+0.00), volume: $1.596T

- Broad General Collateral Rate (BGCR): 5.30% (+0.00), volume: $668B

- Tri-Party General Collateral Rate (TGCR): 5.30% (+0.00), volume: $661B

- (rate, volume levels reflect prior session)

- Daily Effective Fed Funds Rate: 5.33% (+0.00), volume: $96B

- Daily Overnight Bank Funding Rate: 5.31% (+0.00), volume: $263B

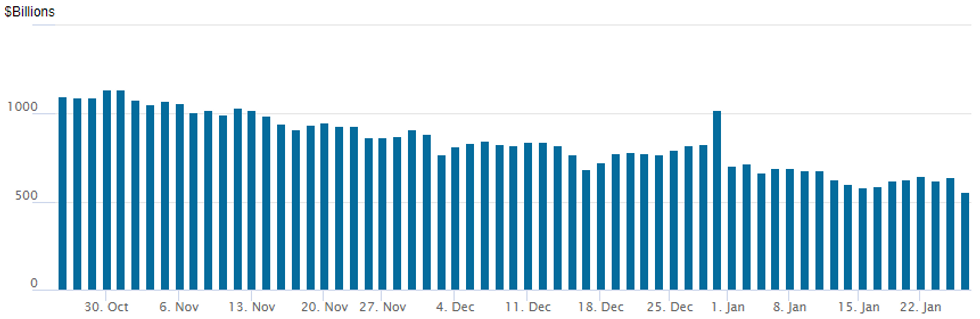

FED Reverse Repo Operation: New Cycle Low

NY Federal Reserve/MNI

- RRP usage falls to new cycle low of $557.687B vs. $639.560B Wednesday. Compares to $583.103B on Tuesday, January 16 - prior lowest level since mid-June 2021.

- Meanwhile, the number of counterparties at 82 vs. 83 Wednesday (65 Tuesday last Tuesday, the lowest since July 7, 2021)

SOFR/TREASURY OPTION SUMMARY

Mixed SOFR/Treasury options segued to better rate cut/upside call trading Thursday as underlying futures added to late session gains following ECB policymaker headlines that suggested a March rate pivot was still possible, depending on data. Rate cut projections for early 2024 gained slightly: January 2024 cumulative -.6bp at 5.323%, March 2024 chance of 25bp rate cut -49.4% vs. -40.7% this morning w/ cumulative of -13.0bp at 5.199%, May 2024 at -85.4% vs. 79.8% earlier w/ cumulative -34.3bp at 4.991%, June 2024 back over 100% at -102.1% vs. 97.5% earlier w/ cumulative -59.9bp at 4.730%. Fed terminal at 5.325% in Feb'24.

- SOFR Options:

- Block +5,000 SFRH4 95.12/95.37 call spds, 0.75 ref 94.87 at 0959:20ET

- Block +5,000 SFRZ4 97.75/98.00 call spds, 2.0 vs. 96.10/0.05% at 0957:51ET

- +30,000 SFRK4 95.50/95.75 1x2 call spds w/SFRK4 96.12/96.50 call spds, 0.75 net cr

- +5,000 0QH4 95.50/95.75/95.87/96.12 put condors, 5.75

- 6,000 SFRK4 94.87/95.06/95.02 put flys ref 95.285 to -.29

- Block, 5,000 SFRM4 95.56/95.62 call spds, 0.75 ref 94.865

- Block, 6,000 SFRM4 94.93/95.18/95.50/95.62 broken put condors, 0.0 net ref 95.265

- 2,000 SFRJ4 94.50/94.87/95.00/95.12 broken put condors ref 95.27

- 3,500 SFRJ4 95.25/95.50/96.00 broken call flys

- 2,000 SFRJ4 94.93/95.00/95.18 put flys

- 4,500 SFRH4 94.87/94.93/95.00 call flys ref 94.855

- 4,000 0QM4 97.00/97.50/97.75 broken call flys vs. 0QM4 95.75/96.00 put spds

- Treasury Options:

- +10,000 TYH4 114.5 calls, 5

- 2,500 FVH4 108/108.5/109 call flys vs. FVH 107.25/107.5/108 put flys

- Block, +14,800 TYG4 110.75 puts, 10 vs. 110-30.5/0.29%

- over 4,200 FVG4 108 calls, 3 last ref 107-20

- over 3,500 TYG4 111.5 calls, 5 last

- over 5,600 TYG4 110.75 puts, 7 last

- 2,000 TYG4 110.5/112 put spds, 59 ref 111-02

- 2,000 TYG4 110.25/110.5 put spds ref 110-30

EGBs-GILTS CASH CLOSE: Bull Steepening As ECB Cut Pushback Proves Limited

European yields fell Thursday amid a lack of hawkish surprises from the ECB and soft economic data on both sides of the Atlantic.

- While weaker-than-expected German IFO data early in the session didn't have much immediate market impact, it set the tone for a constructive session for core FI.

- Mixed US data released between the unsurprising ECB statement and the Lagarde press conference was met with a dovish reaction, with focus on a very soft quarterly inflation reading and a tick higher in jobless claims.

- As for the Lagarde presser, the lack of significant pushback against market rate cut pricing was marginally dovish: there are now 142bp of reductions expected this year, 12bp more than pre-US data/Lagarde, with implied probability of nearly 84% that the first cut will arrive by April (up from 60%).

- Curves finished bull steeper, led by a German short-end rally amid a rebound in ECB rate cut expectations.

- Periphery EGB spreads tightened on the more dovish monetary policy outlook, led by GGBs.

- While there is only largely 2nd tier European data out Friday, we hear from ECB policymakers including Simkus, Kazaks, and Vujcic, and get the ECB Survey of Professional Forecasters.

Closing Yields / 10-Yr Periphery EGB Spreads To Germany:

- Germany: The 2-Yr yield is down 9.2bps at 2.617%, 5-Yr is down 7bps at 2.187%, 10-Yr is down 5.2bps at 2.29%, and 30-Yr is down 2.3bps at 2.499%.

- UK: The 2-Yr yield is down 3.4bps at 4.385%, 5-Yr is down 4.2bps at 3.916%, 10-Yr is down 2.7bps at 3.983%, and 30-Yr is down 1.3bps at 4.594%.

- Italian BTP spread down 2.2bps at 153.7bps / Greek down 3.4bps at 100.2bps

FOREX EUR Slips As ECB Acknowledges Balanced Risks For Inflation

- Despite a broadly as expected ECB decision and press conference, and President Lagarde saying it was too early to discuss the timing of cuts, the Euro came under pressure on Thursday. EURUSD currently sits around 0.50% in the red, with the pair hovering just above the year’s lows as we approach the APAC crossover.

- 1.0900 capped the topside as the press conference began, however, an acknowledgement that wage pressures have started to ease saw a quick 50 pip jolt lower and a breaching of the tight overnight range. Comments on the rate cut debate being premature failed to garner any support, with the single currency keeping a downward bias for the majority of the US session.

- On the downside, a break of 1.0822, Tuesday’s and today’s lows, would resume the recent bearish theme. Lower US yields in the aftermath of the mixed US GDP data briefly supported the Yen, prompting EURJPY to breach yesterday’s lows below 160.00 and print 159.70 before stabilising.

- With major equities tilted into positive territory, the likes of EURAUD, EURNZD and especially EURCAD (-0.75%) are showing particular underperformance, with the latter further weighed by a 3% rally for crude futures.

- Despite the lower yields in the US, the USD index looks set to post a 0.35% advance on the session as markets turn their focus to PCE Core Deflator and US personal spending data on Friday. It is worth noting that the Bank of Japan minutes are scheduled overnight in Asia.

Late Equities Roundup: Energy Shares Buoyed By Crude Rally

- Off midmorning highs, stocks are still firmer in late trade, Energy and Communication Services sector shares outperforming. Currently, S&P E-Mini futures are up 4.75 points (0.1%) at 4902.75, Nasdaq down 22.8 points (-0.1%) at 15458.67, DJIA up 59.6 points (0.16%) at 37866.08.

- Leading gainers: Oil and gas shares buoyed the Energy sector in late trade as crude prices held gains (WTI +2.08 at 77.17): after beating earning expectations this morning, Valero climbed +2.94%, Kinder Morgan +2.34%, Hess Corp +2.10%. Telecom shares led Communication Services: ATT +2.07%, Verizon +2.06%, T-Mobile +0.20% -- is expected to announce after the close. Notable mention: IBM surged over 11% after announcing late Wednesday followed by multiple dealer upgrades today.

- Laggers: Consumer Discretionary and Health Care sectors underperformed, auto makers weighed down by Tesla -12.65% post-earnings, dour sales guidance preceded several downgrades. Ford, on the other hand traded +2.22%. Health Care weighed by provider shares: Humana -10.94%, United Health -5.69%, Molina Health -4.27%.

- Looking ahead: several earnings announcements expected after the close: Intel, Western Digital, Visa, Capital One, T-Mobile, L3Harris Technologies.

E-MINI S&P TECHS: (H4) Northbound

- RES 4: 5000.00 Psychological round number

- RES 3: 4982.62 1.50 proj of Nov 10 - Dec 1 - 7 price swing

- RES 2: 4952.45 1.382 proj of Nov 10 - Dec 1 - 7 price swing

- RES 1: 4933.25 High Jan 24

- PRICE: 4901.50 @ 1450 ET Jan 25

- SUP 1: 4813.28/4721.08 20- and 50-day EMA values

- SUP 2: 4702.00 Low Jan 5

- SUP 3: 4594.00 Low Nov 30

- SUP 4: 4550.75 Low Nov 16

The uptrend in S&P E-Minis remains intact and this week’s move higher reinforces current conditions. Resistance at 4841.50, the Dec 28 high has recently been cleared, confirming an extension of the price sequence of higher highs and higher lows. Moving average studies remain in a bull-mode condition, highlighting positive market sentiment. Sights are on 4952.45 next, a Fibonacci projection. Key support lies at 4721.08, the 50-day EMA.

COMMODITIES WTI Pushes To Late November Levels On Supply and Demand Factors

- WTI is headed for its highest close since late November, amid rising geopolitical risks, disrupted US output and Chinese stimulus plans.

- North Dakota oil production is disrupted by 130-180kbpd due to cold weather according to the pipeline authority on Thursday.

- Iran is under extreme sanctions by the US which is significantly bringing down Iran’s oil exports, Amos Hochstein, the US Energy Security Advisor said to Bloomberg.

- WTI is +2.7% at $77.13, piercing key resistance at $76.31 (Dec 26 high) and opening $77.48 (Fibo retrace of Sep 19 – Dec 13 bear leg) after which lies $79.56 (Nov 30 high).

- Brent is +2.6% at $82.15, also through a key resistance at $81.45 (Dec 26 high) and opening $84.22 (Nov 30 high).

- Gold is +0.2% at $2017.49, pulling back from earlier highs with some strength in the USD index to ultimately consolidate yesterday’s slide. The bear threat is still seen as present, with support at $2001.9 (Jan 17 low).

FRIDAY DATA CALENDAR

| Date | GMT/Local | Impact | Flag | Country | Event |

| 26/01/2024 | 0001/0001 | ** |  | UK | Gfk Monthly Consumer Confidence |

| 26/01/2024 | 0700/0800 | * |  | DE | GFK Consumer Climate |

| 26/01/2024 | 0700/0800 | ** |  | SE | Unemployment |

| 26/01/2024 | 0745/0845 | ** |  | FR | Consumer Sentiment |

| 26/01/2024 | 0900/1000 | ** |  | EU | M3 |

| 26/01/2024 | 1330/0830 | ** |  | US | Personal Income and Consumption |

| 26/01/2024 | 1500/1000 | ** | | US | NAR Pending Home Sales |

| 26/01/2024 | 1600/1100 |  | CA | Finance Dept monthly Fiscal Monitor (expected) | |

| 26/01/2024 | 1800/1300 | ** | | US | Baker Hughes Rig Count Overview - Weekly |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.