Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

HIGHLIGHTS

- MNI US ISM APR MANUF PRICES PAID INDEX 53.2

- JPMorgan to Acquire Failed Regional Bank First Republic, Bbg

- FDIC Releases Comprehensive Overview of Deposit Insurance System

- Second-Quarter GDP Growth Estimate Increased to 1.8% from 1.7% Prior

Key Links:MNI Fed Preview - May 2023: Analyst Outlook / MNI INTERVIEW: Fed Must Do More Or Accept Long Path To 2%-ISM / MNI FED WATCH: May Hike Brings Tightening Cycle Closer To End / US$ Credit Supply Pipeline

US TSYS: Curves Off Deeper Inversion

- Intermediate to long-end Treasury futures continue to gradually extend session lows, while yield curves bounce off deeper inversion after midday 2Y futures Block buy: 2s10s currently +1.978 at -56.670 vs. -64.490 low.

- This morning's data underscores a likely 25bp rate hike from the FOMC on Wednesday: April ISM Prices Paid climbs to 53.2, well over expected 49.0; S&P manufacturing PMI came out slightly lower than expected: 50.2 vs. 50.4 est, but gaining nonetheless vs. 49.2 in March.

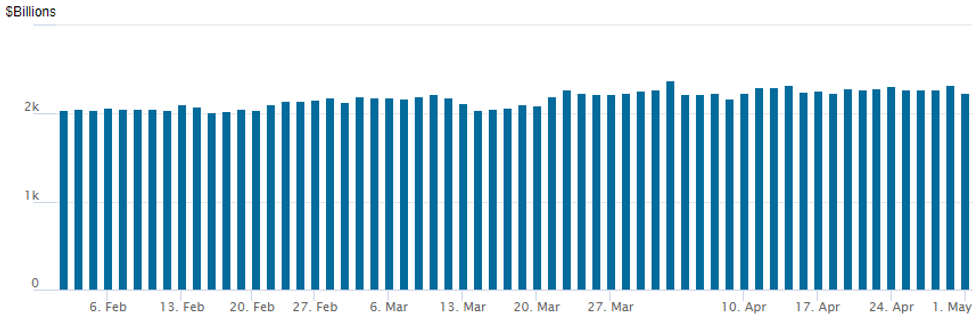

- We'd caution this is a volatile series that tends to track commodity prices as much as anything - so while important, it partly reflects a bounce from the sharp drop in commodity prices last year (Prices Paid bottomed at 39.4 in Dec when the 6-month % change in raw industrials and oil prices were dropping double digits - see chart). Though clearly, we're past the lows.

- Otherwise, US markets remain generally quiet, light volumes with much of Europe out for May Day bank holiday, TYM3 just over 750k at the moment.

SHORT TERM RATES

SOFR Benchmark Settlements:

- 1M +0.01517 to 5.03387 (+.04818 total last wk)

- 3M +0.00797 to 5.08929 (+.01357 total last wk)

- 6M +0.00931 to 5.08888 (-.00877 total last wk)

- 12M +0.01696 to 4.82604 (-.07339 total last wk)

- Daily Effective Fed Funds Rate: 4.83% volume: $113B

- Daily Overnight Bank Funding Rate: 4.81% volume: $259B

- Secured Overnight Financing Rate (SOFR): 4.81%, $1.378T

- Broad General Collateral Rate (BGCR): 4.79%, $541B

- Tri-Party General Collateral Rate (TGCR): 4.79%, $530B

- (rate, volume levels reflect prior session)

FED Reverse Repo Operation

NY Federal Reserve/MNI

NY Fed reverse repo usage falls back to $2,239.866B w/ 103 counterparties, compares to prior $2,325.479B. Compares to high usage for 2023: $2,375.171B on Friday March 31, 2023; all-time record high of $2,553.716B reached December 30, 2022.

SOFR/TREASURY OPTIONS SUMMARY

Light option volumes was due to most of Europe out for May-Day bank holiday Monday. Early SOFR Call structure buying ebbed in the second half while Jun'23 SOFR options saw a pick-up in limited downside put condors as a jump over 50.0 to 53.2 in April ISM Mfg PMI data, underscoring a likely 25bp rate hike this Wednesday.- SOFR Options:

- Block, +10,000 SFRM3 94.68/94.75/94.81/94.87 put condors, 0.75 ref 94.855

- +25,000 SFRM3 94.68/94.75/94.81/94.87 put condors, 0.5 ref 94.855 to -.86

- 2,000 SFRM3 94.93/95.12 call spds ref 94.89

- Block, +10,000 SFRZ3 96.50/97.50 call spds, 13.0 vs. 95.50/0.10%

- +2,000 SFRM3 97.00/97.12/99.50/99.62 call condors

- 1,000 SFRM3 94.75/95.00/95.12 broken put flys, ref 94.915

- 2,000 SFRN3 94.50/94.93/95.00/95.18 put condors ref 95.155

- Treasury Options:

- +4,000 USM 128 puts, 54 ref 130-02

- 2,100 TYM3 112.25 puts, 8 ref 114-30 to -30.5

- 2,500 FVM3 110.5/111.25 call spds ref 109-22 to -22.5

- 2,000 FVM3 112/113 call spds, 5.5 ref 109-25.5

- 3,000 TYM3 115.75/116.5 call spds ref 115-12

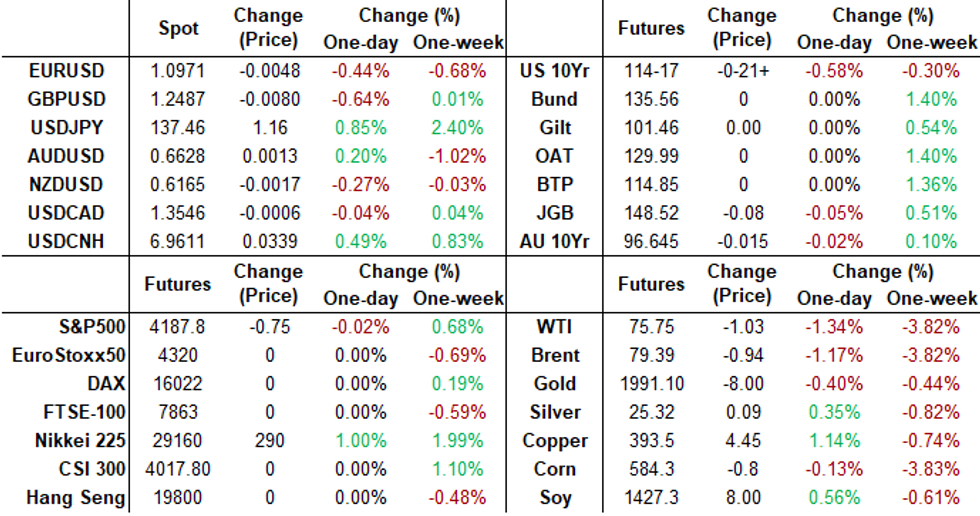

FOREX: EURJPY Prints 150.96 High, Highest Since 2008

- Moves in currency markets on Monday continue to be dominated by the Japanese Yen, comfortably the weakest performer in G10 since Friday’s BoJ Monetary Policy decision. EURJPY has extended its recent rally above the 150.00 handle with the early 150.03 session low confirming the pivot significance.

- Bear flattening in the US treasury curve, aided by some firmer US ISM data (particularly the prices paid component) is providing a positive backdrop for cross/yen and with it, EURJPY continues to register at the highest levels since 2008 after breaking above the 2014 highs last week.

- Price action has confirmed a resumption of the technical uptrend and cancels recent short-term bearish threats. The move higher signals scope for a climb towards 151.00 and 152.00, the 1.382 Fibonacci projection of the Mar 20 - 21 - Apr 6 price swing. Moving average studies remain in a bull mode position, highlighting the uptrend.

- The USD index has held a moderate upward bias on Monday, rising 0.34% as of writing and underpinned by the only notable data point on Monday. For USDJPY, 137 capped the topside for much of the session, however, price has since reached a fresh high of 137.26, further paving the way for 137.91, the Mar 8 high and a key resistance.

- The Australian dollar is the strongest performer on Monday, with a notable 1.2% advance for AUDJPY, rising to the best levels since March 7 just above the 91.00 handle. This comes in the face off some weaker China PMI data overnight, which in turn has weighed on the offshore Yuan, down 0.4% against the USD.

- Central banks in focus this week with the RBA meeting kicking the week off on Tuesday. Attention then inevitably turns to Wednesday’s FOMC decision and the ECB on Thursday, before the US employment data to finish the week.

EQUITIES: Paring Gains in Late Trade

- Stocks have trimmed second half gains, trading mildly weaker at the moment, still holding to a narrow session range. Currently, DJIA down 20.79 points (-0.06%) at 34076.09; - S&P E-Mini Future up 0.75 points (0.02%) at 4189 and Nasdaq down 15.3 points (-0.1%) at 12211.14.

- SPX futures drifted above key resistance of 4198.25 High Apr 18 earlier to 4204.00 high before retreating. A clear break of this level would confirm a resumption of the uptrend that started Mar 13 and open 4244.00, the Feb 2 high.

- On the downside, key short-term support has been defined at 4068.75, the Apr 26 low. A break would be bearish.

- Meanwhile, quarterly earnings cycle resumes after the close, salient stocks include: Stryker Corp, Community Health Systems, Invitation Homes Inc, Vornado Realty Trust, Transocean Ltd, ZoomInfo Technologies Inc, Arista Networks Inc, Avis Budget , Group Inc, SBA Communications Corp, MGM Resorts International, Credit Acceptance Corp and Diamondback Energy Inc.

COMMODITIES

- WTI Crude Oil (front-month) down $1.06 (-1.38%) at $75.71

- Gold is down $7.78 (-0.39%) at $1982.18

Tuesday Data Calendar

| Date | GMT/Local | Impact | Flag | Country | Event |

| 02/05/2023 | 2301/0001 | * |  | UK | BRC Monthly Shop Price Index |

| 02/05/2023 | 0430/1430 | *** |  | AU | RBA Rate Decision |

| 02/05/2023 | 0600/0800 | ** |  | DE | Retail Sales |

| 02/05/2023 | 0715/0915 | ** |  | ES | IHS Markit Manufacturing PMI (f) |

| 02/05/2023 | 0745/0945 | ** |  | IT | S&P Global Manufacturing PMI (f) |

| 02/05/2023 | 0750/0950 | ** |  | FR | IHS Markit Manufacturing PMI (f) |

| 02/05/2023 | 0755/0955 | ** | | DE | IHS Markit Manufacturing PMI (f) |

| 02/05/2023 | 0800/1000 | ** |  | EU | M3 |

| 02/05/2023 | 0800/1000 | ** | | EU | IHS Markit Manufacturing PMI (f) |

| 02/05/2023 | 0830/0930 | ** | | UK | S&P Global Manufacturing PMI (Final) |

| 02/05/2023 | 0900/1100 | *** | | EU | HICP (p) |

| 02/05/2023 | 0900/1100 | *** | | IT | HICP (p) |

| 02/05/2023 | 1000/1200 | ** | | IT | PPI |

| 02/05/2023 | 1255/0855 | ** |  | US | Redbook Retail Sales Index |

| 02/05/2023 | 1400/1000 | ** | | US | Factory New Orders |

| 02/05/2023 | 1400/1000 | ** | | US | JOLTS jobs opening level |

| 02/05/2023 | 1400/1000 | ** | | US | JOLTS quits Rate |

| 02/05/2023 | - | *** | | US | Domestic-Made Vehicle Sales |

| 02/05/2023 | 1530/1130 | * | | US | US Treasury Auction Result for Cash Management Bill |

| 03/05/2023 | 2245/1045 | *** |  | NZ | Quarterly Labor market data |

| 03/05/2023 | 2300/0900 | * | | AU | IHS Markit Final Australia Services PMI |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok