- Treasuries initially gapped higher as PCE Inflation less hawkish in light of Thursday's Q1 beat.

- Treasuries scaled back but remained well bid after a very strong Supercore rundown.

- Focus turns to next Wednesday's FOMC, followed by Friday's latest employment report.

US TSYS PCE Data Less Hawkish in Light of Thu's Q1 Beat, Supercore Tempers Bid

- Treasuries looked to finish mostly higher Friday, curves flatter with the short end mildly weaker (2s10s -3.478 at -33.043). Intermediates trade near the middle of this morning's wide post-data range, Jun'24 10Y +6.5 at 107-18 (107-09L/107-27.5H).

- Treasury futures trade higher after the latest PCE data comes out in-line to slightly higher -- deemed less hawkish in light of Thursday's Q1 beat:

- PCE Deflator MoM (0.3% vs. 0.3%), YoY (2.7% vs. 2.6% est, 2.5% prior)

- PCE Core Deflator MoM (0.3% vs. 0.3% est), YoY (2.8% vs. 2.7% est, 2.8% prior).

- Treasuries support receded after a very strong Supercore: 0.39% M/M in Mar after 0.19 (initial 0.18) in Feb and 0.75 (initial 0.66) in Jan).

- Meanwhile, Personal Income (0.5% vs. 0.5% est, 0.3% prior), Personal Spending (0.8% vs. 0.6% est, 0.8% prior), Real Personal Spending (0.5% vs. 0.3% est, 0.4% prior).

- Treasury futures held gains after the latest University of Michigan data: Sentiment (77.2 vs. 77.9 est), Current Conditions (79.0 vs. 79.3 prior), 1 Yr Inflation (3.2% vs. 3.1% prior), 5-10 Yr Inflation unchanged at 3.0% vs. 3.0% est.

- Focus turns to next week's FOMC policy annc on Wednesday, followed by the latest employment data next Friday.

SOFR FIXES AND PRIOR SESSION REFERENCE RATES

SOFR Benchmark Settlements:

- 1M -0.00253 to 5.31573 (-0.00117/wk)

- 3M +0.00463 to 5.32950 (+0.00310/wk)

- 6M +0.02018 to 5.31384 (+0.01094/wk)

- 12M +0.04658 to 5.24380 (+0.02929/wk)

- Secured Overnight Financing Rate (SOFR): 5.31% (+0.00), volume: $1.774T

- Broad General Collateral Rate (BGCR): 5.31% (+0.01), volume: $690B

- Tri-Party General Collateral Rate (TGCR): 5.31% (+0.01), volume: $681B

- (rate, volume levels reflect prior session)

- Daily Effective Fed Funds Rate: 5.33% (+0.00), volume: $89B

- Daily Overnight Bank Funding Rate: 5.32% (+0.00), volume: $264B

FED Reverse Repo Operation

NY Federal Reserve/MNI

- RRP usage inches up to $464.912B vs. $443.928B Thursday. Compares to $327.066B on Monday, April 15 -- the lowest level since mid-May 2021.

- Meanwhile, the latest number of counterparties inches up to 78 vs. 74 prior.

SOFR/TEASURY OPTION SUMMARY

SOFR and Treasury option trade remained mixed Friday, most accounts squared and pared ahead of the weekend with focus on next Wednesday's FOMC rate announcement. After gaining slightly post data, projected rate cut pricing held largely steady vs. late Thursday levels: May 2024 -2.6% w/ cumulative -0.6bp at 5.322%; June 2024 at -9.9% w/ cumulative rate cut -3.1bp at 5.298%. July'24 cumulative at -8.6bp, Sep'24 cumulative -18.1bp.

- SOFR Options:

- +4,000 SFRM4 94.93/95.25 call spds 1.0 ref 94.71

- +13,000 SFRZ4 96.00/97.00 call spds 5.5 ref 95.015

- -6,000 SFRU4 95.00/95.25/95.50 call flys, 1.75 vs. 94.845/0.10%

- +6,000 SFRU4 94.87/95.00/95.12/95.25 call condors, 1.875 ref 94.855

- Block, 5,000 SFRM4 94.81/94.93/95.00/95.12 call condors, 0.75 ref 94.741

- +15,000 SFRH4 94.43/94.56 put spds 2.75 ref 95.20

- -8,000 SFRZ4 94.68/94.81 put spds 5.0 ref 95.01

- +5,000 0QM4 96.50 calls 1.5 ref 95.345

- Block, 10,000 SFRM4 94.62 puts, 1.25 ref 94.71

- Block, -7,500 SFRM4 94.68/94.75 put spds 3.5 over 94.93/95.68 call spds ref 94.71

- -12,750 SFRQ4 94.87/94.93 call spds vs. 94.62/94.68 put spds ref 98.85

- 2,000 SFRU4 94.25/94.62 put spds ref 94.855

- Treasury Options: May options expire today

- 7,000 TUM4 101.5/101.75 put spds ref 101-14.38

- over 14,400 TYK4 107.5 calls, 9 last ref 107-14.5

- 1,700 FVK4 104.75 puts, 5 ref 104-25.75

- 3,900 TYK 107.25 puts, 4 ref 107-17

- 2,000 wk1 TY 107.75/108.25 call spds ref 107-14

- over 7,800 TYM4 106 puts 21 ref 107-16

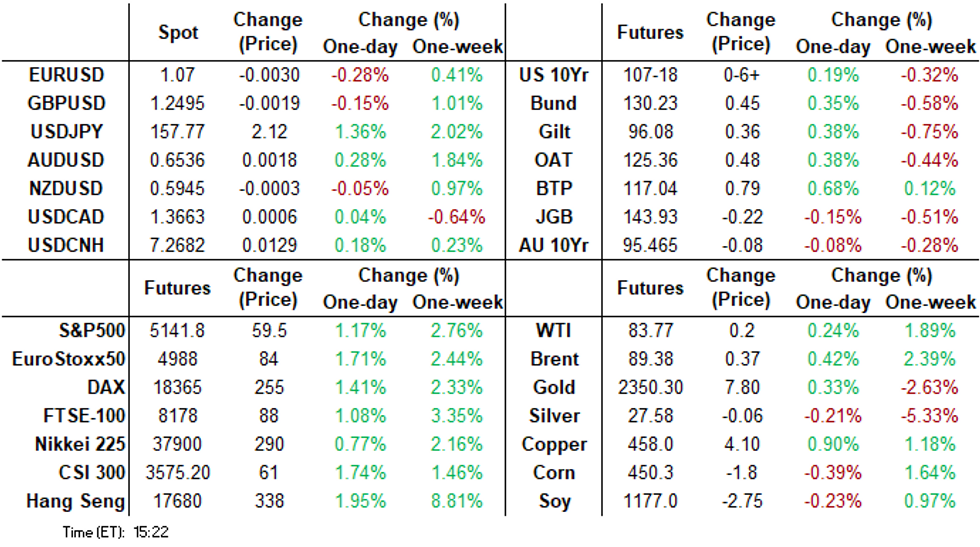

FOREX USDJPY Surges 1.3% To Fresh Cycle Highs

- With the Bank of Japan Governor seemingly playing down the Japanese Yen’s impact on inflation at today’s meeting, investors appear to have been given the green light to bolster their bearish views on the waning currency. Despite the usual two-way flurry in the aftermath of the post-decision press conference, USDJPY has resumed its strong upward bias and currently stands up 1.3% as we approach the weekend close.

- USDJPY highs for the session have been 157.79 at typing, with multiple topside targets being breached on Friday. Above here, the next notable level is 158.38, the 2.382 projection of the Feb 1 - 13 - Mar 8 price swing.

- With USDJPY leading the charge, the broader greenback found some support across US hours, with EURUSD and GBPUSD briefly slipping below Thursday’s lows.

- The USD index has risen 0.4% and despite some mixed reaction in the direct aftermath of the data, stronger-than-expected US core PCE figures may have bolstered the dollar bid.

- GBPUSD’s move higher this week was allowing an oversold condition to unwind, with trend conditions remaining bearish. A resumption of weakness would open 1.2266, the Nov 14 2023 low. Resistance to watch is 1.2583, the 50-day EMA.

- Equities have traded with a positive tone, keeping the Australian dollar as a relative outperformer with AUDUSD tracking around +0.20%. Both NZD and CAD sit mid-range, ~0.10% in the red against the dollar.

- German and Spanish CPI data kick off next week’s economic data calendar on Monday, with China PMIs highlighting Tuesday’s docket.

Late Equities Roundup: Interactive Media, Chip Stocks Lead Gainers

- Stocks continue to see-saw higher late Friday, profit taking/position squaring ahead of the weekend knocks S&P Eminis off 5146.50 recent high -- the best level since Middle East tensions triggered risk-off sentiment on April 15. Currently, DJIA is up 189.68 points (0.5%) at 38276.64, S&P E-Minis up 52 points (1.02%) at 5134.5, Nasdaq up 309.4 points (2%) at 15921.94.

- Leading gainers: Recovering from better sell interest yesterday, Communication Services and Information Technology sectors continued to outperform in late trade: Google surged +9.65%, while AT&T, Verizon and Comcast gained +1.45%-1.55%. Chip stocks continued to extend gains for the fifth day running: Nvidia +5.91%, Teradyne +5.17%, KLA Corp +5.13%.

- Laggers: Energy and Utility sectors continued to underperform, oil equipment and services shares weighed on the former: Phillips66 -3.50%, Exxon Mobil -2.24%, Pioneer Natural Resources -1.63%. Utilities weighed down by electricity and multi-energy shares: Xcel Energy -1.47%, American Electric -1.36%, Eversource Energy -1.07%.

- Expected corporate earnings announcements surge early next week:

- Monday: Domino's Pizza, ON Semiconductor, SBA Communications;

- Tuesday: Coca-Cola, Molson Coors, Sirius XM, McDonalds, Corning, PACCAR, Martin Marietta Materials, 3M, American Tower, GE Health, Sysco, Eli Lilly, PayPal Holdings, Archer-Daniels-Midland, Eaton Corp, Stryker, Prudential Fncl, ONEOK, Boston Properties, Diamondback Energy, Public Storage, Pinterest, Amazon, Starbucks, Advanced Micro Designs, Super Micro Computer.

E-MINI S&P TECHS: (M4) Short-Term Key Resistance Remains Intact For Now

- RES 4: 5333.50 High Apr 1 and the bull trigger

- RES 3: 5285.00 High Apr 10

- RES 2: 5213.25 High Apr 15

- RES 1: 5146.50 Intra-day high Apr 26

- PRICE: 5138.00 @ 1435 ET Apr 26

- SUP 1: 4963.50 Low Apr 19

- SUP 2: 4907.57 50.0% retracement of the Oct 27 ‘23 - Apr 1 bull leg

- SUP 3: 4863.75 Low Jan 19

- SUP 4: 4799.50 Low Jan 17

The short-term trend condition in S&P E-Minis remains bearish and the latest recovery appears - for now - to be a correction. Last week’s bearish extension reinforced current short-term conditions. The contract has recently cleared the 50-day EMA, signaling scope for a continuation lower. Sights are on 4907.57 next, a Fibonacci retracement. Firm resistance is 5138.90, the 20-day EMA. A clear break of the average would signal a possible reversal.

COMMODITIES WTI Crude, Spot Gold Edge Higher

- Oil prices have gained slightly on Friday, supporting an overall crude recovery this week driven on supply/demand fundamentals, while a Middle East instability premium lingers and Ukraine drone strikes continue on Russian infrastructure.

- WTI Jun 24 is up 0.4% at $83.9/bbl today, taking the weekly gain to 2.1%.

- WTI futures have recovered from their recent lows and price continues to trade above key short-term support at $81.14, the 50-day EMA. On the upside, key resistance and the bull trigger has been defined at $86.97, the Apr 12 high.

- Spot gold has edged up by 0.3% to $2,340/oz on Friday, leaving the yellow metal 2.2% lower on the week, which would be the first weekly loss in six.

- From a technical perspective, gold is in consolidation mode. Having pierced the 20-day EMA this week, this highlights the start of a possible corrective cycle. A continuation lower would signal scope for an extension towards $2229.4, the 50-day EMA.

- Meanwhile, copper is up by another 0.8% at $457/lb, having earlier in the session hit a new two-year high.

- Supply side concerns are continuing to fuel prices, highlighted by Codelco today which reported a decline in quarterly output.

MONDAY DATA CALENDAR

| Date | GMT/Local | Impact | Flag | Country | Event |

| 29/04/2024 | 0600/0800 | ** |  | SE | Retail Sales |

| 29/04/2024 | 0700/0900 | *** |  | ES | HICP (p) |

| 29/04/2024 | 0800/1000 | *** |  | DE | North Rhine Westphalia CPI |

| 29/04/2024 | 0800/1000 | *** | | DE | Bavaria CPI |

| 29/04/2024 | 0900/1100 | ** |  | EU | EZ Economic Sentiment Indicator |

| 29/04/2024 | 0900/1100 | * | | EU | Consumer Confidence, Industrial Sentiment |

| 29/04/2024 | 1200/1400 | *** | | DE | HICP (p) |

| 29/04/2024 | 1430/1030 | ** |  | US | Dallas Fed manufacturing survey |

| 29/04/2024 | 1530/1130 | * | | US | US Treasury Auction Result for 13 Week Bill |

| 29/04/2024 | 1530/1130 | * | | US | US Treasury Auction Result for 26 Week Bill |