Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

EXECUTIVE SUMMARY

- FED: Powell: SLR Exemption Up For Public Comment "Soon"

- MNI BRIEF: Biden, EU Leaders Set Up Mar 25 Video Summit

- BOC WILL END LIQUIDITY FACILITIES IN COMING WEEKS

- MERKEL IMPOSES EASTER LOCKDOWN, EXTENDS CURBS, Bbg

- NETHERLANDS EXTENDS LOCKDOWN UNTIL APRIL 20, RUTTE SAYS, Bbg

- ASTRAZENECA MAY HAVE GIVEN OUTDATED DETAILS ON COVID VACCINE, Bbg

US

FED: SLR question to Powell, whether the temporary exclusion to Tsys/Reserves helped banks provide credit to the economy over the past year.

- Says they threw "the kitchen sink" at the problems facing the economy a year ago, so hard to say what impact SLR exemption alone had.

- Says the Fed expects to put something out for comment "relatively soon", will have a transparent public process over this issue.

- Powell says that due to the substantial increase in reserves and Tsys, the leverage ratio is rapidly becoming the binding constraint from a capital standpoint, that wasn't the Fed's intention at the beginning.

- The latter is interesting because it suggests the Fed leadership may push for exemption of reserves, as has been suggested by some analysts.

- The joint call, to start at 1945GMT, will be a chance to share views, Michel said via Twiter, adding it was "time to rebuild our transatlantic alliance."

- According to a White House statement released Tuesday, the President will engage with leaders bout his desire "to revitalize U.S.-EU relations." Other topics will include working together to combat the pandemic, climate change, and trade. He will also discuss "shared foreign policy interests, including China and Russia."

CANADA

BOC: Bank of Canada Deputy Governor Toni Gravelle said Tuesday any tapering of QE would be done in slow steps, and would not signal any change in the outlook for the policy interest rate to remain at 0.25% until 2023.

- Slowing down purchases of at least CAD4 billion a week of federal bonds can be done without removing monetary stimulus, by stabilizing the size of the bond portfolio and re-investing the proceeds of maturing assets, Gravelle said in the text of a speech.

- "We would be easing our foot off the accelerator, not hitting the brakes," he said. For more see MNI Policy main wire at 1316ET.

OVERNIGHT DATA

- US Q4 CURRENT ACCOUNT GAP -$188.5

- US Q3 CURRENT ACCOUNT REVISED TO -$180.9

- The U.S. current acct deficit widened by $7.6 billion, or 4.2%, to -$188.5 billion in Q4, Bureau of Economic Analysis reported Tue, mainly reflects an expanded deficit on goods and reduced surplus on services.

- The Q3 deficit was revised to -$180.9 billion (prev -$178.5 billion). The current account deficit in 2020 widened by 34.8% to -$647.2 billion or 3.1% of current dollar GDP, up from 2.2% in 2019

- US FEB NEW HOME SALES -18.2% TO 0.775M SAAR

- US JAN NEW HOME SALES REVISED TO 0.948M SAAR

- US MAR PHILADELPHIA FED NONMFG INDEX 38.6

MARKETS SNAPSHOT

Key late session market levels- DJIA down 339.73 points (-1.04%) at 32391.57

- S&P E-Mini Future down 33.5 points (-0.85%) at 3896.25

- Nasdaq down 152 points (-1.1%) at 13223.85

- US 10-Yr yield is down 7.2 bps at 1.6224%

- US Jun 10Y are up 15.5/32 at 132-1

- EURUSD down 0.0082 (-0.69%) at 1.1851

- USDJPY down 0.24 (-0.22%) at 108.61

- Gold is down $11.33 (-0.65%) at $1727.56

- EuroStoxx 50 down 6.82 points (-0.18%) at 3827.02

- FTSE 100 down 26.91 points (-0.4%) at 6699.19

- German DAX up 4.81 points (0.03%) at 14662.02

- French CAC 40 down 23.18 points (-0.39%) at 5945.3

US TYS SUMMARY: Springtime Indoors

The overnight risk-off tone spurred on by pick-up in extended or renewed lockdowns in Europe continued through the US Session -- accelerating into the NY rates close:deferring re-opening hopes weighed on stock indexes (hotel, travel shares hit hard), ESM1 extending session lows, while Tsys neared late overnight highs into the close.

- US Data support for rates: new home sales fell: -18.2% TO 0.775M SAAR; U.S. current acct deficit widened by $7.6B, +4.2%, to -$188.5B in Q4, reflects expanded deficit on goods and reduced surplus on services. USD gained on European headlines: MERKEL IMPOSES EASTER LOCKDOWN, EXTENDS CURBS; NETHERLANDS EXTENDS LOCKDOWN UNTIL APRIL 20, RUTTE SAYS; ASTRAZENECA MAY HAVE GIVEN OUTDATED DETAILS ON COVID VACCINE, Bbg.

- Yield curves bull flattened, long end made continued to rally after the bell, short end anchored on 2Y issuance: US Tsy $60B 2Y Note (91282CBU4): draws 0.152% high yield (0.119% last month) in-line w/ 0.152% WI, bid/cover 2.54 vs. 2.44 previous.

- Heavy Fed funds sales -30k FFJ1, 99.935 to 99.93; -27k FFH1, 99.93.

- Tone change in Eurodollar options accelerating, more constant and varied upside call buying, liquidation/unwinds put positions.

- The 2-Yr yield is unchanged at 0.1472%, 5-Yr is down 3.7bps at 0.8254%, 10-Yr is down 5.6bps at 1.6382%, and 30-Yr is down 4.6bps at 2.3529%.

US TSY FUTURES CLOSE:

- 3M10Y -8.259, 160.44 (L: 160.44 / H: 168.293)

- 2Y10Y -7.174, 147.159 (L: 146.983 / H: 154.865)

- 2Y30Y -6.094, 218.539 (L: 218.306 / H: 225.187)

- 5Y30Y -1.605, 151.791 (L: 151.009 / H: 154.268)

- Current futures levels:

- Jun 2Y up 0.25/32 at 110-12.5 (L: 110-12 / H: 110-12.875)

- Jun 5Y up 6.5/32 at 123-28.5 (L: 123-20.75 / H: 123-29)

- Jun 10Y up 16.5/32 at 132-2 (L: 131-14 / H: 132-02.5)

- Jun 30Y up 38/32 at 156-14 (L: 154-28 / H: 156-15)

- Jun Ultra 30Y up 51/32 at 184-11 (L: 181-30 / H: 184-13)

US EURODOLLAR FUTURES CLOSE:

- Jun 21 +0.005 at 99.835

- Sep 21 steady at 99.815

- Dec 21 +0.015 at 99.750

- Mar 22 +0.005 at 99.785

- Red Pack (Jun 22-Mar 23) +0.005 to +0.020

- Green Pack (Jun 23-Mar 24) +0.025 to +0.050

- Blue Pack (Jun 24-Mar 25) +0.065 to +0.080

- Gold Pack (Jun 25-Mar 26) +0.080

Short Term Rates

US DOLLAR LIBOR: Latest settles:

- O/N +0.00025 at 0.07688% (+0.00000/wk)

- 1 Month +0.00125 to 0.10863% (+0.00025/wk)

- 3 Month +0.01013 to 0.20063% (+0.00375/wk) (Record Low of 0.17525% on 2/19/21)

- 6 Month +0.00125 to 0.20538% (+0.00300/wk)

- 1 Year +0.00313 to 0.27938% (+0.00313/wk)

- Daily Effective Fed Funds Rate: 0.07% volume: $68B

- Daily Overnight Bank Funding Rate: 0.07%, volume: $241B

- Secured Overnight Financing Rate (SOFR): 0.01%, $869B

- Broad General Collateral Rate (BGCR): 0.01%, $358B

- Tri-Party General Collateral Rate (TGCR): 0.01%, $332B

- (rate, volume levels reflect prior session)

- TIPS 7.5Y-30Y, $1.199B accepted vs. $1.665B submission

- Next scheduled purchases:

- Wed 3/24 1010-1030ET: Tsy 2.25Y-4.5Y, appr $8.825B

- Thu 3/25 1010-1030ET: Tsy 20Y-30Y, appr $1.750B

- Fri 3/26 No buy operation

PIPELINE: Nomura, Santander Launched

- Date $MM Issuer (Priced *, Launch #)

- 03/23 $1.75B *Rentenbank 5Y +3

- 03/23 $1B *OMERS Finance Trust 5Y +18

- 03/23 $3.25B #Nomura $1.25B 5Y +105, 7Y +120, 10Y +130

- 03/23 $2.25B #Banco Santander $1.5B 5Y +103, $750M 10Y +133

- 03/23 $Benchmark Northern States Power WNG 10Y, 31Y

- 03/23 $Benchmark ISDB (Islamic Development Bank) 5Y Sukuk +39a

FOREX: Dented Sentiment Prompts AUD/USD to Resume Downleg

- A risk-off feel was evident from the European open, with growth and risk-proxies including NZD and AUD flagging in favour of USD and JPY. There was no specific catalyst for the risk-off, but a confluence of factors from lockdown extensions in the Eurozone, heightened vaccine protectionism and concern over New Zealand's tempering of house price growth that weighed from the off.

- The downtick in risk sentiment as well as the NZD resulted in AUD/USD resuming the downleg from the February high, narrowing the gap with early March lows as well as the 100-dma support at 0.7610.

- Greenback strength put the USD index on track for a test of the March highs at 92.503. A break above here opens the 200-dma resistance crossing at 92.672.

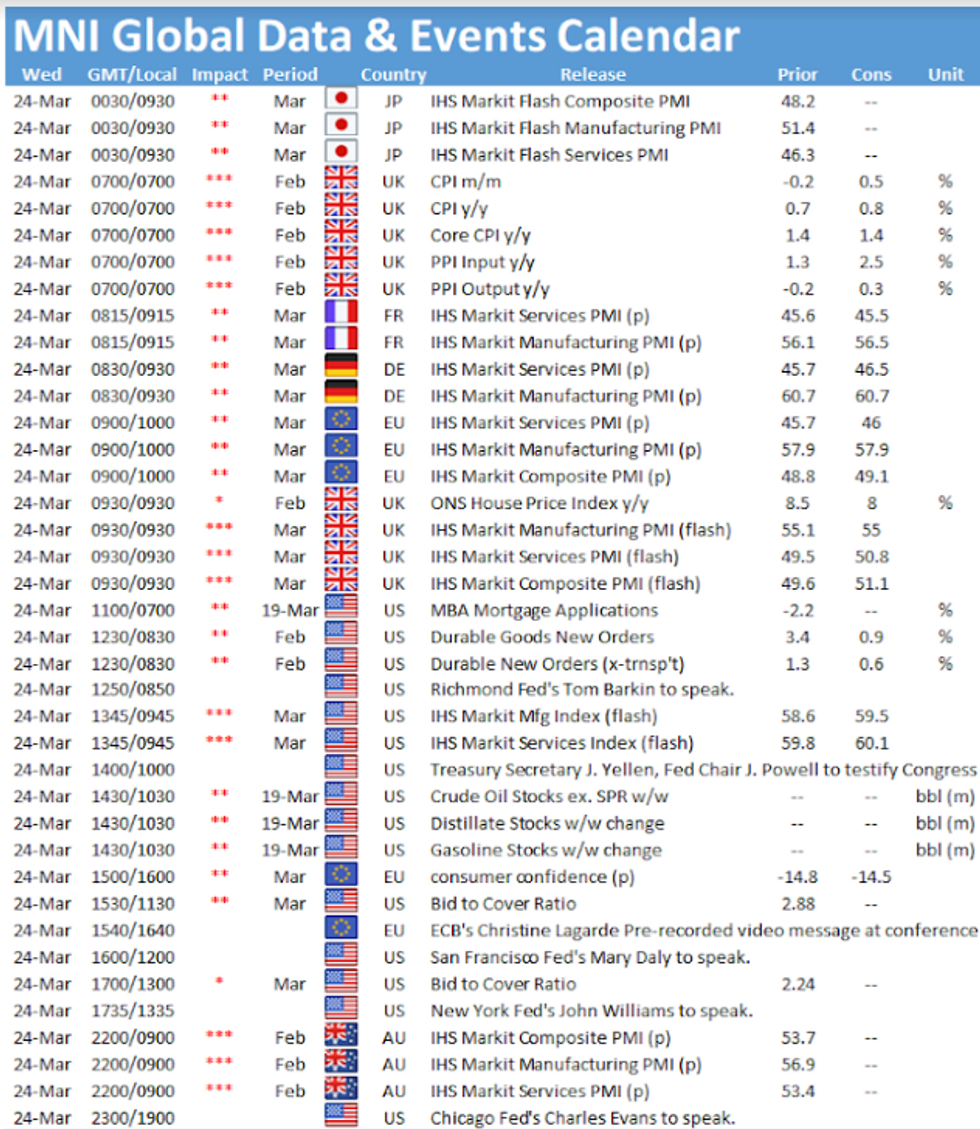

- UK inflation and prelim March Eurozone & UK PMI data take focus Wednesday. Most metrics are seen broadly inline with February's turnout, indicating continued modest growth across manufacturing, but a still flagging services sector. ECB's Lagarde speaks, but on the topic of climate change, not policy.

- From the US, durable goods orders and speeches from Fed's Barkin, Powell, Williams, Daly and Evans are due.

EGBs-GILTS CASH CLOSE: Lockdown Concerns

Core FI rallied throughout the day with a prevailing risk-off tone globally, with European COVID/lockdown concerns continuing to mount. Germany's announcement of a strict Easter lockdown was a focal point overnight, while the UK-EU vaccine export debate simmered.

- Gilts outperformed Bunds; periphery spreads tightened slightly after earlier widening, with a sizeable rally in the afternoon. Weekly ECB PEPP purchase data show only E0.9bln of redemptions last week, broadly in line w expectations.

- Issuance highlight was E13bn total of EU SURE dual-tranche 5Y/25Y via syndication. Germany sells E4bn of Bund Wednesday, while the UK sells linkers.

- UK jobs data was a little better than expected, with earnings in line. Looking forward to Weds, the scheduled highlight is flash March PMIs.

Closing yields/10-Yr Spreads to Bunds:

- Germany: The 2-Yr yield is down 0.9bps at -0.709%, 5-Yr is down 1.6bps at -0.67%, 10-Yr is down 3bps at -0.341%, and 30-Yr is down 3.4bps at 0.231%.

- UK: The 2-Yr yield is down 2.8bps at 0.046%, 5-Yr is down 4bps at 0.33%, 10-Yr is down 5.1bps at 0.763%, and 30-Yr is down 5.3bps at 1.288%.

- Italian BTP spread down 1.5bps at 94.3bps / Spanish spread down 1.5bps at 63.4bps

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.