Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

EXECUTIVE SUMMARY

- INFRASTRUCTURE DEAL REACHED BY BIDEN, BIPARTISAN SENATE GROUP - bbg

- BULLARD: NOT SURE WE HAVE LONG WAYS TO GO ON JOBS MANDATE, Bbg

- BULLARD: NOT SURE FED NEEDS TO BE IN MORTGAGE SECURITIES MARKET, bbg

- KAPLAN REPEATS HE'D LIKE FED TO TAPER SOONER RATHER THAN LATER, Bbg

- Kaplan: Paring Stimulus Now May Reduce Risk of More Aggressive Shift Later, DJ

- Former NY Fed President Bill Dudley:

- DUDLEY SAYS HE THINKS FED WILL BE 'PRETTY PATIENT' HERE

- DUDLEY: DON'T PUT TOO MUCH WEIGHT ON WHAT ONE FED PRESIDENT SAY

- BOE LEAVES RATES UNCHANGED AT 0.1%

- BOE LEAVES TOTAL QE AT GBP895 BILLION (GILTS 875B, CORP 20B)

- Surprise Bank of Mexico .25bp rate hike from 4.0% to 4.25%

US TSY SUMMARY: Frmr NY Fed Dudley: Don't Focus To Much on One Fed Pres

After some light two way after a flurry of mixed data (higher initial/lower continuing claims, better revisions on durables spurred some selling), Tsys extended highs before trimming gains -- kicking off a session of see-saw trade. Focus turned to half-dozen Fed speakers on the day, and final leg Tsy supply: $62B 7Y note.- Fed-speak really didn't break any new ground -- largely repeating already voiced opinions. Former NY Fed pres Bill Dudley did weigh in, however, suggesting the "FED WILL BE 'PRETTY PATIENT' HERE" and not to "PUT TOO MUCH WEIGHT ON WHAT ONE FED PRESIDENT SAY."

- No reacts in rates, but lent to some interest in reading at least: bipartisan infrastructure agreement reached, and Mexico hiked rates .25 to 4.25%.

- Decent Tsy auction: $62B 7Y note (91282CCH2) auction trades through with high yield of 1.264% vs. 1.267% WI. Tsys holding off session highs so far -- little reaction. Bid-to-cover: 2.36x vs. 2.26x 5 month avg, Indirect take-up of 59.97 well over the 5 month average of 55.19% but well shy of Jan's 64.09%. Primary dealer take-up 18.69% well below 25.23% 5 month avg (compares to February's >1Y high of 39.80%.) Direct take-up climbs to 21.34 vs. 19.53% 5M avg. The next 7Y auction is tentatively scheduled for July 29.

- The 2-Yr yield is up 0.4bps at 0.2661%, 5-Yr is up 2.4bps at 0.9054%, 10-Yr is up 0.2bps at 1.4868%, and 30-Yr is down 1.1bps at 2.0974%.

OVERNIGHT DATA

US Q1 GDP +6.4%

US JOBLESS CLAIMS -7K TO 411K IN JUN 19 WK

US PREV JOBLESS CLAIMS REVISED TO 418K IN JUN 12 WK

US CONTINUING CLAIMS -0.144M to 3.390M IN JUN 12 WK

US MAY DURABLE NEW ORDERS +2.3%; EX-TRANSPORTATION +0.3%

US APR DURABLE GDS NEW ORDERS REV TO -0.8%

US MAY NONDEF CAP GDS ORDERS EX-AIR -0.1% V APR +2.7%

US MAY ADVANCE INTL TRADE BALANCE -$88.1 B VS APR -$85.7B

US MAY ADVANCE WHOLESALE INVENTORIES +1.1%, $707.5B VS APR $699.8B

US MAY ADVANCE RETAIL INVENTORIES -0.8%, $598.3B VS APR $603.1B

U.S. WEEKLY LANGER CONSUMER COMFORT INDEX AT 56.9 VS 56.2

MARKETS SNAPSHOT

Key late session market levels:

- DJIA up 350.34 points (1.03%) at 34225.54

- S&P E-Mini Future up 27.5 points (0.65%) at 4259

- Nasdaq up 101.1 points (0.7%) at 14373.7

- US 10-Yr yield is up 0.2 bps at 1.4868%

- US Sep 10Y are down 1/32 at 132-5

- EURUSD up 0.0007 (0.06%) at 1.1933

- USDJPY down 0.1 (-0.09%) at 110.86

- WTI Crude Oil (front-month) up $0.14 (0.19%) at $73.22

- Gold is down $2.24 (-0.13%) at $1776.44

European bourses closing levels:

- EuroStoxx 50 up 46.49 points (1.14%) at 4122.43

- FTSE 100 up 35.91 points (0.51%) at 7109.97

- German DAX up 132.84 points (0.86%) at 15589.23

- French CAC 40 up 80.08 points (1.22%) at 6631.15

US TSY FUTURES CLOSE

- 3M10Y +0.081, 143.783 (L: 142.176 / H: 145.309)

- 2Y10Y -0.057, 122.048 (L: 121.201 / H: 123.18)

- 2Y30Y -1.28, 183.069 (L: 181.573 / H: 185.822)

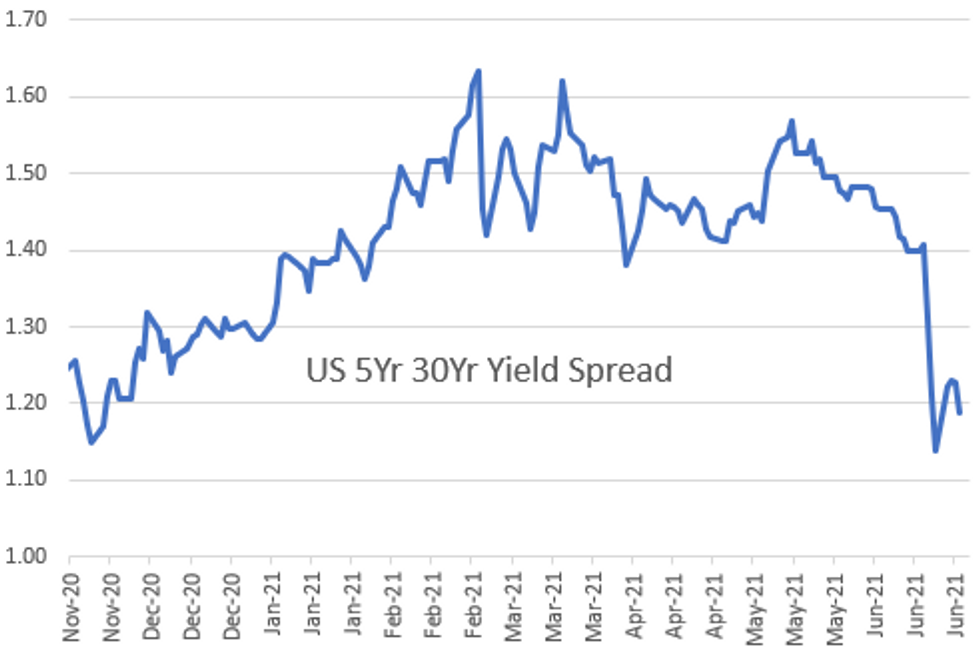

- 5Y30Y -3.134, 119.171 (L: 117.676 / H: 122.862)

- Current futures levels:

- Sep 2Y down 0.5/32 at 110-3.875 (L: 110-03.5 / H: 110-04.875)

- Sep 5Y down 1.5/32 at 123-9.5 (L: 123-08.25 / H: 123-13.25)

- Sep 10Y down 1/32 at 132-5 (L: 132-01 / H: 132-09)

- Sep 30Y up 2/32 at 159-27 (L: 159-12 / H: 160-02)

- Sep Ultra 30Y up 16/32 at 191-17 (L: 190-10 / H: 192-02)

US EURODOLLAR FUTURES CLOSE

- Sep 21 -0.005 at 99.855

- Dec 21 -0.005 at 99.785

- Mar 22 -0.005 at 99.790

- Jun 22 -0.010 at 99.710

- Red Pack (Sep 22-Jun 23) -0.015 to -0.01

- Green Pack (Sep 23-Jun 24) -0.015 to -0.01

- Blue Pack (Sep 24-Jun 25) -0.01 to steady

- Gold Pack (Sep 25-Jun 26) steady to +0.005

SHORT TERM RATES

US DOLLAR LIBOR: Latest Settles

- O/N -0.00025 at 0.08500% (+0.00450/wk)

- 1 Month +0.00350 to 0.09500% (+0.00400/wk)

- 3 Month -0.00125 to 0.14600% (+0.01112/wk) ** (New Record Low: 0.11800% on 6/14)

- 6 Month +0.00587 to 0.16525% (+0.00900/wk)

- 1 Year +0.00413 to 0.24763% (+0.00750/wk)

- Daily Effective Fed Funds Rate: 0.10% volume: $71B

- Daily Overnight Bank Funding Rate: 0.08% volume: $261B

- Secured Overnight Financing Rate (SOFR): 0.05%, $835B

- Broad General Collateral Rate (BGCR): 0.05%, $348B

- Tri-Party General Collateral Rate (TGCR): 0.05%, $325B

- (rate, volume levels reflect prior session)

- Tsy 22.5Y-30Y, $2.001B accepted vs. $4.631B submission

- Next scheduled purchase:

- Fri 6/25 1010-1030ET: Tsy 2.25Y-4.5Y, appr $8.425B

FED: Repo and Reverse Repo Operations

NY Fed reverse repo usage makes another new record high of $813.573B from 73 counterparties. Compares to Tue's record of $791.605B -- continued knock-on effect of FOMC's IOER technical adjustment to 0.15% from 0.10%.

MONTH-END EXTENSION: PRELIMINARY Barclays/Bbg Extension Estimates for US

PRELIMINARY forecast summary compared to avg increase for prior year and same time in 2020. TIPS 0.01Y; US Gov infl-linked -0.4Y.

| Indices | Estimate | 1Y Avg Incr | Last Year |

| US Tsys | 0.08 | 0.09 | 0.09 |

| Agencies | 0.11 | 0.04 | 0.06 |

| Credit | 0.05 | 0.12 | 0.09 |

| Govt/Credit | 0.07 | 0.10 | 0.09 |

| MBS | 0.11 | 0.06 | 0.08 |

| Aggregate | 0.08 | 0.09 | 0.09 |

| Long Gov/Cr | 0.07 | 0.09 | 0.12 |

| Iterm Credit | 0.07 | 0.10 | 0.10 |

| Interm Gov | 0.09 | 0.08 | 0.07 |

| Interm Gov/Cr | 0.08 | 0.09 | 0.08 |

| High Yield | 0.07 | 0.11 | 0.09 |

PIPELINE: Issuance Slow-Down

Only $3.8B high-grade corporate issuance to price Thursday- Date $MM Issuer (Priced *, Launch #)

- 06/24 $1.8B #Centene Corp 7Y +2.45%

- 06/24 $1.5B #Enbridge $1B 12Y +105, $00M 30Y +130

- 06/24 $500M #Athene Global Funding 5Y +72

EGBs-GILTS CASH CLOSE: BoE Not Hawkish Enough For Gilt Bears

Gilts outperformed on BoE day, with the Bank defying those who had positioned for a hawkish surprise.

- The BoE decision was in line with expectations (no change in policy, 8-1 vote to maintain QE policy, with the departing Haldane dissenting). Gilts rallied, and with Bunds stalling, the UK/ German spread is now at tightest levels since February.

- Periphery spreads tightened slightly, led by BTPs (which had underperformed Wednesday).

- French business confidence and German IFO data exceeded expectations.

- The only supply was Italy selling E6bln of new 7Y CCTeu floater via syndication. Tomorrow they sell E3.75B of short-term BTP and BTPei.

German/UK Yields And 10-Yr Spreads To Germany

- Germany: The 2-Yr yield is up 0.2bps at -0.651%, 5-Yr is down 0.1bps at -0.569%, 10-Yr is down 0.7bps at -0.185%, and 30-Yr is down 0.2bps at 0.306%.

- UK: The 2-Yr yield is down 1.6bps at 0.073%, 5-Yr is down 3bps at 0.354%, 10-Yr is down 3.6bps at 0.744%, and 30-Yr is down 3.5bps at 1.245%.

- Italian BTP spread down 2bps at 105.3bps /Spanish down 1.1bps at 61.7bps

FOREX: Muted Action in G10 FX, GBP Softer Following BOE

- G10 FX broadly held narrow ranges on Thursday. Initial greenback weakness overall was pared approaching the London WMR fix, leaving the dollar index unchanged from Wednesday's close.

- GBPUSD was sold down below 1.39 following the Bank of England decision and statement. It said growing inflation would surpass 3% as the UK economy reopens, but the climb further above its 2% target would only be "temporary". There are little signs in the minutes or statement that the MPC is considering an early end to QE, potentially weighing on Sterling, currently down 0.31%.

- For cable, our technical team still see a bearish threat present with GBPUSD trading through the 100-DMA, reinforcing current negative conditions. Scope is seen for an extension lower towards 1.3717, Apr 14 low.

- The strongest performers were SEK and NOK, firming roughly 0.35% with the latter benefitting from oil prices continuing to consolidate gains, following the recent strong rally.

- Emerging market currency indices continued to unwind the post FOMC losses, with notable moves in MXN (+1.28%), BRL (+1.14%) and RUB (+0.56%). The JPMorgan EM CCY index rose 0.35%.

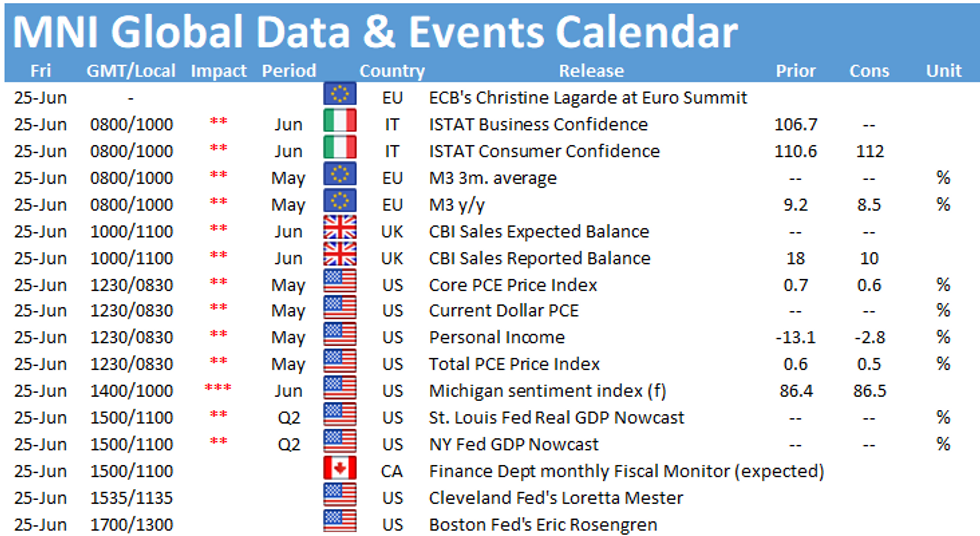

- The main data point for Friday will be the US PCE and personal income/spending figures for May, followed by Uni of Michigan Sentiment data to close out the week.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.