Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

EXECUTIVE SUMMARY

- MNI: Fed's Daly Sees Year-End Taper, 2022 Rate Hike Unlikely

- MNI: Supply Bottlenecks Lasting Longer Than Expected-Sintra

- MNI: Fed's Harker Sees Rate Liftoff As Early As End-2022

- MNI FED: Philly's Harker Looks For "Boring" Taper

- US: Schumer: Senate Could Take Action On CR As Early As Today

- MNI INSIGHT: BOE Clarifies Tightening Strategy, Focus On Rates

- FED'S POWELL: BIGGEST RISKS TO STABILITY ARE CYBER ATTACKS, STRUCTURAL ISSUES IN MARKETS AND CLIMATE CHANGE, Rtrs

- PELOSI: HOUSE PLANS TO VOTE ON DEBT LIMIT TODAY, Bbg

US

FED: San Francisco Fed President Mary Daly said Wednesday the economy will build the substantial progress needed to scale back asset purchases by the end of this year, while conditions for raising near-zero interest rates will likely remain out of reach through 2022.

- Tapering would just be "dialing back on the amount of accommodation we are adding to the economy," and the Fed would still be providing "tremendous support" to the recovery, she told reporters after a speech. Daly is an FOMC voter this year. For more see MNI Policy main wire at 1515ET.

FED: Inflation expectations appear stable but warrant careful monitoring as lingering supply constraints worsen price increases associated with the reopening of economies, the heads of the Federal Reserve, ECB and BOC said Wednesday.

- "The current inflation spike is really a consequence of supply constraints meeting very strong demand and that's all associated with the reopening of the economy, which is a process that has a beginning, middle and end," Fed Chair Jay Powell told the ECB's Sintra conference.

- "If it lasts long enough, will it start changing the way people think about inflation? We do not see evidence of that now. If we were to see sustained higher inflation and that becomes a concern we will certainly use our tools to make sure inflation is consistent with our goal." For more see MNI Policy main wire at 1241ET.

FED: Philly's Harker Looks For "Boring" Taper; The title of Philadelphia Fed Pres Harker's speech today is "Economic Outlook: Cautious Optimism" nicely sums up his outlook.

- His current rate view: "I wouldn't expect any hikes to interest rates until late next year or early 2023" is the same as his comment pre-Sept FOMC. And at that point he said his rate forecast hadn't changed since either the March or June dot plots. So pretty consistent and looks unlikely to change unless something dramatic happens.

- On tapering: time "soon" to "slowly ... methodically... boringly" pare back asset purchases.

- Overall, Harker's somewhere in the middle of the FOMC hawk-dove spectrum, probably leaning slightly hawkish, but doesn't appear to want tapering or rate liftoff to happen too quickly.

- He added that "it will soon be time" to begin to wind down the USD120 billion monthly asset purchase program, as QE kept markets functioning during the crisis but "aren't doing much -- or anything -- to ameliorate" labor shortages.

- "After we taper our asset purchases, we can begin to think about raising the federal funds rate. But I wouldn't expect any hikes to interest rates until late next year or early 2023," he said in remarks prepared for a virtual meeting of the Risk Management Association of Philadelphia.

- The CR would avoid a gov't shutdown and would likely carry significant bipartisan support, with Senate Republicans happy with the separation of gov't funding from legislation seeking to suspend/raise the debt ceiling.

- Schumer also states that Democrats are 'working on a way to prevent a default on US debt'. Senate Republicans pushing Dems to vote through debt ceiling hike via reconciliation (which would pass with 50 votes rather than 60, meaning no GOP senators would have to vote in favor).

UK

BOE: Bank of England Governor Andrew Bailey has clarified the Monetary Policy Committee's majority view of its new tightening strategy, stressing that interest rates should be the BOE's tightening tool after two members called for quantitative easing to be ended first.

- The MPC's September minutes and a speech by Bailey several days later have led market observers to bring forward expectations of a rate hike, with the governor saying that an increase in Bank Rate would, if needed, come before the end of the current asset purchase program in December. For more see MNI Policy main wire at 0956ET.

OVERNIGHT DATA

US NAR AUG PENDING HOME SALES INDEX 119.5 V 110.5 IN JUL; +8.1% vs. +1.3% est

MARKET SNAPSHOT

Key late session market levels:

- DJIA up 269.25 points (0.79%) at 34552.59

- S&P E-Mini Future up 29.75 points (0.68%) at 4369.75

- Nasdaq up 61.4 points (0.4%) at 14589.97

- US 10-Yr yield is up 0.7 bps at 1.5444%

- US Dec 10Y are down 0.5/32 at 131-14.5

- EURUSD down 0.008 (-0.68%) at 1.1603

- USDJPY up 0.5 (0.45%) at 112

- WTI Crude Oil (front-month) down $0.34 (-0.45%) at $74.87

- Gold is down $8.48 (-0.49%) at $1725.48

- EuroStoxx 50 up 21.4 points (0.53%) at 4080.22

- FTSE 100 up 80.06 points (1.14%) at 7108.16

- German DAX up 116.71 points (0.77%) at 15365.27

- French CAC 40 up 54.3 points (0.83%) at 6560.8

US TSYS: Early Bond Bid Evaporates, US$ Climbs Back To Nov 2020 levels

Rates finish mixed, yield curves reversed early flattening as long end support continued to evaporate after August pending home sales beat expectations 119.5 vs. 110.5 in Jul: +8.1% vs. +1.3% est.- Equities held modest gains, while USD climbed to Nov 2020 lvl -- historical tie-in to election just coincidence. Steady climb on same underlying catalyst behind curve steepening: Fed decision prompting markets to price in sooner, steeper policy normalization.

- No Market reaction on more or less consensus policy remarks as Philly Fed Pres Harker (non voter) penciling in first Covid-era interest rate increase for late next year or early 2023, after QE tapering is complete. Harker added that "it will soon be time" to begin to wind down the USD120B monthly asset purchase program, as QE kept markets functioning during the crisis but "aren't doing much -- or anything -- to ameliorate" labor shortages.

- SF Fed Daly sees by the end of this year, while conditions for raising near-zero interest rates will likely remain out of reach through 2022.

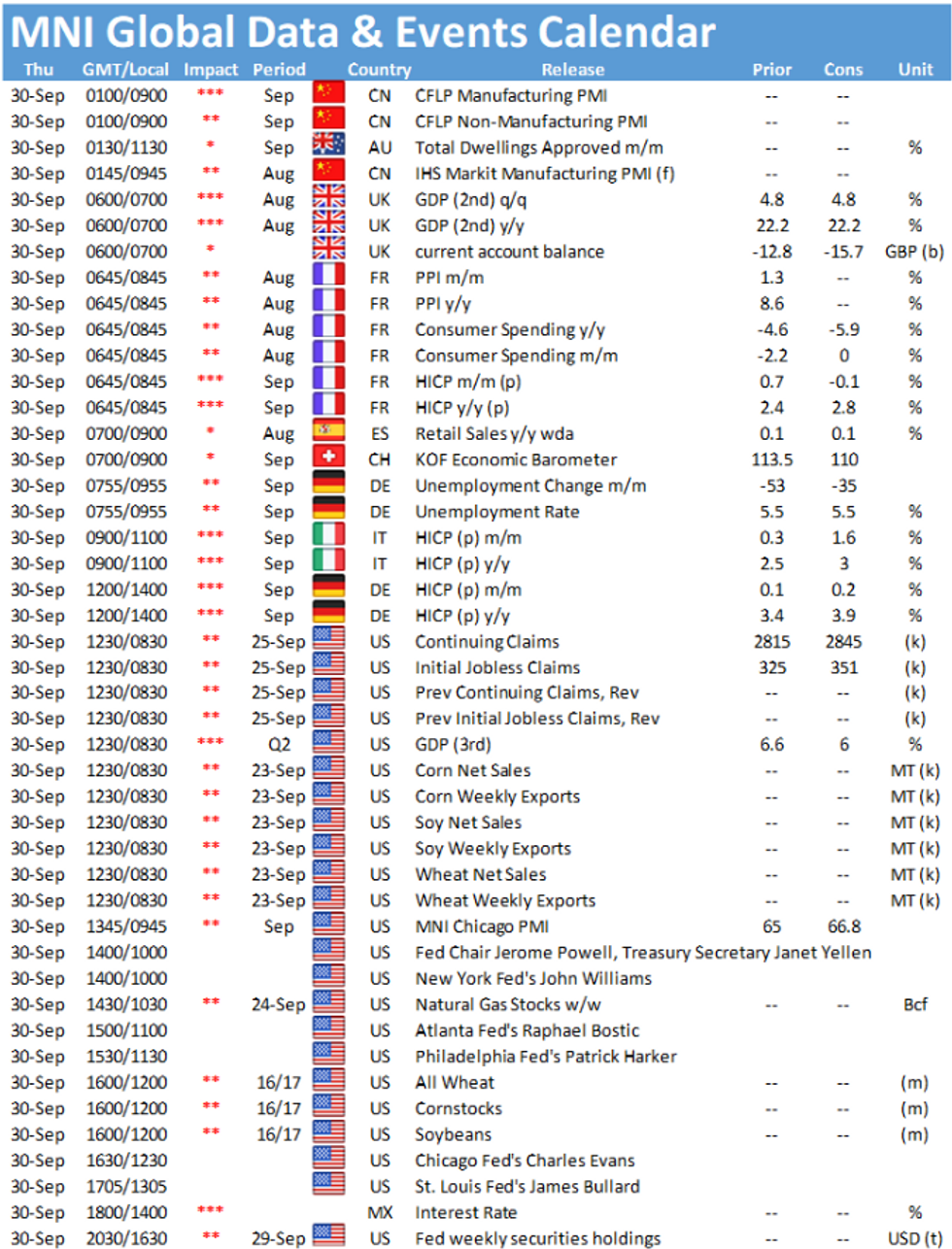

- Focus on Thu's weekly claims, GDP and at least seven additional Fed speakers Thu including Fed Chair Powell &Tsy Sec Yellen House Panel testimony.

- The 2-Yr yield is down 0.4bps at 0.297%, 5-Yr is down 0.8bps at 1.0115%, 10-Yr is up 0.7bps at 1.5444%, and 30-Yr is up 0.9bps at 2.0953%.

MONTH-END EXTENSIONS: PRELIMINARY Barclays/Bbg Extension Estimates for US

Preliminary forecast summary compared to avg increase for prior year and same time in 2020. TIPS 0.02Y, real extension 0.04Y; US Gov inflation linked 0.01Y.

| SECURITY | Estimate | 1Y Avg Incr | Last Year |

| US Tsys | 0.07 | 0.09 | 0.1 |

| Agencies | 0.08 | 0.06 | 0.05 |

| Credit | 0.09 | 0.12 | 0.11 |

| Govt/Credit | 0.07 | 0.1 | 0.09 |

| MBS | 0.09 | 0.07 | 0.09 |

| Aggregate | 0.09 | 0.09 | 0.09 |

| Long Gov/Cr | 0.06 | 0.08 | 0.12 |

| Iterm Credit | 0.07 | 0.1 | 0.1 |

| Interm Gov | 0.08 | 0.08 | 0.08 |

| Interm Gov/Cr | 0.07 | 0.09 | 0.08 |

| High Yield | 0.06 | 0.12 | 0.12 |

US TSY FUTURES CLOSE

- 3M10Y +0.355, 150.293 (L: 144.681 / H: 151.85)

- 2Y10Y +1.14, 124.391 (L: 119.515 / H: 125.237)

- 2Y30Y +1.142, 179.254 (L: 174.091 / H: 180.135)

- 5Y30Y +1.326, 107.806 (L: 104.742 / H: 108.288)

- Current futures levels:

- Dec 2Y up 0.5/32 at 110-0.25 (L: 109-31.5 / H: 110-00.5)

- Dec 5Y up 2/32 at 122-20.75 (L: 122-17 / H: 122-25)

- Dec 10Y steady at at 131-15 (L: 131-10 / H: 131-25.5)

- Dec 30Y down 8/32 at 159-2 (L: 158-22 / H: 160-03)

- Dec Ultra 30Y down 20/32 at 191-4 (L: 190-13 / H: 192-30)

US EURODOLLAR FUTURES CLOSE

- Dec 21 +0.005 at 99.825

- Mar 22 +0.005 at 99.850

- Jun 22 steady at 99.785

- Sep 22 +0.010 at 99.675

- Red Pack (Dec 22-Sep 23) +0.015 to +0.030

- Green Pack (Dec 23-Sep 24) +0.035 to +0.035

- Blue Pack (Dec 24-Sep 25) +0.010 to +0.035

- Gold Pack (Dec 25-Sep 26) -0.01 to +0.005

Short Term Rates

US DOLLAR LIBOR: Latest settlements

- O/N -0.00138 at 0.07025% (-0.00225/wk)

- 1 Month -0.00175 to 0.08238% (-0.00275/wk)

- 3 Month -0.00062 to 0.13088% (-0.00138/wk) ** Record Low 0.11413% on 9/12/21

- 6 Month -0.00050 to 0.15738% (+0.00200/wk)

- 1 Year +0.00213 to 0.24063% (+0.01100/wk)

- Daily Effective Fed Funds Rate: 0.08% volume: $71B

- Daily Overnight Bank Funding Rate: 0.07% volume: $244B

- Secured Overnight Financing Rate (SOFR): 0.05%, $883B

- Broad General Collateral Rate (BGCR): 0.05%, $378B

- Tri-Party General Collateral Rate (TGCR): 0.05%, $348B

- (rate, volume levels reflect prior session)

- Tsy 22.5Y-30Y, $2.001B accepted vs. $4.937B submission

- Next scheduled purchases

- Thu 9/30 1010-1030ET: TIPS 1Y-7.5Y, appr $2.025B

- Fri 10/01 1100-1120ET: Tsy 2.25Y-4.5Y, appr $8.425B

FED Reverse Repo Operation, Records Meant To Be Broken

NY Fed reverse repo usage climbs to another new record high: $1,415.840B from 80 counter-parties today vs. yesterday's prior record $1,365.185B.

PIPELINE: Over $6B Corporate Debt Issued Wednesday

$6.25B to Price Wednesday; $28.6B/wk

- Date $MM Issuer (Priced *, Launch #)

- 09/29 $1.5B #Enbridge $500M each: 2Y +30, $5Y +60, 08/01/51 tap +125

- 09/29 $1.25B *SEK (Swedish Export Cr) 3Y SOFR +17

- 09/29 $1.15B #Athene $650M 5Y +73, $500M 5Y FRN/SOFR, 10Y +110

- 09/29 $1B #Everest Reinsurance 31Y +115

- 09/29 $750M *APICORP 5Y Green +40

- 09/29 $600M #Bank of Nova Scotia 60NC5 3.625%

EGBs-GILTS CASH CLOSE: Gilts Underperform (Alongside GBP)

Wednesday saw some retracement from Tuesday's yield rises for the most part, but Gilts underperformed Bunds and periphery spreads traded mixed.

- Not much thematically tying moves together (equities bounced, EUR and especially GBP weakened), more of a correction of the previous session's big moves.

- Though UK assets in general appeared weaker with EU tensions (over fishing) and energy supply problems making headlines all day.

- BTPs outperformed the space, with spreads/10Y Bund tightening 1.7bp.

- Supply concluded the week with BTP and Bund sales this morning.

Closing Yields / 10-Yr Periphery EGB Spreads To Germany

- Germany: The 2-Yr yield is down 0.5bps at -0.688%, 5-Yr is down 0.9bps at -0.558%, 10-Yr is down 1.4bps at -0.213%, and 30-Yr is down 1.3bps at 0.251%.

- UK: The 2-Yr yield is down 0.4bps at 0.405%, 5-Yr is down 0.3bps at 0.625%, 10-Yr is down 0.3bps at 0.991%, and 30-Yr is up 1bps at 1.335%.

- Italian BTP spread down 1.7bps at 103.7bps / Spanish up 1bps at 65.1bps

FOREX: Sterling Sinks for Second Session

- For the second consecutive session, GBP was traded acutely weak as selling pressure on mounted on the push to fresh 2021 lows. Explanations are broad and varied, with some positing the images of fuel shortages and supply chain woes are raising the spectre of stagflation, however a number of sell-side analysts are pinning price action on month/quarter-end rebalancing, an effect that may persist into the Thursday fix.

- NZD was the sole currency to underperform GBP Wednesday, with a return lower for equities and commodity markets undermining high beta FX and growth proxies. The price action put NZD/USD within range of the 2021 lows printed back in August at $0.6805.

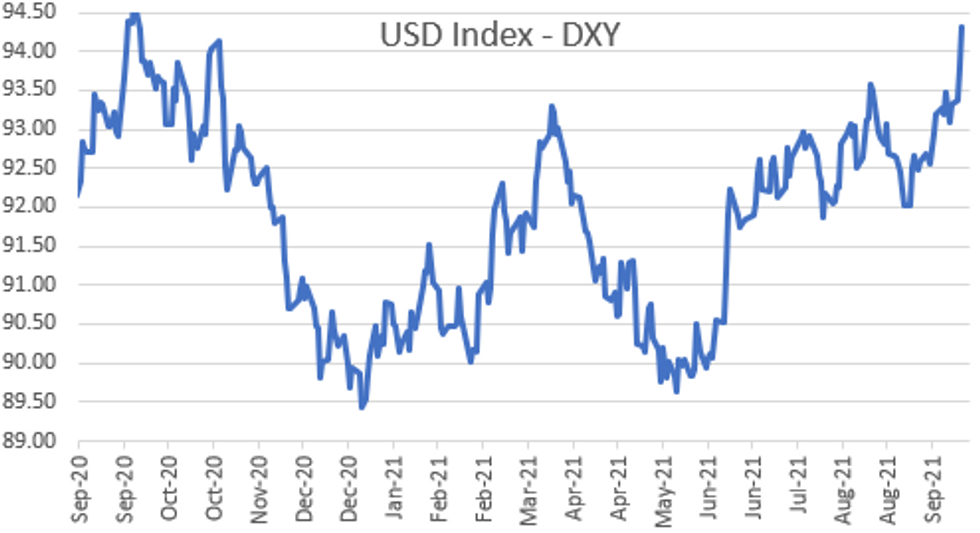

- The pervasive risk-off sentiment helped underpin greenback gains, resulting in the USD Index hitting the best levels since last November's Presidential election.

- The US MNI Chicago Business Barometer, Japanese industrial production & retail sales data, China's September manufacturing and non-manufacturing PMI, Italian CPI and the weekly jobless claims release are highlights Thursday.

- Central bank speaker events remain frantic, with Fed's Powell appearing again in front of lawmakers as well as speeches from Williams, Bostic, Harker, Evans and Bullard.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.