Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

EXECUTIVE SUMMARY

- MNI Chicago Business Barometer Jumps To 68.4 in October

- Forward guidance shift, rate hike timelines inch forward ahead Wed's FOMC, taper announcement expected

- October employment estimates robust at +400k jobs

- Tsy yield curves flatten to new 18+ month lows

US

US DATA: The Chicago Business Barometer rose to 68.4 in October, picking up after two consecutive months of decline.

- Prices Paid rose 3.6 points in October to a 42-year high of 94.3, with many companies saying prices continued to be an issue.

- Among the main five indicators, four were higher, led by Order backlogs and Employment. Only Production fell across the month.

- After the sharp September fall, Order Backlogs recovered more than half the loss, picking up 13.5 points to stand at 74.6.

- Supplier Deliveries rose 3.5 points through September to 84.7, as firms again reported worsening port congestion and ongoing logistical issues with trucking, rail, and even air cargo.

- New Orders advanced 3.1 points to 67.5, recovering from September's 6-month low. Some businesses said raw material shortages and a low supply of critical components like semiconductors at suppliers was impacting opportunities.

- Production was the only component to fall in October, dropping 2.2 points to 58.5, the lowest reading since August 2020.

- Employment increased again, up for a fourth straight month, rising 4.2 points to 56.6, the highest in just over three years.

US TSYS: Off Lows Late, Set Sights On FOMC, Oct NFP Next Week

Futures volume surged heading into the close -- month end extensions w/ TYZ1 trading another appr 200k to 1.9m after the bell. Though futures finishing near late session highs, 10s mildly weaker/hold on narrow range since late morning.

- Tsys followed EGBs lower on the open amid carry-over widening in sovereign spds after Thu's ECB policy annc (mkt underwhelmed w/ECB Lagarde presser: "not for her to say" if markets had got ahead of themselves; specs piling on rate hike bets targeting 3Q'22.

- Rates held weaker levels after Sep core PCE climbs 0.2%, +3.6% YoY, yield curves bending flatter after posting mildly steeper earlier. Sources noted prop buying 30s vs. real$ sales.

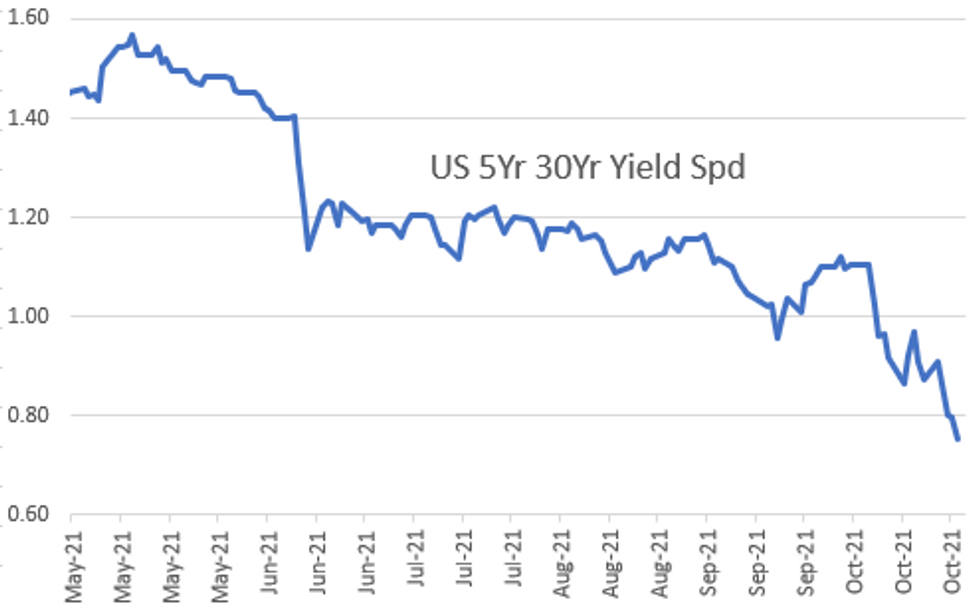

- Yield curves held flatter but off lows as futures turn steady to mixed by late morning, bonds outperformed. Sources noted continued buying in 2s-3s from domestic real$ and central banks, not to mention the +15k block buys in 5s, has short end back to steady. Curve levels shows broad range of moves after 5s30s nearly dipped below 71.0 for first time since March 2020 (L: 71.144 / H: 81.21).

- Aside from FOMC policy annc on Wednesday next week, markets get October employment data -- at the moment, mean estimate is +400k from 42 economists polled by Bbg with a range +250k to +700k.

- By the bell the 2-Yr yield is unchanged at 0.4891%, 5-Yr is up 0.2bps at 1.1864%, 10-Yr is down 2.8bps at 1.5521%, and 30-Yr is down 4.3bps at 1.9383%.

OVERNIGHT DATA

- MNI CHICAGO BUSINESS BAROMETER 68.4 OCT V 64.7 SEP

- MNI CHICAGO: PRICES PAID AT 94.3; HIGHEST SINCE OCT 1979

- MNI CHICAGO: OCT EMPLOYMENT AT 56.6; HIGHEST SINCE AUG 2018

- MNI CHICAGO: PRODUCTION 58.5 OCT V 60.7 SEP; 14-MO LOW

- US SEP PERSONAL INCOME -1.0%; NOM PCE +0.6%

- US SEP PCE PRICE INDEX +0.3%; +4.4% Y/Y

- US SEP CORE PCE PRICE INDEX +0.2%; +3.6% Y/Y

- US SEP UNROUNDED PCE PRICE INDEX +0.320%; CORE +0.211%

- MICHIGAN FINAL OCT. CONSUMER SENTIMENT AT 71.7; EST. 71.4

- CANADA AUG GROSS DOMESTIC PRODUCT +0.4% MOM

- CANADA AUG GOODS INDUSTRY GDP -0.1%, SERVICES +0.6%

- CANADA REVISED JUL GROSS DOMESTIC PRODUCT -0.1% MOM

- CANADA FLASH SEPT GDP 0.0% MOM

MARKETS SNAPSHOT

Key late session market levels:- DJIA up 20.55 points (0.06%) at 35742.53

- S&P E-Mini Future up 1 points (0.02%) at 4587.75

- Nasdaq down 3.6 points (0%) at 15444.1

- US 10-Yr yield is down 2.6 bps at 1.5539%

- US Dec 10Y are down 1/32 at 130-23

- EURUSD down 0.012 (-1.03%) at 1.1559

- USDJPY up 0.34 (0.3%) at 113.93

- WTI Crude Oil (front-month) up $0.54 (0.65%) at $83.37

- Gold is down $16.47 (-0.92%) at $1782.33

European bourses closing levels:

- EuroStoxx 50 up 16.69 points (0.39%) at 4250.56

- FTSE 100 down 11.9 points (-0.16%) at 7237.57

- German DAX down 7.56 points (-0.05%) at 15688.77

- French CAC 40 up 26.12 points (0.38%) at 6830.34

US TSY FUTURES CLOSE

- 3M10Y -2.004, 150.162 (L: 149.377 / H: 156.474)

- 2Y10Y -2.257, 106.432 (L: 104.374 / H: 110.546)

- 2Y30Y -4.148, 144.658 (L: 141.143 / H: 151.102)

- 5Y30Y -4.702, 74.775 (L: 71.144 / H: 81.21)

- Current futures levels:

- Dec 2Y up 0.25/32 at 109-20.125 (L: 109-16.375 / H: 109-22.625)

- Dec 5Y steady at at 121-23.25 (L: 121-12.5 / H: 121-27.5)

- Dec 10Y down 2/32 at 130-22 (L: 130-07.5 / H: 130-27.5)

- Dec 30Y up 11/32 at 160-27 (L: 159-15 / H: 160-30)

- Dec Ultra 30Y up 25/32 at 196-14 (L: 193-13 / H: 196-28)

US EURODOLLAR FUTURES CLOSE

- Dec 21 steady at 99.795

- Mar 22 -0.015 at 99.740

- Jun 22 -0.010 at 99.560

- Sep 22 -0.020 at 99.355

- Red Pack (Dec 22-Sep 23) -0.03 to -0.02

- Green Pack (Dec 23-Sep 24) -0.02 to +0.010

- Blue Pack (Dec 24-Sep 25) +0.010 to +0.030

- Gold Pack (Dec 25-Sep 26) +0.025 to +0.030

SHORT TERM RATES

US DOLLAR LIBOR: Latest settlements

- O/N -0.00150 at 0.07213% (-0.00138/wk)

- 1 Month +0.00112 to 0.08750% (-0.00038/wk)

- 3 Month +0.00062 to 0.13225% (+0.00738/wk) ** Record Low 0.11413% on 9/12/21

- 6 Month +0.00737 to 0.20100% (+0.02900/wk)

- 1 Year -0.00950 to 0.36113% (+0.04425/wk)

- Daily Effective Fed Funds Rate: 0.08% volume: $84B

- Daily Overnight Bank Funding Rate: 0.07% volume: $272B

- Secured Overnight Financing Rate (SOFR): 0.05%, $871B

- Broad General Collateral Rate (BGCR): 0.05%, $345B

- Tri-Party General Collateral Rate (TGCR): 0.05%, $317B

- (rate, volume levels reflect prior session)

- Tsy 10Y-22.5Y, $1.401B accepted vs. $4.722B submission

- Next scheduled purchases

- Mon 11/01 1100-1120ET: Tsy 22.5Y-30Y, appr $2.025B

- Tue 11/02 1010-1030ET: TIPS 1Y-7.5Y, appr $2.025B

- Wed 11/03 No buy operation due to FOMC annc

- Thu 11/04 1010-1030ET: Tsy 4.5Y-7Y, appr $6.025B

- Thu 11/04 1100-1120ET: Tsy 10Y-22.5Y, appr $1.425B

- Fri 11/05 1010-1030ET: Tsy 2.25Y-4.5Y, appr $8.425B

FED Reverse Repo Operation

NY Federal Reserve/MNI

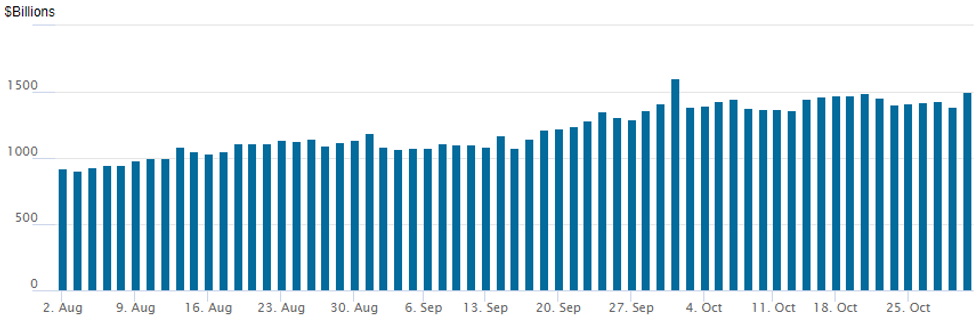

NY Fed reverse repo surged to second highest usage on record at $1,502.296B from 94 counterparties vs. $1,384.684B on Thursday. Record high remains at $1,604.881B from Thursday, September 30.

PIPELINE: October Total High-Grade Issuance $148.8B

$8.8B Priced Thursday, $28.1B/wk puts October total at $148.8B well over October 2020 total issuance of $111.65B

- Date $MM Issuer (Priced *, Launch #)

- 10/28 $4B *Rep of Peru $2.25B 12Y +150, $750M 2051 Tap +150, $1B 50Y +180

- 10/28 $1.75B *Capital One $1.25B 6NC5 fix/FRN +70, $500M 11NC10 fix/FRN +105

- 10/28 $1.25B *Rio Tinto 30Y +85

- 10/28 $700M *Ares Capital 10Y +170

- 10/28 $600M *Kimberly-Clark WNG 10Y +48

- 10/28 $500M *Fifth Third 6NC5 +53

EGBs: Peripheral Spreads Blow Wider as ECB Support Seen Waning

- Markets took further their view that the ECB failed to push back against rate hike expectations by pushing peripheral European spreads wider still Friday, with solid volumes seen throughout the session. IT/GE and SP/GE 10y yield spreads closed wider by 9 and 6bps apiece, with a similar impact seen across the front-end of the curve.

- Bund futures extended the Thursday weakness to touch a fresh low of 167.71, marking a pullback off the midweek highs of over 2 points. The German curve traded flatter still, taking the lead from similar moves stateside.

- Focus in the coming week turns to the Fed rate decision on Wednesday as well as the decisions from the RBA, Bank of England and Norwegian central bank.

FOREX: EURUSD Sinks As Greenback Comes Marching Back

- After yesterday's largest intra-day range for EURUSD since mid-June of 110 pips, an even more powerful reversal ensued on Friday, leading the single currency to plummet well over 1%, taking out the ECB lows to trade just shy of the October lows at 1.1525.

- Thursday's rally fell short of a key resistance at 1.1711, the top of a bear channel drawn from the Jun 1 high. Today's weakness confirms broader trend conditions remain bearish below this channel resistance. Support can be found at 1.1493, 50.0% retracement of the Mar '20 - Jan '21 bull phase.

- Particular EUR weakness prompted negative price action in the crosses, with EURJPY, EURAUD, EURCAD and EURNZD all falling comfortably over 0.5%.

- The US dollar came roaring back after the dollar index found strong touted support at the 50-day MA. Additionally, the 23.6% retracement of the 2021 Low-High held at 93.30.

- The greenback rally sent the dollar index (+0.85%) soaring to the best levels of the week, signalling further strength to the mid-Oct highs, residing at 94.56.

- The dollar bid was broad based, gaining against all other G10 currencies. Particular weakness was seen in the Norwegian Krona, with USDNOK rising 1.4% on Friday.

- US ISM Manufacturing PMI headlines Monday's calendar, before the RBA meet early on Tuesday.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.