Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

EXECUTIVE SUMMARY

- MNI STATE OF PLAY: BOE Hikes As Inflation Heads To 6%

- MNI STATE OF PLAY: ECB Flexibility Future Crises Key: Lagarde

- U.S. PUSHES EU TO READY RUSSIA SANCTIONS HITTING ENERGY, BANKS, Bbg

EUROPE

BoE: The Bank of England delivered a 15-basis point hike at its December meeting, acting on its November promise that a hike was likely 'in coming months'. With Bank staff predicting that headline CPI inflation will peak around 6% in the spring, triple the Monetary Policy Committee's target, policymakers voted 8-1 to increase rates now and not wait for a February decision.

- Market participants had responded to the likelihood of a large new wave of Covid infections due to the Omicron variant by lowering the odds on a December hike to around 1 -in-5, but MPC members were scrupulous following the November guidance in offering no steer that a rate increase would be delayed and in the event they backed the December rise, as MNI's latest BOE Insight piece highlighted (MNI INSIGHT: BOE Meeting Live To Consider Hike Despite Omicron).

- There had been some speculation BOE Governor Andrew Bailey wanted strong support for this first hike and, after only two members backed an increase in November, the committee was firmly behind this move.

- Policymakers also decided to extend the reinvestments from PEPP until at least October 2024, and allow special provisions for Greek sovereign debt within the programme.

- Monthly net purchases under the APP will be set at a pace of EUR40 billion in Q2, 2022, and EUR30 billion Q3, then maintained from October 2022 at a monthly pace of EUR20 billion for as long as necessary, Lagarde said. Net purchases under the PEPP could be restarted if needed to counteract negative shocks related to the pandemic, in line with MNI's latest sources story (MNI SOURCES: ECB Seen Buying E40-60 Bln After March) .

US TSYS: Hawks Are Circling, BoE Hikes, ECB Ups Inflation Forecast

Tsys trading mostly higher (30Y-ultra weaker amid decent steepener flow since Wed's FOMC), near top end session range -- a stark contrast from session lows after the BoE and ECB policy annc's.

- Yield curves steepened but were off highs as long end partially recovered from post BoE/ECB policy selling. Fading the move, trading desks report central bank selling in 2s-3s and couple waves of buying in 30s, foreign real money selling 5s. Large steepener Blocks (5s and 10s vs. 30Y Ultra) since late Wednesday setting the tone after months of flattening.

- Misc acct buying in 2s-10s during early London trade evaporated on BoE rate hike to .25 followed by additional selling on ECB annc (steady, raises APP pace). Trading desks noted fast$, bank and dealer acct selling in long end initially, prop selling 10s, flattener unwinds (5s and 10s vs 30s).

- Aside the 2x taper acceleration, Chair Powell said rate liftoff could start after Mar22 (if warranted, etc), the FOMC shifted dot-plot to three hikes in 2022 and 2023. Forward guidance siphoned more aggressive rate hike pricing out of Eurodollar futures w/ Reds-Blues +0.080-0.120. Inversion of EDZ4 vs. futures out to EDM6 has waned as policy shock/error is quickly receding. EDZ4 (98.375) remains inverted through EDU5 (98.38).

- The 2-Yr yield is down 4.2bps at 0.6209%, 5-Yr is down 7.3bps at 1.1718%, 10-Yr is down 3.9bps at 1.4173%, and 30-Yr is down 0.3bps at 1.8565%.

OVERNIGHT DATA

- US JOBLESS CLAIMS +18K TO 206K IN DEC 11 WK

- US PREV JOBLESS CLAIMS REVISED TO 188K IN DEC 04 WK

- US CONTINUING CLAIMS -0.154M to 1.845M IN DEC 04 WK

- MNI: US NOV HOUSING STARTS 1.679M; PERMITS 1.712M

- US OCT STARTS REVISED TO 1.502M; PERMITS 1.653M

- US NOV HOUSING COMPLETIONS 1.282M; OCT 1.231M (REV)

- US DEC PHILADELPHIA FED MFG INDEX 15.4

- US NOV INDUSTRIAL PROD +0.5%; CAP UTIL 76.8%

- US OCT IP REV TO +1.7%; CAP UTIL REV 76.5%

- US NOV MFG OUTPUT +0.7%

- US DATA: US PMI Comes in Below Forecast

- US Market US Manufacturing PMI (Dec P) M/M 57.8 vs. Exp. 58.5 (Prev. 58.3)

- US Services PMI (Dec P) M/M 57.5 vs. Exp. 58.8 (Prev. 58.0)

- US Composite PMI (Dec P) M/M 56.9 (Prev. 57.2)

MARKETS SNAPSHOT

Key late session market levels:

- DJIA down 84.42 points (-0.24%) at 35841.08

- S&P E-Mini Future down 51.25 points (-1.09%) at 4649

- Nasdaq down 421.4 points (-2.7%) at 15143.15

- US 10-Yr yield is down 3.9 bps at 1.4173%

- US Mar 10Y are up 20/32 at 131-3

- EURUSD up 0.0035 (0.31%) at 1.1324

- USDJPY down 0.41 (-0.36%) at 113.64

- WTI Crude Oil (front-month) up $1.04 (1.47%) at $71.91

- Gold is up $20.98 (1.18%) at $1797.89

- EuroStoxx 50 up 42.19 points (1.01%) at 4201.87

- FTSE 100 up 89.86 points (1.25%) at 7260.61

- German DAX up 160.05 points (1.03%) at 15636.4

- French CAC 40 up 77.44 points (1.12%) at 7005.07

US TSY FUTURES CLOSE

- 3M10Y -2.47, 137.854 (L: 136.495 / H: 142.54)

- 2Y10Y +1.696, 80.432 (L: 77.882 / H: 82.644)

- 2Y30Y +5.101, 124.184 (L: 117.395 / H: 125.588)

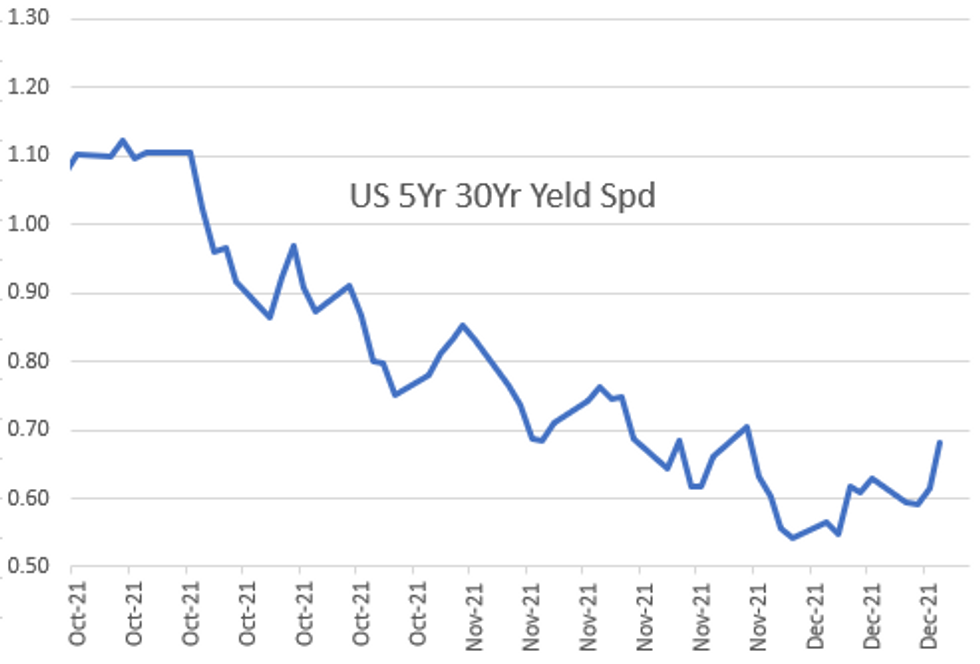

- 5Y30Y +7.359, 68.682 (L: 59.773 / H: 70)

- Current futures levels:

- Mar 2Y up 4.25/32 at 109-6.125 (L: 109-01.75 / H: 109-06.5)

- Mar 5Y up 13.5/32 at 121-7.5 (L: 120-24 / H: 121-09.25)

- Mar 10Y up 18/32 at 131-1 (L: 130-11.5 / H: 131-04.5)

- Mar 30Y up 6/32 at 161-30 (L: 161-03 / H: 162-11)

US EURODOLLAR FUTURES CLOSE

- Mar 22 +0.005 at 99.660

- Jun 22 +0.005 at 99.440

- Sep 22 +0.030 at 99.250

- Dec 22 +0.055 at 99.005

- Red Pack (Mar 23-Dec 23) +0.080 to +0.115

- Green Pack (Mar 24-Dec 24) +0.10 to +0.120

- Blue Pack (Mar 25-Dec 25) +0.080 to +0.090

- Gold Pack (Mar 26-Dec 26) +0.070 to +0.080

SHORT TERM RATES

US DOLLAR LIBOR: Latest settlements

- O/N -0.00175 at 0.07638% (+0.00413/wk)

- 1 Month -0.00475 to 0.10388% (-0.00475/wk)

- 3 Month -0.00200 to 0.21363% (+0.01538/wk) ** Record Low 0.11413% on 9/12/21

- 6 Month +0.01000 to 0.31150% (+0.02325/wk)

- 1 Year +0.00775 to 0.52463% (+0.01525/wk)

- Daily Effective Fed Funds Rate: 0.08% volume: $74B

- Daily Overnight Bank Funding Rate: 0.07% volume: $248B

- Secured Overnight Financing Rate (SOFR): 0.05%, $959B

- Broad General Collateral Rate (BGCR): 0.05%, $355B

- Tri-Party General Collateral Rate (TGCR): 0.05%, $337B

- (rate, volume levels reflect prior session)

- Tsy 10Y-22.5Y, appr $1.601B accepted vs. $4.693B submission

- TIPS 1Y-7.5Y, appr $1.501B accepted vs. $2.570B submission

- Next scheduled purchase

- Fri 12/17 1010-1030ET: Tsy 22.5Y-30Y, appr $1.825B vs. $1.600B prior

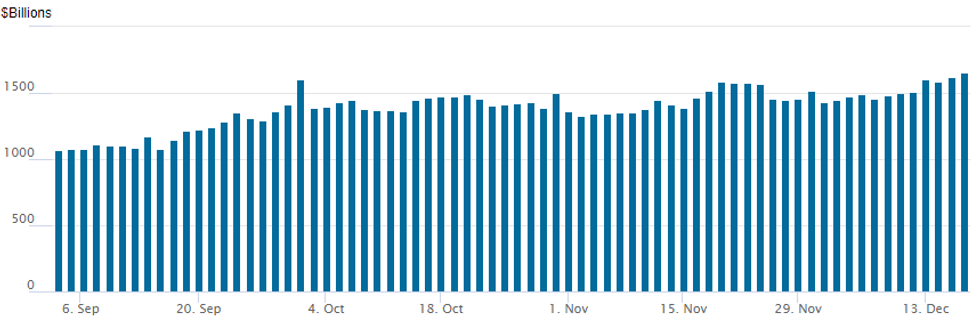

FED Reverse Repo Operation, Second Consecutive Record High

NY Federal Reserve/MNI

NY Fed reverse repo usage climbs to second consecutive all-time high of $1,657.626B from 78 counterparties after Wednesday's $1,621.097B beat prior record high of 1,604.881B from Thursday, September 30.

EGBs-GILTS CASH CLOSE: BoE Steals The Show

Gilts underperformed Bunds Thursday, with Greece outperforming among periphery EGBs, amid one of the busiest 24 hours in recent memory for central bank decisions.

- After the Fed took a hawkish turn Weds evening, the BoE surprised many today by hiking Bank rate 15bp; this was followed by the ECB's announcement it was ending net PEPP purchases in March 2022 but will reinvest until at least Oct 2024 and keep APP purchases (beginning Q2 2022) open-ended.

- The UK curve flattened sharply with the short end selling off, though this reversed, with yields ending the day higher in parallel. The German curve steepened all day. GGBs easily outperformed, with the ECB announcing that they could be the beneficiary of flexible PEPP reinvestment policy.

- Weak PMI data and Omicron headlines were largely shrugged off.

Closing Yields / 10-Yr Periphery EGB Spreads To Germany

- Germany: The 2-Yr yield is down 1bps at -0.69%, 5-Yr is unchanged at -0.583%, 10-Yr is up 1.2bps at -0.348%, and 30-Yr is up 4.1bps at -0.005%.

- UK: The 2-Yr yield is up 1.9bps at 0.508%, 5-Yr is up 2.1bps at 0.61%, 10-Yr is up 2.1bps at 0.757%, and 30-Yr is up 1.5bps at 0.918%.

- Italian BTP spread up 4.3bps at 132.2bps / Greek down 3bps at 156.3bps

FOREX: EUR and GBP Rise After Central Bank Decisions, USD Weakness Prevails

- The greenback slipped another half a percent following yesterday’s reversal lower after the FOMC statement and press conference. The DXY weakness was aided by falls in both USDJPY and USDCHF as global equities retraced gains.

- Central bank decisions were again the story of the day on Thursday. The Norges Bank kicked things off lifting the key rate by 25bps. Initial weakness for EURNOK, trading down to 10.12, has largely reversed course throughout the afternoon and the NOK remains broadly unchanged.

- The Bank of England then gave GBP a shot in the arm with a rate hike that was not expected by the majority of surveyed analysts. Cable jumped from 1.3280 to highs of 1.3368 in very quick fashion.

- This area essentially capped the topside with GBP grinding lower throughout the remainder of the session. Resistance was broken at 1.3308, the 20-day EMA signalling a short-term reversal of the bearish technical outlook and therefore tomorrows price action may be significant for the short-term momentum.

- Next up was the ECB and while broadly in line with expectations, importantly for monetary policy, the inflation forecast was revised up over the horizon, suggesting a hike in 2023 is still feasible.

- The EUR remained buoyed following a breach of 1.1300 during the European morning and extended on gains toward 1.1360 as Lagarde spoke. Technically, the pair remains in a range and below 1.1383, Nov 30 high. A break of this resistance would signal potential for a stronger recovery towards 1.1429, the 50-day EMA.

- Today’s retracement in equities lent support to both the Japanese Yen and the Swiss Franc. USDJPY was unable to remain above 114 and once back below, shot down an additional 40 pips to 113.60. Upside momentum for the pair had been limited by the broad dollar weakness and the reversal in equities was all the pair needed to gravitate lower. In tandem CHF topped the G10 leaderboard, rising 0.6% back below 0.9200.

- Overnight we will have the Bank of Japan decision, before UK retail sales and German IFO data finish off the week.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.