Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

EXECUTIVE SUMMARY

- MNI BRIEF: Three Fed Banks Wanted Discount Rate Hike--Minutes

- WHITE HOUSE: Biden Announces Russia Sanctions, first tranche starts Wednesday

- Russia Sanctions Include Sovereign Debt Restrictions

- UK: UK'S JOHNSON:PUTIN'S VENTURE IN UKRAINE MUST FAIL, Bbg

- Germany: Scholz Halts Pipeline as Putin Backs Separatists

US

US: President Biden has announced US sanctions on Russia. He has said that Russia has followed the playbook outlined by Sec of State Blinken at the UN last week. Here is a summary of Bidens comments from the White House.

- 'Putin authorised Russian troops to deploy into Ukraine. Claiming large areas under the jurisdiction of Ukrainian government.'

- 'This is the beginning of a Russian invasion of Ukraine'.

- 'We are enacting sanctions far beyond what we did in 2014'.

- 'It is a flagrant violation of international law.' 'Russia has now undeniably moved against Ukraine'.

- 'I am announcing the first tranche of sanctions. Closely coordinated with allies. We are implementing full blocking sanctions on VEB and military bank. Comprehensive sanctions on Russian sovereign debt. Russia can no longer raise money on US or EU markets.'

- 'Starting tomorrow we are imposing sanctions of Russian elites and their family members.'

- 'We are working with Germany to ensure Nordstream 2 WILL NOT move forward.'

- 'US will continue to provide defensive support of Ukraine. US equipment will be moved to Baltic states. This is a defensive move. We will defend every inch of NATO territory.'

- 'We believe Russia will go further. There are still more that 150k troops surrounding Ukraine.'

FED: The directors of the Federal Reserve Banks of Cleveland, St. Louis and Kansas City voted to raise the discount rate by 25bps in the period ahead of the January FOMC, according to minutes from meetings of the regional Bank boards, a shift from the previous intermeeting period of unanimous consent for keeping the rate steady.

- The Fed's board of governors sided with the majority, keeping the rate steady at 0.25%, and expressed "no sentiment" for changing the rate at the time, the minutes said.

- "Given ongoing inflation pressures and strong labor market conditions, a number of directors noted that it might soon become appropriate to begin a process of removing policy accommodation.," the minutes said. "Inflation remained elevated, and some directors noted uncertainty and upside risks in connection with the inflation outlook."

US TSYS: US Sanctions Russia, First Tranche Start Wednesday

US Tsy trade mixed after the bell, curves flatter with long end outperforming, stocks well off late session lows (SPX emini -25.0 at 4317.0), Gold weaker -5.84, WTI crude gained $1.28/bbl to 92.35.

- Markets reacted the way one would expect following the Russia/Ukraine news last night: gap bid in rates/safe havens on Russia formally recognizing and in short order inserting "peacekeeping" forces into Ukraine separatist regions of Donetsk and Luhansk.

- Risk-off/safe-haven support evaporated through the session -- perhaps tied to to measured response via sanctions from US and allies lending to relative calm, Pres Biden annc sanctions similar to EU later in the session: 'We are implementing full blocking sanctions on VEB and military bank. Comprehensive sanctions on Russian sovereign debt. Russia can no longer raise money on US or EU markets.'

- Decent 2Y note sale, short end Tsy futures held weaker but off lows after $52B 2Y note auction (91282CEA5) small stop through: 1.553% high yield vs. 1.57% WI; 2.64x bid-to-cover vs. last moth's 2.81x, well over five auction avg: 2.56x.

- Indirect take-up: eases to 65.58% vs. 66.00% in January;

- Primary dealer take-up falls to 15.65% vs. 24.61% last month;

- Direct take-up: climbs to 18.77% vs. last month's 1+ year low of 9.39%

- BLOCKING MAJOR RUSSIAN FINANCIAL INSTITUTIONS

- TARGETING ELITES AND FAMILIES CLOSE TO PUTIN

- SOVEREIGN DEBT RESTRICTIONS

- On the latter, US Tsy dept announced OFAC also increased restrictions on dealings in Russia’s sovereign debt, further cutting Russia off from sources of revenue to fund its government or President Putin’s priorities, including his further invasion into Ukraine. These restrictions significantly cut off a core way for Russia to raise money. This kind of measure creates a strain on resources for the Russian state and greater risk for its ability to manage its finances.

- Specifically, OFAC issued Russia-related Directive 1A under E.O. 14024, “Prohibitions Related to Certain Sovereign Debt of the Russian Federation” (the “Russia-related Sovereign Debt Directive”), amending and superseding Directive 1 under E.O. 14024. This extends existing sovereign debt prohibitions to cover participation in the secondary market for bonds issued after March 1, 2022 by the Central Bank of the Russian Federation, the National Wealth Fund of the Russian Federation, or the Ministry of Finance of the Russian Federation.

OVERNIGHT DATA

- US Q4 FHFA HPI Q/Q SA +3.3% V +17.5% Q4 2021

- US DEC FHFA HPI SA +1.2% V +1.2% NOV; +17.6% Y/Y

- Markit: US economy rebounds from Omicron wave, but output prices rise at survey record pace.

- Flash US Composite Output Index at 56.0 (51.1 in January). 2-month high.

- Flash US Services Business Activity Index at 56.7 (51.2 in January). 2-month high.

- Flash US Manufacturing PMI at 57.5 (55.5 in January). 2-month high.

- Flash US Manufacturing Output Index at 52.5 (50.5 in January). 2-month high.

- U.S. FEB. RICHMOND FED FACTORY INDEX AT 1

- U.S. FEB. CONSUMER CONFIDENCE AT 110.5; EST. 110.0 (prior revised lower)

- U.S. FEB. RICHMOND FED FACTORY INDEX AT 1 (10 expected, 8 prior)

- US FEB PHILADELPHIA FED NONMFG INDEX 15.9

MARKETS SNAPSHOT

Key late session market levels:

- DJIA down 293.37 points (-0.86%) at 33759.47

- S&P E-Mini Future down 15.25 points (-0.35%) at 4326.75

- Nasdaq down 37.1 points (-0.3%) at 13494.64

- US 10-Yr yield is up 2.1 bps at 1.9494%

- US Mar 10Y are down 7/32 at 126-14.5

- EURUSD up 0.0027 (0.24%) at 1.1339

- USDJPY up 0.36 (0.31%) at 115.1

- WTI Crude Oil (front-month) up $1.28 (1.41%) at $92.35

- Gold is down $6.7 (-0.35%) at $1900.52

- EuroStoxx 50 down 0.24 points (-0.01%) at 3985.47

- FTSE 100 up 9.88 points (0.13%) at 7494.21

- German DAX down 38.12 points (-0.26%) at 14693

- French CAC 40 down 0.74 points (-0.01%) at 6787.6

US TSY FUTURES CLOSE

- 3M10Y +1.309, 158.142 (L: 148.213 / H: 161.389)

- 2Y10Y -7.011, 38.682 (L: 38.201 / H: 43.567)

- 2Y30Y -7.567, 69.262 (L: 68.433 / H: 77.039)

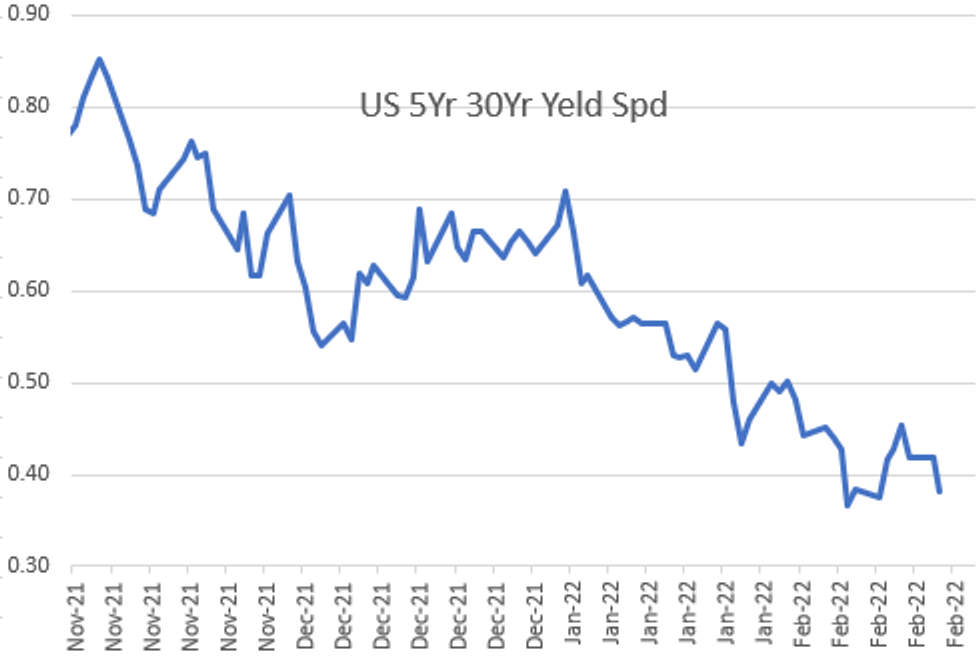

- 5Y30Y -3.039, 38.735 (L: 37.895 / H: 44.347)

- Current futures levels:

- Mar 2Y down 5/32 at 107-20 (L: 107-19.375 / H: 107-28)

- Mar 5Y down 7.25/32 at 117-27.75 (L: 117-26.5 / H: 118-13)

- Mar 10Y down 6/32 at 126-15.5 (L: 126-12 / H: 127-09)

- Mar 30Y down 1/32 at 153-0 (L: 152-17 / H: 154-14)

- Mar Ultra 30Y down 6/32 at 182-25 (L: 182-06 / H: 185-10)

US 10Y FUTURES TECH: (H2) Stalls Above The 20-Day EMA

- RES 4: 128-22+ High Jan 24

- RES 3: 128-03+ 50-day EMA

- RES 2: 127-24 High Feb 4

- RES 1: 127-09 High Feb 22

- PRICE: 126-19+ @ 16:15 GMT Feb 22

- SUP 1: 125-17+ Low Feb 10 and the bear trigger

- SUP 2: 125-06+ Low May 30 2019 (cont)

- SUP 3: 125-04+ 2.00 proj of the Jan 13 - 19 - 24 price swing

- SUP 4: 123-25 2.0% 10-dma envelope

Treasuries traded higher early Tuesday faded off levels just above the 20-day EMA (126-30+). Despite recent gains, the trend outlook remains bearish. Moving average conditions point south and a price sequence of lower lows and lower highs is intact. The bear trigger is 125-17+, the Feb 10 low. On the upside, a resumption of gains would open the 50-day EMA at 128-03+.

US EURODOLLAR FUTURES CLOSE

- Mar 22 -0.045 at 99.315

- Jun 22 -0.085 at 98.760

- Sep 22 -0.10 at 98.375

- Dec 22 -0.105 at 98.065

- Red Pack (Mar 23-Dec 23) -0.10 to -0.055

- Green Pack (Mar 24-Dec 24) -0.04 to -0.015

- Blue Pack (Mar 25-Dec 25) -0.01 to steady

- Gold Pack (Mar 26-Dec 26) steady

SHORT TERM RATES

US DOLLAR LIBOR: Latest settlements:

- O/N +0.00100 at 0.07657% (+0.00100/wk)

- 1 Month +0.01386 to 0.17586% (+0.00515/wk)

- 3 Month +0.0240 to 0.48786% (+0.00829/wk) ** Record Low 0.11413% on 9/12/21

- 6 Month +0.02314 to 0.78143% (+0.00014/wk)

- 1 Year +0.03086 to 1.28857% (+0.00271/wk)

STIR: FRBNY EFFR for prior session:

- Daily Effective Fed Funds Rate: 0.08% volume: $71B

- Daily Overnight Bank Funding Rate: 0.07% volume: $245B

US TSYS: Repo Reference Rates

- Secured Overnight Financing Rate (SOFR): 0.05%, $931B

- Broad General Collateral Rate (BGCR): 0.05%, $345B

- Tri-Party General Collateral Rate (TGCR): 0.05%, $335B

- (rate, volume levels reflect prior session)

NY Fed Purchase Operation: The Desk plans to purchase approximately $20 billion, ending Thu, March 9.

- TIPS 1Y-7.5Y, appr $1.001B accepted vs. $2.747B submission

- Next scheduled purchases:

- Thu 02/24 1010-1030ET: Tsy 0Y-22.5Y, appr $6.225B steady

- Tue 03/01 1100-1120ET: TIPS 7.5Y-30Y, appr $0.625B vs. $1.225B prior

- Thu 03/03 1100-1120ET: Tsy 7Y-10Y, appr $1.625B vs. $3.225 prior

- Tue 03/08 1010-1030ET: Tsy 22.5Y-30Y, appr $1.825B steady

- Thu 03/09 1010-1030ET: Tsy 2.25Y-4.5Y, appr $4.025B

FED Reverse Repo Operation

NY Federal Reserve/MNI

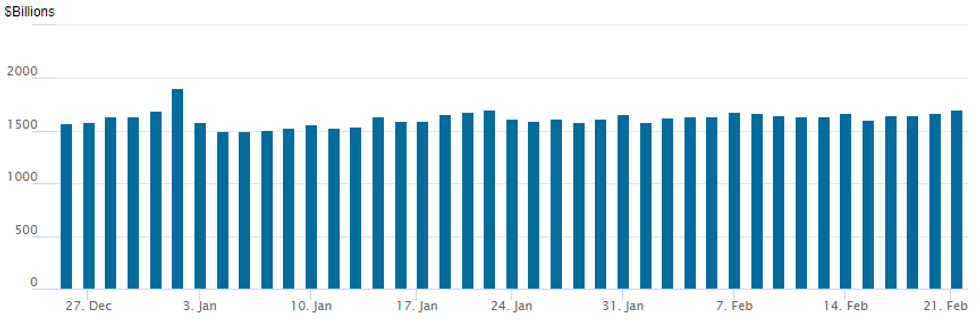

NY Fed reverse repo usage climbs to $1,699.432B w/ 81 counterparties vs. $1,674.929B prior session -- remains well off all-time high of $1,904.582B on Friday, December 31.

PIPELINE: $2.9B ConocoPhillips 3Pt Launched

- Date $MM Issuer (Priced *, Launch #)

- 02/22 $2.9B #ConocoPhillips $900M 2NC.5 +60, $900M 3NC1 +70, $1.1B 10Y +155

- 02/22 $1.3B #Eversource $650M 5Y +105, $650M 10Y +145

- 02/22 $1B #Stanley Black & Decker $00M 3NC1 +62.5, $500M 10Y +110

- 02/22 $500M #Moody's 30Y +160

- On tap for Wednesday:

- 02/23 $Benchmark PSP Capital 3Y FRN/SOFR +26

- 02/23 $Benchmark Rep of Chile investor calls

EGBs-GILTS CASH CLOSE: Reversal On Geopolitical Relief

Markets entered Tuesday firmly in risk-off mode, but faded the move later in the morning - with geopolitics driving throughout once again.

- The risk-on reversal came as both Russia and the US/Europe appeared more measured in their approach to the Ukraine crisis than had been feared late Monday.

- After showing some signs of short covering last week (see today's Europe Pi for more), Bund futures sold off sharply this morning.

- Short end rates sold off; one exception was March UK which further faded 50bp hike probability following relatively dovish comments by BoE's Ramsden.

- BTP spreads fell sharply thanks to the broader risk-on move.

Closing Yields / 10-Yr Periphery EGB Spreads To Germany

- Germany: The 2-Yr yield is up 5.5bps at -0.399%, 5-Yr is up 4.9bps at 0.001%, 10-Yr is up 3.7bps at 0.243%, and 30-Yr is up 2.2bps at 0.496%.

- UK: The 2-Yr yield is up 5.4bps at 1.338%, 5-Yr is up 6bps at 1.362%, 10-Yr is up 6.3bps at 1.471%, and 30-Yr is up 5.6bps at 1.548%.

- Italian BTP spread down 2.4bps at 168.1bps / Spanish down 1.7bps at 102bps

FOREX: Swiss Franc Retraces Monday Strength, Scandinavian FX Outperforms

- Price action for the majors remains subdued as equity markets continue to have large swings amid the geopolitical headline turbulence. A strong initial rally across equity/commodity markets was met with some US dollar weakness, however, renewed pressure on risk throughout US hours leaves the DXY unchanged for Tuesday.

- EURUSD appears content trading between 1.1300-50 while USDJPY resides close to the week’s open just below the 115 mark.

- More notable move seen in the Swiss Franc as the majority of yesterday’s risk-off induced strength was unwound. EURCHF climbed 0.73% to 1.0436, after the downward move fell shy of the 1.0300 support level.

- Scandinavian FX were the strongest performers in the G10 space with commodity-tied currencies leading the way as Brent crude futures touched $99.50/bbl, the highest level since 2014. NOK leads the way, rising 1.38% against the greenback as the Russia - Europe Nordstream 2 gas pipeline falls victim to sanctions responses.

- Late post-Biden relief rally in equities lent strong support to the Russian Ruble which is also seen over 1% in the green against the dollar with markets potentially expecting a wider array of strict sanctions from the US.

- Australian Wage Price Index data overnight before the February RBNZ rate decision/statement. There is very limited scheduled event risk for Wednesday’s US session.

Wednesday Data Roundup

| Date | GMT/Local | Impact | Flag | Country | Event |

| 23/02/2022 | 0030/1130 | *** |  | AU | Quarterly wage price index |

| 23/02/2022 | 0030/1130 | *** | | AU | Quarterly construction work done |

| 23/02/2022 | 0100/1400 | *** |  | NZ | RBNZ official cash rate decision |

| 23/02/2022 | 0700/0800 | * |  | DE | GFK Consumer Climate |

| 23/02/2022 | 0700/1500 | ** |  | CN | MNI China Liquidity Suvey |

| 23/02/2022 | 0745/0845 | ** |  | FR | Manufacturing Sentiment |

| 23/02/2022 | 0915/1015 |  | EU | ECB Elderson Intro & panel participation at Eurofi Seminar | |

| 23/02/2022 | 0930/0930 |  | UK | BOE Governor Bailey et al at TSC | |

| 23/02/2022 | 1000/1100 | *** | | EU | HICP (f) |

| 23/02/2022 | 1130/1230 | | EU | ECB de Guindos Q&A at El Español & Invertia symposium | |

| 23/02/2022 | 1200/0700 | ** |  | US | MBA Weekly Applications Index |

| 23/02/2022 | 1330/0830 | * |  | CA | Quarterly financial statistics for enterprises |

| 23/02/2022 | 1355/0855 | ** | | US | Redbook Retail Sales Index |

| 23/02/2022 | 1500/1500 | | UK | BOE Tenreyro speaks at NIESR Institute lecture | |

| 23/02/2022 | 1630/1130 | ** | | US | US Treasury Auction Result for 2 Year Floating Rate Note |

| 23/02/2022 | 1630/1130 | * | | US | US Treasury Auction Result for Cash Management Bill |

| 23/02/2022 | 1800/1300 | * | | US | US Treasury Auction Result for 5 Year Note |

| 23/02/2022 | 2030/1530 | | US | San Francisco Fed's Mary Daly |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.