Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

EXECUTIVE SUMMARY

- MNI INTERVIEW: Fed To Stay On Hold After Rates Peak -Blinder

- MNI INTERVIEW: BOC Already Faces Wage-Driven Inflation - CFIB

- MNI BRIEF: Fed To Launch Payments System Next Summer -Brainard

- EU PREPARING POWER MARKET EMERGENCY INTERVENTION: VON DER LEYEN, Bbg

- IEA HEAD BIROL: A FURTHER STRATEGIC PETROLEUM RESERVE RELEASE IS "NOT OFF THE TABLE"- Reuters

US

FED: The Federal Reserve is unlikely to cut interest rates shortly after it stops raising them as many in financial markets still seem to think, ex-Fed Vice Chair Alan Blinder told MNI on the sidelines of this year’s Jackson Hole conference.

- The Fed may also need to push interest rates somewhat higher than the central bank’s median projection of 3.8%, Blinder said in an interview with MNI’s FedSpeak podcast.

- “I never believed that and I think Powell never believed that, and part of his exclamation point was to basically shout at the markets, stop believing that because it’s not going to be over that fast,” said Blinder, also a former member of the White House Council of Economic Advisers and a Princeton University professor. For more see MNI Policy main wire at 1208ET.

- "The shift to real-time payment infrastructure requires a focused effort, but the shift is inevitable," she said in prepared remarks that did not touch on monetary policy. Benefits from providing the FedNow Service as a neutral platform, accessible to financial institutions of all sizes nationwide, said Brainard, include increasing competition for end-user services and promoting innovation. The FedNow system would compete with a separate real-time network built and launched by big banks in 2017.

CANADA

BOC: Companies are already bidding up wages in response to rapid inflation, says a top economist from the business group that hosted BOC Governor Tiff Macklem last month when he argued firms should stick with modest salary decisions.

- “We have three times as many firms now planning on aggressive wage hikes, compared to say what we had before the pandemic, and even with that we still have significant labor shortages,” said Andreea Bourgeois of the Canadian Federation of Independent Business. “When we have such a high share of businesses planning very major wage increases,” she said, then wage-driven inflation “is already part of that story” around broader inflation. For more see MNI Policy main wire at 0731ET.

US TSYS: Narrow/Weaker Range

Tsy futures hold weaker after the bell, maintaining narrow range since noon after see-sawing to new session lows (through overnight lows) late morning w/30YY tapping 3.2662% high, yield curves steeper/new highs (2s10s taps -29.564 high). Thin markets/whippy trade tied to lack of participants (London bank holiday) and limited data:

- US AUG. DALLAS FED MANUFACTURING INDEX AT -12.9 VS -22.6

- US AUG. DALLAS FED GENERAL BUSINESS ACTIVITY AT -12.9

- Tsys see-sawed on earlier ECB Lane comments:

- "Our upcoming September monetary policy meeting will be the start of a new phase... In terms of execution, this new phase will consist of a meeting-by-meeting (MBM) approach to setting interest rates... As policy rates move away from the lower bound, the inherent flexibility of the MBM approach is better suited to calibrating monetary policy in a highly uncertain environment."

- Rates rebounded on follow-up comment over smaller hikes "make it easier to correct course."

- Technicals for TYU2 at 117-00.5: outlook remains bearish and the contract has resumed its downtrend, breaching last week’s low of 117-03+ on Aug 24 / 25 low. This confirms a resumption of the current bear cycle and opens 116-11 next, the Jun 28 low. Further out, attention is on 116-02+, a Fibonacci retracement. Initial resistance has been defined at 117-29+, Friday’s high. The 50-day EMA, at 118-28+ marks a firmer resistance.

OVERNIGHT DATA

- US AUG. DALLAS FED MANUFACTURING INDEX AT -12.9 VS -22.6

- US AUG. DALLAS FED GENERAL BUSINESS ACTIVITY AT -12.9

MARKETS SNAPSHOT

Key late session market levels:

- DJIA down 15.72 points (-0.05%) at 32268.4

- S&P E-Mini Future down 3.5 points (-0.09%) at 4056

- Nasdaq down 48.9 points (-0.4%) at 12092.58

- US 10-Yr yield is up 6.7 bps at 3.108%

- US Sep 10Y are down 17/32 at 117-1.5

- EURUSD up 0.003 (0.3%) at 0.9996

- USDJPY up 1.15 (0.84%) at 138.79

- WTI Crude Oil (front-month) up $3.84 (4.13%) at $96.91

- Gold is down $0.75 (-0.04%) at $1737.41

- EuroStoxx 50 down 33.17 points (-0.92%) at 3570.51

- German DAX down 78.48 points (-0.61%) at 12892.99

- French CAC 40 down 51.98 points (-0.83%) at 6222.28

US TSY FUTURES CLOSE

- 3M10Y +1.339, 21.378 (L: 19.275 / H: 25.787)

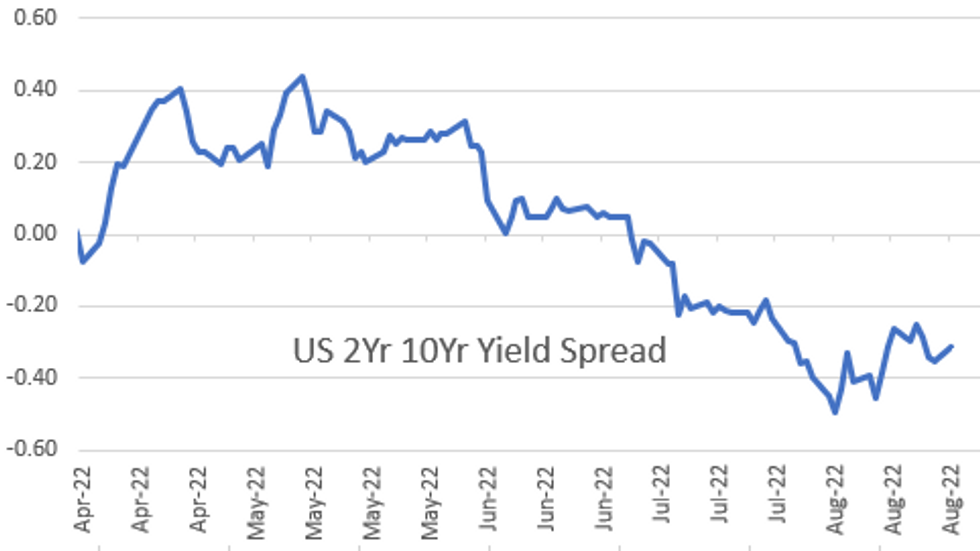

- 2Y10Y +4.263, -31.928 (L: -37.781 / H: -29.564)

- 2Y30Y +2.807, -18.062 (L: -23.62 / H: -15.038)

- 5Y30Y -0.01, -1.655 (L: -4.654 / H: 0.554)

- Current futures levels:

- Sep 2Y down 1.875/32 at 104-10.625 (L: 104-06.875 / H: 104-12.375)

- Sep 5Y down 10.75/32 at 110-27.5 (L: 110-22 / H: 111-03.5)

- Sep 10Y down 17.5/32 at 117-1 (L: 116-26.5 / H: 117-14.5)

- Sep 30Y down 1-05/32 at 136-17 (L: 136-08 / H: 137-20)

- Sep Ultra 30Y down 1-09/32 at 149-25 (L: 149-09 / H: 151-06)

US 10YR FUTURE TECHS: (U2) Heading South

- RES 4: 119-31 High Aug 15

- RES 3: 119-14+ High Aug 17

- RES 2: 118-28+ 50-day EMA

- RES 1: 117-29+/118-20 High Aug 26 / 20-day EMA

- PRICE: 116-31 @ 11:05 BST Aug 29

- SUP 1: 116-26+ Low Jun 29 and the intraday low

- SUP 2: 116-11 Low Jun 28

- SUP 3: 116-02+ 76.4% retracement of the Jun 14 - Aug 2 bull run

- SUP 4: 115-20 Low Jun 17

The Treasuries outlook remains bearish and the contract has resumed its downtrend, breaching last week’s low of 117-03+ on Aug 24 / 25 low. This confirms a resumption of the current bear cycle and opens 116-11 next, the Jun 28 low. Further out, attention is on 116-02+, a Fibonacci retracement. Initial resistance has been defined at 117-29+, Friday’s high. The 50-day EMA, at 118-28+ marks a firmer resistance.

US EURODOLLAR FUTURES CLOSE

- Sep 22 -0.033 at 96.593

- Dec 22 -0.060 at 95.925

- Mar 23 -0.050 at 95.910

- Jun 23 -0.050 at 95.955

- Red Pack (Sep 23-Jun 24) -0.05 to -0.035

- Green Pack (Sep 24-Jun 25) -0.075 to -0.05

- Blue Pack (Sep 25-Jun 26) -0.105 to -0.085

- Gold Pack (Sep 26-Jun 27) -0.115 to -0.11

Short Term Rates

US DOLLAR LIBOR: No new settlements Monday due to London bank holiday, resume Tuesday. In the meantime, below are Friday's settlements:

- O/N -0.01129 to 2.30914% (-0.01200/wk)

- 1M +0.03043 to 2.52386% (+0.09858/wk)

- 3M +0.02643 to 3.06957% (+0.11186/wk) * / **

- 6M +0.03957 to 3.56643% (+0.01886/wk)

- 12M +0.02600 to 4.12329% (+0.10473/wk)

- * Record Low 0.11413% on 9/12/21; ** New 14Y high: 3.06957% on 8/26/22

- Daily Effective Fed Funds Rate: 2.33% volume: $98B

- Daily Overnight Bank Funding Rate: 2.32% volume: $281B

- Secured Overnight Financing Rate (SOFR): 2.28%, $953B

- Broad General Collateral Rate (BGCR): 2.26%, $391B

- Tri-Party General Collateral Rate (TGCR): 2.26%, $385B

- (rate, volume levels reflect prior session)

FED Reverse Repo Operation

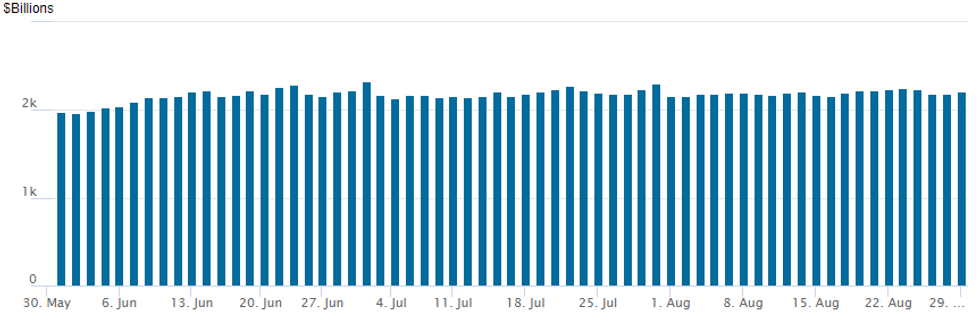

NY Federal Reserve/MNI

NY Fed reverse repo usages climbs to $2,205.188B w/ 99 counterparties vs. $2,182.452B prior session. Record high still stands at $2,329.743B from Thursday June 30.

Pipeline

- No new high grade issuance Monday, August running total at $165.7B.

Tuesday Data Calendar

| Date | GMT/Local | Impact | Flag | Country | Event |

| 30/08/2022 | 0130/1130 | * |  | AU | Building Approvals |

| 30/08/2022 | 0700/0900 | ** |  | SE | Economic Tendency Indicator |

| 30/08/2022 | 0700/0900 |  | ES | Retail sales | |

| 30/08/2022 | 0700/0900 | *** | | ES | HICP (p) |

| 30/08/2022 | 0800/1000 | *** |  | DE | Bavaria CPI |

| 30/08/2022 | 0830/0930 | ** |  | UK | BOE M4 |

| 30/08/2022 | 0830/0930 | ** | | UK | BOE Lending to Individuals |

| 30/08/2022 | 0900/1100 | *** | | DE | Saxony CPI |

| 30/08/2022 | 0900/1100 | ** |  | EU | Economic Sentiment Indicator |

| 30/08/2022 | 0900/1100 | * | | EU | Consumer Confidence, Industrial Sentiment |

| 30/08/2022 | 0900/1100 | * | | EU | Business Climate Indicator |

| 30/08/2022 | 1200/1400 | *** | | DE | HICP (p) |

| 30/08/2022 | 1200/0800 |  | US | Richmond Fed's Tom Barkin | |

| 30/08/2022 | 1230/0830 | * |  | CA | Current account |

| 30/08/2022 | 1255/0855 | ** | | US | Redbook Retail Sales Index |

| 30/08/2022 | 1300/0900 | ** | | US | S&P Case-Shiller Home Price Index |

| 30/08/2022 | 1300/0900 | ** | | US | FHFA Home Price Index |

| 30/08/2022 | 1300/0900 | ** | | US | FHFA Quarterly Price Index |

| 30/08/2022 | 1400/1000 | *** | | US | Conference Board Consumer Confidence |

| 30/08/2022 | 1400/1000 | ** | | US | JOLTS jobs opening level |

| 30/08/2022 | 1400/1000 | ** | | US | JOLTS quits Rate |

| 30/08/2022 | 1500/1100 | | US | New York Fed's John Williams |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.